Monday, February 14, 2022

Racial Disparities in the Paycheck Protection Program

Source: NBER Working Paper (2022)

Researchers Sergey Chernenko and David S. Scharfstein write about the significant racial disparities in borrowing through the Paycheck Protection Program (PPP) using data gathered from a large sample of restaurants in Florida and then investigate the causes of these disparities. They find that- “Black-owned restaurants are 25% less likely to receive PPP loans. Restaurant location explains 5 percentage points of this differential. Restaurant characteristics explain an additional 10 percentage points of the gap in PPP borrowing. On average, prior borrowing relationships do not explain disparities. The remaining 10% disparity is driven by a 17% disparity in PPP borrowing from banks, which is partially offset by greater borrowing from nonbanks, largely fintechs. Disparities in PPP borrowing cannot be attributed to lower awareness of PPP loans or lower demand for PPP loans by minority-owned restaurants. Black-owned restaurants are significantly less likely to receive bank PPP loans in counties with more racial bias. In these counties, Black-owned restaurants are more likely to substitute to nonbank PPP loans. This substitution, however, is not strong enough to eliminate racial disparities in PPP borrowing”.

Source: NBER Working Paper (2022)

Researchers Sergey Chernenko and David S. Scharfstein write about the significant racial disparities in borrowing through the Paycheck Protection Program (PPP) using data gathered from a large sample of restaurants in Florida and then investigate the causes of these disparities. They find that- “Black-owned restaurants are 25% less likely to receive PPP loans. Restaurant location explains 5 percentage points of this differential. Restaurant characteristics explain an additional 10 percentage points of the gap in PPP borrowing.

Posted by at 12:05 PM

Labels: Inclusive Growth

Saturday, February 12, 2022

Vulnerabilities in the residential real estate sectors of the EEA countries

From European Systemic Risk Board:

“In this report, the ESRB presents its medium-term assessment of vulnerabilities relating to the RRE sector across the EEA countries. In carrying out this assessment, the ESRB first performed an analysis of vulnerabilities across the EEA countries. For the 24 countries for which the vulnerabilities identified were more pronounced, an in-depth analysis was conducted. This analysis pointed also to the need to take into account or change other than macroprudential policies, for example by changing tax incentives or increasing the housing supply. A similar assessment was conducted by the ESRB in 2019, when 11 countries received either ESRB recommendations (Belgium, Denmark, Finland, Luxembourg, Netherlands and Sweden) or warnings (Czech Republic, Germany, France, Iceland and Norway).

The risk assessment concluded that, in five countries which received ESRB recommendations or warnings in 2019 (Denmark, Luxembourg, Netherlands, Norway and Sweden) the vulnerabilities relating to residential real estate markets remained high, while in six countries (Belgium, Czech Republic, Germany, Finland, France and Iceland) the vulnerabilities were assessed as medium. Among other EEA countries, 13 (Austria, Bulgaria, Estonia, Croatia, Hungary, Ireland, Liechtenstein, Lithuania, Malta, Poland, Portugal, Slovenia and Slovakia) were identified as facing medium risks.

The policy assessment found that in five countries which received ESRB recommendations or warnings in 2019 (Belgium, Czech Republic, France, Iceland and Norway), policies were assessed as appropriate and sufficient to mitigate the vulnerabilities identified. In two countries (the Netherlands and Sweden), policies were assessed as being appropriate but partially sufficient, while in four of the countries (Germany, Denmark, Finland and Luxembourg), policies were assessed as partially appropriate and partially sufficient. Among the rest of the EEA countries analysed in this report, in one country (Slovakia) policies were identified as appropriate and partially sufficient, while in five countries (Austria, Bulgaria, Hungary, Croatia and Liechtenstein) policies were found to be partially appropriate and partially sufficient.

In countries in which the policies were assessed as only partially sufficient to mitigate the identified vulnerabilities, the ESRB suggested various macroprudential measures to be considered by the national authorities. In particular, the ESRB pointed out that a number of countries should either introduce additional borrower-based measures or tighten existing ones to mitigate the existing vulnerabilities more effectively or prevent a further build-up of vulnerabilities. Countries with accumulated vulnerabilities should also ensure that capital is preserved until a possible materialisation of risks or consider (re)introducing capital-based measures once the economic recovery is on a firm footing. However, taking into account the economic uncertainty related to the pandemic, any policy actions should be carefully assessed to ensure that they contribute towards mitigating RRE vulnerabilities, while aiming to avoid procyclical effects on the real economy and the financial system. In the near term, it is particularly important for all countries that banks make adequate provision for expected losses. Finally, the analysis notes that, in some countries in which the systemic risk levels identified remain high, interventions in other policy areas may be required to complement macroprudential policy.”

From European Systemic Risk Board:

“In this report, the ESRB presents its medium-term assessment of vulnerabilities relating to the RRE sector across the EEA countries. In carrying out this assessment, the ESRB first performed an analysis of vulnerabilities across the EEA countries. For the 24 countries for which the vulnerabilities identified were more pronounced, an in-depth analysis was conducted. This analysis pointed also to the need to take into account or change other than macroprudential policies,

Posted by at 6:29 AM

Labels: Global Housing Watch

Friday, February 11, 2022

Debt Vulnerability Analysis: A Multi-Angle Approach

Source: World Bank Working Paper (2022)

“This paper develops a methodology to identify countries that are at risk of debt default based on four elements of debt vulnerability. These elements capture the different ways in which risks associated with high debt are assessed, namely: (i) the fundamental, (ii) the subjective, (iii) the judgmental, and (iv) the theoretical. The fundamental element considers the liquidity, solvency, and institutional risk elements of debt vulnerability. The subjective element captures the investors’ perceptions of debt default, while the judgmental element is based on the debt thresholds as defined by Debt Sustainability Frameworks. Finally, the theoretical element is normative and captures what ought to be. The methodology constructs an index for each of these four elements and uses them as predictors in a model of public debt default. The methodology flags countries that are at risk of default by means of machine learning techniques and delivers outputs that point to underlying causes of vulnerability.”

Also Read:

Source: World Bank Working Paper (2022)

“This paper develops a methodology to identify countries that are at risk of debt default based on four elements of debt vulnerability. These elements capture the different ways in which risks associated with high debt are assessed, namely: (i) the fundamental, (ii) the subjective, (iii) the judgmental, and (iv) the theoretical. The fundamental element considers the liquidity, solvency, and institutional risk elements of debt vulnerability.

Posted by at 12:23 PM

Labels: Macro Demystified

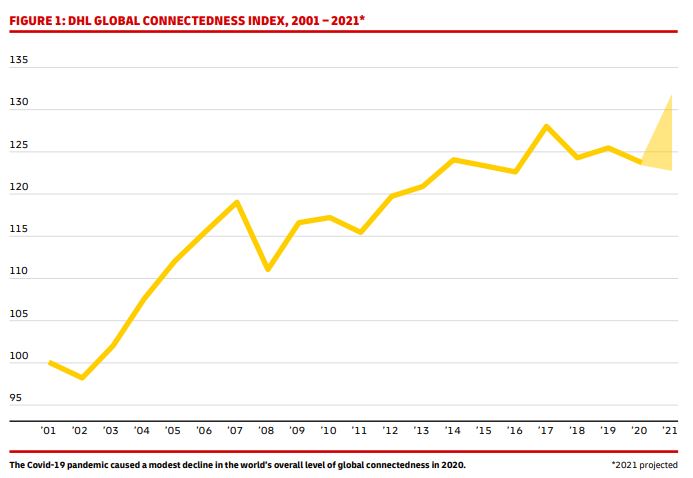

DHL Global Connectedness Index – 2021 Update

From a new report by Steven A. Altman and Caroline R. Bastian:

“The DHL Global Connectedness Index measures globalization based on international flows of trade, capital, information, and people. This update highlights key developments in these four areas for the world as a whole, with a focus on the Covid-19 crisis. Overall, globalization is emerging from the pandemic far stronger than many expected. The DHL Global Connectedness Index declined modestly in 2020, and there is clear evidence of a recovery underway in 2021. Nonetheless, the pandemic has also highlighted vulnerabilities that should be addressed in order to fortify and expand the benefits of global connectedness.”

From a new report by Steven A. Altman and Caroline R. Bastian:

“The DHL Global Connectedness Index measures globalization based on international flows of trade, capital, information, and people. This update highlights key developments in these four areas for the world as a whole, with a focus on the Covid-19 crisis. Overall, globalization is emerging from the pandemic far stronger than many expected. The DHL Global Connectedness Index declined modestly in 2020,

Posted by at 6:31 AM

Labels: Macro Demystified

Housing View – February 11, 2022

On cross-country:

- Property ladder too high for central Europe’s first-time buyers – Reuters

On the US:

- The Housing Boom May Be About to Go Bust. A new generation of buyers is jumping into the market at what may be the worst possible time. – Bloomberg

- The Housing Party Is Starting to Wind Down. Builders are ramping up supply just as a record low percentage of Americans say it’s a good time to buy a home. – Bloomberg

- In Covid-19 Housing Market, the Middle Class Is Getting Priced Out. Surging demand and shrinking supply combine to make home buying more difficult, as affordability worsens for many – Wall Street Journal

- It’s Time to Put Cities at the Top of America’s Economic Agenda. The U.S. economy today is actually a collection of regional economies. We need a national place-based strategy that recognizes local differences. – Bloomberg

- National and Metro Housing Market Indicators – AEI

- Zillow: Our 2022 housing forecast is way off—home prices now set to spike 16% – Fortune

- Inequality in the Time of COVID-19: Evidence from Mortgage Delinquency and Forbearance – Philadelphia Fed

- Is the ‘American Dream’ of Homeownership a False Promise? In “Owned: A Tale of Two Americas,” director Giorgio Angelini traces the origins of a discriminatory housing market. – Bloomberg

- Record-High Prices and Record-Low Inventory Make It Increasingly Difficult to Achieve Homeownership, Particularly for Black Americans – NAR

- Want Affordable Housing? Strengthen Regional Governments. Most Americans live in metropolitan areas, and it takes a metropolitan regional government to coordinate the growth in housing, transit, and employment that makes the region livable. – The American Prospect

- The Housing Situation Is Dire. But Progress Is Still Possible. In the South Bronx, developers found ways to build an array of sleek, affordable apartments in two subsidized housing developments. Is this a way forward? – New York Times

- There are hardly any houses left to buy – Axios

- US Housing Supply Gap Expands in 2021 – Realtor.com

- Diverse neighborhoods are made of diverse housing – Brookings

- U.S. Housing Costs Surge, With No End In Sight. Locked out of the supply-constrained home-buying market, more households are crowding the rental market, driving up rents and stressing housing support programs. – Bloomberg

- How Rent Hikes Make Buying a House Even Harder. Rising rents are pushing many to buy a home even if the housing market is already tough – Wall Street Journal

- Where Are Rents Rising the Most? In 2021, rents rebounded from pandemic lows in nearly all of the 100 largest American cities. – New York Times

- What Freddie Mac is Doing About the Rental Affordability Crisis – Freddie Mac

- Millennial Demand is Driving up Prices in Family-Friendly Neighborhoods – Zillow

- How strip malls could help solve the housing shortage. There’s a lot of space for apartments above the commercial real estate on main suburban streets – Fast Company

- California’s Free-Market Housing Fix. A new state law allows landowners to build four units on most lots zoned currently for one unit. – Wall Street Journal

- They Rushed to Buy in the Pandemic. Here’s What They Would Change. A frenzied sellers’ market led some people to make harried decisions when buying their homes that they now regret. – New York Times

- Homeownership in old age and at the time of death – Economics Letters

- How New York’s housing market got even more ridiculous. For a brief moment, dream apartments seemed possible – but then it all came crashing down – The Guardian

- American Protectionism and Construction Materials Costs. Tariffs imposed by the U.S. government on materials used by the domestic construction sector cause a significant increase in the cost of those goods. – Cato Institute

- The Sustainable City Podcast: Where the Suburbs End. Join us as we discuss California’s audacious effort to deconstruct single-family zoning – New York Times

On China

- Chinese property group Shimao feels chill of sector’s liquidity crisis. Developer sucked into bond market sell-off following Evergrande collapse – FT

- China’s Taking on a Risky Bubble Deflation Experiment. Property investors, like Wile E. Coyote, may feel wobbly if they look down. – Bloomberg

- China Eases Property Loan Curbs as Housing Market Slumps. Loans to fund public rental housing become exempt from limits. PBOC’s move is latest softening of real estate clampdown – Bloomberg

On other countries:

- [Canada] Canadians Deepen Faith in Red-Hot Housing While Rate Hikes Loom. 64% expect real-estate prices to rise over next half year. Jump in sentiment comes amid central bank, regulatory warnings – Bloomberg

- [Iceland] Europe’s Hottest Housing Boom May Prompt Bigger Hike in Iceland. Central bank might raise key interest rate by 0.75% this week. House prices on Atlantic island have risen 150% since 2010 – Bloomberg

- [United Kingdom] Why are there so few homes for sale in the UK? A supply crunch has left many prospective buyers struggling to find the right property – FT

- [United Kingdom] Most Tory voters want more affordable housing stock, finds poll. YouGov study also finds most Conservative supporters in favour of higher taxes on second homes – The Guardian

- [United Kingdom] Residential rents rise at fastest pace in 13 years. Tenants under pressure to find affordable urban homes as workplaces reopen – FT

- [United Kingdom] U.K. Builder Says House Prices Outpacing Cost-Inflation Surge – Bloomberg

- [United Kingdom] These Are Britain’s Property Hotspots. The North-South divide is stark in a new analysis of property price growth over the past decade, with southern England values almost doubling in several places. – Bloomberg

On cross-country:

- Property ladder too high for central Europe’s first-time buyers – Reuters

On the US:

- The Housing Boom May Be About to Go Bust. A new generation of buyers is jumping into the market at what may be the worst possible time. – Bloomberg

- The Housing Party Is Starting to Wind Down. Builders are ramping up supply just as a record low percentage of Americans say it’s a good time to buy a home.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts