Friday, February 4, 2022

Housing View – February 4, 2022

On cross-country:

- Housing Returns in Big and Small Cities – New York Fed

- Large investors drive up house prices in Europe’s cities, study finds. Housing is increasingly attractive asset for institutional investors due to near zero interest rates – The Guardian and link to report

- Crypto Kings Are the Real-Estate Industry’s Newest Whales. People who have made fortunes investing in digital currency, or who helped build the vast crypto industry, are the new darlings of the high-end residential property market – Wall Street Journal

- Real estate prices are rising at record speed in US, UK and Australia, as WFH and the pandemic pushed families out of big cities in 2021 – are new homes still a good investment? – South China Morning Post

On the US:

- How the Fed’s Policy Shift Is Rippling Through the Housing Market. The central bank had been the biggest buyer of mortgage bonds, but now it is stepping back and borrowing costs are rising – Wall Street Journal

- Wonking Out: Are We in Another Housing Bubble? – New York Times

- Why, and Where, are Housing Prices Rising? – Econofact

- The Simple Reason Why So Many Can’t Afford Housing – Barron’s

- It’s Harder to Find a Home Than Love When Housing Markets Are This Hot. Bidding wars, low inventory and huge price hikes have turned homebuying into an ordeal for many house hunters over the past two years. – Bloomberg

- Would Housing Cost Less If It Were Easier to Build New Homes? Surprisingly, Not Much. A new study suggests that supply and demand are only part of a complex problem – Kellogg Insight

- New York’s ideas for zoning reform offer many paths to tackling the housing crisis – Brookings

- Newly Built Homes Make Up Record Share of U.S. Housing Supply – Bloomberg

- Rents are up 40 percent in some cities, forcing millions to find another place to live – Washington Post

- Wall Street’s $85 Billion Housing Bet Intensifies U.S. Land Boom. Investors are snapping up lots to build an empire of suburban rental homes. – Bloomberg

- What Financial Resources Have Renters Tapped During the Pandemic? – Harvard Joint Center for Housing Studies

- Report: Owning more affordable than renting in most housing markets – Washington Post

- December Rental Data: Rents Surged by 10.1% in 2021 – Realtor.com

- The Record-Breaking Rental Market – Harvard Joint Center for Housing Studies

- ‘It’s anguish, it’s pain, it’s agony’ – here’s what it’s like to shop for a home in today’s tight housing market – CNBC

- Measuring America’s Affordability Problem: Comparing Alternative Measurements of Affordable Housing – Housing Policy Debate

- When Will Be a Good Time to Buy a House? There won’t be a perfect moment anytime soon—but that shouldn’t stop you if you’re ready. – The Atlantic

- AEI housing market indicators, January 2022 – AEI

- Where to build in a state on fire? California housing projects face growing challenges – The Guardian

- Regulation and the Housing Affordability Crisis. Government regulations account for nearly 25% of the price of building a single-family home. – Wall Street Journal

- Why Are Residential Property Tax Rates Regressive? – Federal Reserve Bank of Philadelphia

- Q4 Homeownership Rate Reflects Slight Growth, Demographic Disparities – Realtor.com

- Exploring Climate Change in U.S. Housing Policy – Housing Policy Debate

- The Role of 421-a during a Decade of Market Rate and Affordable Housing Development – NYU Furman Center

On China

- Beijing has shortcut to prop up real estate – Reuters

- Understanding the Resurgence of the SOEs in China: Evidence from the Real Estate Sector – NBER

- China Home Sales Slump Deepened in January in Blow to Economy – Bloomberg

On other countries:

- [Australia] Regional house prices surge as Melburnians flood coastal and tree-change hotspots – The Sydney Morning Herald

- [Australia] Australia Home Prices Edge Up, Further Sign of Cooling Boom – Bloomberg

- [Brazil] The financialisation of housing by numbers: Brazilian real estate developers since the Lulist era – Housing Studies

- [Canada] This is what a rate hike will cost homeowners – Globe and Mail

- [Canada] Bank of Canada ‘no hike’ leaves housing fire burning, say market watchers – Reuters

- [Canada] Housing Market in a ‘Speculative Fever,’ Canada Regulator Says – Bloomberg

- [Israel] New plan aims to entice cities to construct housing with NIS 60 million bait. To resolve housing crisis, government will reward 12 high-demand municipalities with cash for each apartment approved; project could add 30,000 new units in the next three years – The Times of Israel

- [Netherlands] Sentiment in the Housing Market – University of Groningen

- [Singapore] Singapore House Prices Surge Most in Decade as Curbs Test Market – Bloomberg

- [Spain] Housing prices in Spain: convergence or decoupling? – Central Bank of Spain

- [Spain] Spain’s new “right to housing” law enshrines rent control nationwide – Quartz

- [Switzerland] Swiss banks criticise steps to cool runaway property market – Reuters

- [United Kingdom] Demand Is Surging for Flats Outside London. Price increases for apartments have been relatively modest compared to other types of property, according to Zoopla. – Bloomberg

- [United Kingdom] The plight of the UK’s first-time buyers. The immediate pressures of the pandemic may have eased, but prospective homeowners must now contend with record prices and a looming cost of living crisis – FT

- [United Kingdom] Failure to help struggling households will cost Tories dear. Rising housing and energy costs plus higher taxes mean ministers have to come up with something – The Guardian

- [United Kingdom] UK homeowners secure £800bn windfall with house price rise. Average property values increased more than 10 per cent last year, according to new analysis – FT

- [United Kingdom] UK house prices show strongest start to year since 2005. Property price index rises by annual rate of 11.2% in January surpassing economists’ expectations – FT

- [United Kingdom] Mortgage lenders cut 10-year fixed rates ahead of Bank rate decision. Borrowers seeking long-term fixed-rate loans amid rising rates and inflation – FT

On cross-country:

- Housing Returns in Big and Small Cities – New York Fed

- Large investors drive up house prices in Europe’s cities, study finds. Housing is increasingly attractive asset for institutional investors due to near zero interest rates – The Guardian and link to report

- Crypto Kings Are the Real-Estate Industry’s Newest Whales. People who have made fortunes investing in digital currency,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, February 3, 2022

Do Well Managed Firms Make Better Forecasts?

New NBER Working paper by Nicholas Bloom, Takafumi Kawakubo, Charlotte Meng, Paul Mizen, Rebecca Riley, Tatsuro Senga & John Van Reenen.

“We link a new UK management survey covering 8,000 firms to panel data on productivity in manufacturing and services. There is a large variation in management practices, which are highly correlated with productivity, profitability and size. Uniquely, the survey collects firms’ micro forecasts of their own sales and also macro forecasts of GDP. We find that better managed firms make more accurate micro and macro forecasts, even after controlling for their size, age, industry and many other factors. We also show better managed firms appear aware that their forecasts are more accurate, with lower subjective uncertainty around central values. These stylized facts suggest that one reason for the superior performance of better managed firms is that they knowingly make more accurate forecasts, enabling them to make superior operational and strategic choices.”

Read more here.

New NBER Working paper by Nicholas Bloom, Takafumi Kawakubo, Charlotte Meng, Paul Mizen, Rebecca Riley, Tatsuro Senga & John Van Reenen.

“We link a new UK management survey covering 8,000 firms to panel data on productivity in manufacturing and services. There is a large variation in management practices, which are highly correlated with productivity, profitability and size. Uniquely, the survey collects firms’ micro forecasts of their own sales and also macro forecasts of GDP.

Posted by at 2:22 PM

Labels: Forecasting Forum

Do realized higher moments have information content? – VaR forecasting based on the realized GARCH-RSRK model

New paper by Tianyi Wang, Hong Yan, Zhuo Huang & Fang Liang in Economic Modelling.

“In this paper, we develop a new model, the Realized GARCH-RSRK, to determine the time-varying distribution of financial returns with realized higher moments. Based on Gram-Charlier expansion (GCE) density, we first explicitly link the expansion parameters with moments that are calculated based on intraday returns using our new model. Then, the Cornish-Fisher expansion is applied to forecast Value-at-Risk (VaR) with estimated moments to demonstrate the economic significance of this new model. Compared with the daily-return-based dynamic higher moments models, the inclusion of realized higher moments significantly improves this model’s ability to forecast extreme tails. The empirical results indicate that this new model outperforms the benchmark models when forecasting extreme VaR. In addition, we provide a formula to correct the moments associated with the commonly used squared transformation of GCE. Our empirical evidence highlights the importance of using corrected moments in VaR forecasting.”

Read more by clicking here.

New paper by Tianyi Wang, Hong Yan, Zhuo Huang & Fang Liang in Economic Modelling.

“In this paper, we develop a new model, the Realized GARCH-RSRK, to determine the time-varying distribution of financial returns with realized higher moments. Based on Gram-Charlier expansion (GCE) density, we first explicitly link the expansion parameters with moments that are calculated based on intraday returns using our new model. Then, the Cornish-Fisher expansion is applied to forecast Value-at-Risk (VaR) with estimated moments to demonstrate the economic significance of this new model.

Posted by at 1:16 PM

Labels: Forecasting Forum

The Economics of Internal Migration: Advances and Policy Questions

From a new paper by Ning Jia, Raven Molloy, Christopher Smith, and Abigail Wozniak:

“Internal migration patterns in the US have drawn growing attention among researchers, policy analysts, and others. This interest has been driven by two trends. First, internal migration in the US has fallen for more than three decades (Molloy et al. 2011; Frey 2009; Cooke 2011, 2013). This decline raises questions about whether it stems from desirable factors, like improved location or job matching, or undesirable factors, like employer monopsony power or other barriers to job mobility (Kaplan and Schulhofer-Wohl 2017; Molloy et al. 2016). Relatedly, highly educated Americans have become increasingly concentrated in larger cities (Diamond 2016). Thus, both the level of migration in the US and the types of destinations chosen by different types of people have changed in important ways over the last several decades.

(…)

Dao et al. (2017) revisit the key ideas from BK and show more directly that the nature of local labor market adjustment to demand shocks has changed in the last few decades—and that the diminished responsiveness of net migration is a key reason for the change in how local labor markets adjust. The authors take a similar approach to BK by estimating adjustment margins at the state level’s response to demand shocks. However, they extend the BK sample with an additional 20 years of data and make other methodological innovations, including using administrative data on migration flows instead of inferring population adjustment from CPS-based measures. Among the many useful contributions of this analysis is a demonstration that after 1990, the net migration response to a state-level demand shock has been smaller on average than in earlier periods, and the response of the unemployment and labor force participation rates is larger. Hence, one way to reconcile the BK findings with the more recent conflicting evidence on local labor market adjustment and regional divergence is that migration was more important as an equilibrating mechanism from the 1970s through the early 1990s (the period in the BK sample) and has recently become less important.”

From a new paper by Ning Jia, Raven Molloy, Christopher Smith, and Abigail Wozniak:

“Internal migration patterns in the US have drawn growing attention among researchers, policy analysts, and others. This interest has been driven by two trends. First, internal migration in the US has fallen for more than three decades (Molloy et al. 2011; Frey 2009; Cooke 2011, 2013). This decline raises questions about whether it stems from desirable factors,

Posted by at 7:18 AM

Labels: Inclusive Growth, Macro Demystified

Wednesday, February 2, 2022

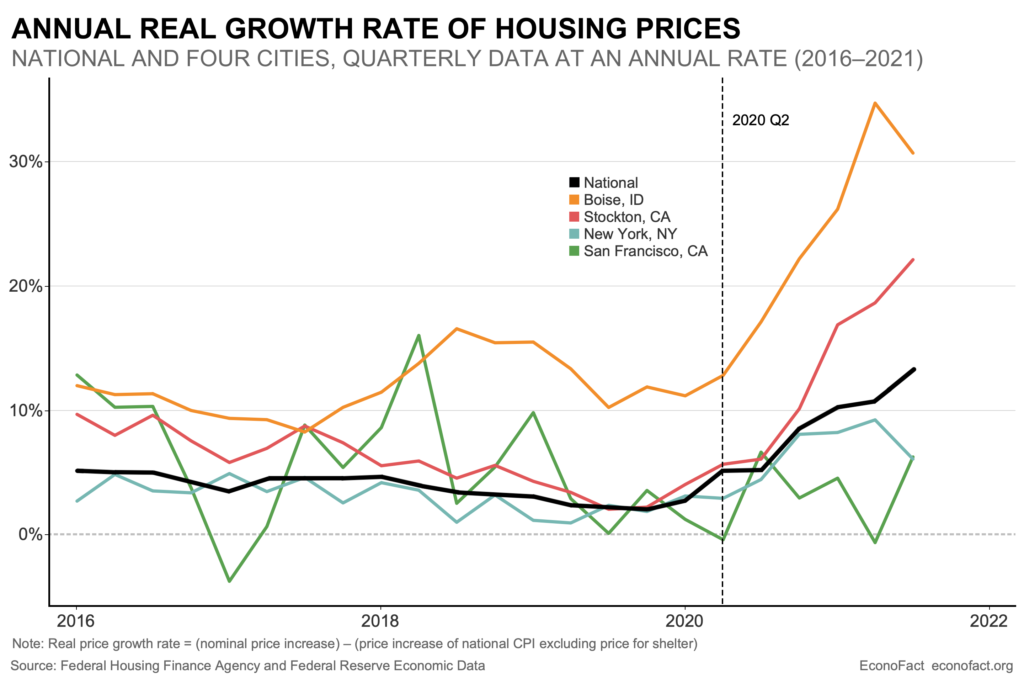

Why, and Where, are Housing Prices Rising?

From Econofact:

“The Issue:

The price of housing has a special importance because housing is both a basic necessity and a key component of wealth. Around the start of the pandemic, some experts predicted a protracted collapse in housing prices and the housing market. For example, in April 2020 the staff at Freddie Mac projected home prices would fall by 0.5 percent over the next year. In fact, the opposite happened: The Case Shiller National Home Price Index rose by 15 percent between April 2020 and April 2021 while home sales hit a 15 year high in the calendar year 2021. This stands in stark contrast to the Great Recession when the price index fell 44 percent between May 2007 and May 2009. But one similarity across the Great Recession and the COVID downturn is the wide differences in housing price changes across different parts of the United States. What has happened to housing prices during the COVID pandemic and why? And what are the broader economic implications of this?

The Facts:

House sales and housing construction fell at the outset of the pandemic in March 2020. The total housing inventory on the market, including newly constructed houses and those being resold, was down 10.2 percent between March 2019 and March 2020. Between February 2020 and March 2020 housing starts declined by 22.3 percent, perhaps reflecting builders’ bleak expectations for future demand. Total existing-home sales fell 8.5 percent in March 2020 compared with the prior month and tumbled a further 17.8 percent in April.”

Continue reading here.

From Econofact:

“The Issue:

The price of housing has a special importance because housing is both a basic necessity and a key component of wealth. Around the start of the pandemic, some experts predicted a protracted collapse in housing prices and the housing market. For example, in April 2020 the staff at Freddie Mac projected home prices would fall by 0.5 percent over the next year.

Posted by at 2:03 PM

Labels: Global Housing Watch

Subscribe to: Posts