Monday, February 21, 2022

The World Uncertainty Index

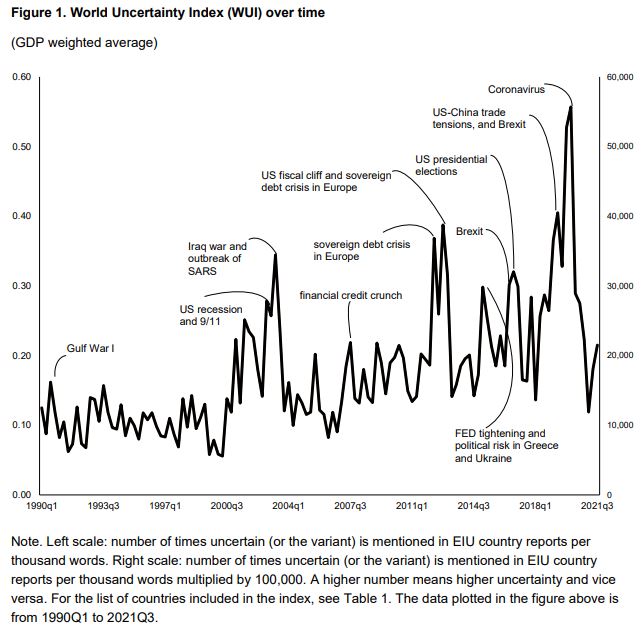

From a NBER paper by Hites Ahir, Nicholas Bloom and Davide Furceri:

“We construct the World Uncertainty Index (WUI) for an unbalanced panel of 143 individual countries on a quarterly basis from 1952. This is the frequency of the word “uncertainty” in the quarterly Economist Intelligence Unit country reports. Globally, the Index spikes around major events like the Gulf War, the Euro debt crisis, the Brexit vote and the COVID pandemic. The level of uncertainty is higher in developing countries but is more synchronized across advanced economies with their tighter trade and financial linkages. In a panel vector autoregressive setting we find that innovations in the WUI foreshadow significant declines in output. This effect is larger and more persistent in countries with lower institutional quality, and in sectors with greater financial constraints.”

From a NBER paper by Hites Ahir, Nicholas Bloom and Davide Furceri:

“We construct the World Uncertainty Index (WUI) for an unbalanced panel of 143 individual countries on a quarterly basis from 1952. This is the frequency of the word “uncertainty” in the quarterly Economist Intelligence Unit country reports. Globally, the Index spikes around major events like the Gulf War, the Euro debt crisis, the Brexit vote and the COVID pandemic.

Posted by at 6:11 PM

Labels: Macro Demystified

Education, Income and Mobility: Experimental Impacts of Childhood Progresa after 20 Years

Source: Poverty Action Lab, Paris School of Economics

In 1997, the Mexican government designed the conditional cash transfer program Progresa, which became the

worldwide model of a new approach to social programs, simultaneously targeting human capital accumulation

and poverty reduction. This paper studies the differential long-term impact of children’s exposure to Progresa, 20 years after its launch. The two focus groups include (a) children who were in-utero or in their initial years of life, and (b) children who were transitioning from primary to secondary school.

Results show that children exposed to the program in their early childhood witnessed better educational attainment and labor market outcomes, and the study of impacts on the second group shows that even the short-term impact of the program was sustained in the long run. Positive impacts manifested as larger labor incomes, more geographical mobility including through international migration, and later family formation. Besides, results from this paper also confirm that while conditional cash transfers are helpful in enhancing the educational and nutritional development of children in their formative stages, there is still a need for complementary policies to be rolled out so that the full range of households (not just ones with infants at the time of program rollout) are able to realize the full range of newly available labor market opportunities.

Click here to be a part of the discussion on this paper.

Source: Poverty Action Lab, Paris School of Economics

In 1997, the Mexican government designed the conditional cash transfer program Progresa, which became the

worldwide model of a new approach to social programs, simultaneously targeting human capital accumulation

and poverty reduction. This paper studies the differential long-term impact of children’s exposure to Progresa, 20 years after its launch. The two focus groups include (a) children who were in-utero or in their initial years of life,

Posted by at 1:09 PM

Labels: Inclusive Growth

Saturday, February 19, 2022

Recent developments in housing markets and related policy challenges

Speech by Governor Constantinos Herodotou, Central Bank of Cyprus:

“The fact that not all euro area countries receive relevant warnings and recommendations by the ESRB is an indication that the Residential Market in the euro area is characterised by heterogeneity. In the upper right quartile of the chart, we find a number of countries that registered an accumulated increase in residential property prices of at least 25% in the last three years. Other countries have recorded accumulated growth as low as 5%.

Using as a starting point the observed heterogeneity and by analysing the experiences of several countries, we can draw certain broad conclusions on the effectiveness of the macroprudential toolbox.

The design of Borrower and Capital Based Measures is a decision of authorities. For example, based on information from the ESRB, Belgium introduced a Loan-to-Value on both owner-occupied and buy-to-let properties. Cyprus, in order to deal with a specific sectoral exposure, further to the Loan-to-Value cap, recently introduced an even stricter Loan-to-Value for luxurious properties. However, by observing the real estate cycles registered in a number of countries, it is evident that even the idiosyncratic design of these measures does not always stop real estate cycles from materialising. The Netherlands and Slovenia are examples of countries that have recorded vulnerabilities despite the implementation of such measures.

Analysis performed at the Central Bank of Cyprus verifies this observation.

Using an econometric model, we explain the growth rates of housing loans and house prices considering the implementation of macroprudential measures.

The analysis indicates that the Loan-to-Value ratio seems to be effective in containing housing loans, for 10 out of 12 countries in our sample and effective in containing house prices in only in 3 out of the 12 cases. Income based measures (such as Debt-Service-to-Income) and Capital Based Measures were found to be effective in around half of the countries that use them.

We can therefore conclude, that there is no “one-size-fits-all” type of macroprudential tool.

One of the reasons why macroprudential tools are not always effective, could be that vulnerabilities are not necessarily driven by the credit cycles. In the cases examined, it is evident, that credit for house purchases is not always correlated with the trends in housing prices. For example, Slovenia and the Netherlands experienced a build-up in vulnerabilities in the residential real estate market without a corresponding excessive growth in housing loans.

Structural factors could explain the above observation as they affect both demand and supply of housing. More particularly,

*Net migration and population growth are factors that have continued to put pressure on house prices in countries such as Luxembourg, which experienced net population growth of 13,6% in 2020. Countries with low vulnerabilities in the housing market, such as Greece, experienced a negative population growth.

*Strong preference for home ownership could also be a driving factor for the observed vulnerabilities in Luxembourg and Slovakia. Homeowners represent 92,9% of the population of Slovakia whereas in France, a country with low identified real estate vulnerabilities, homeowners represent 65,2%.

From the above examples, we can conclude that in designing a macroprudential tool, idiosyncratic structural factors need to be identified and accounted for.”

Monetary policy also plays a role. Although macroprudential policy is the first line of defence, the ECB has recognised that Financial Stability is a precondition for price stability. It has also been acknowledged that monetary policy, can, in principle, influence asset prices such as real estate.

(…)

To sum up, the euro area residential real estate market is characterised by heterogeneity. Vulnerabilities in the real estate market are not necessarily cyclical in nature but structural factors also play a role. A single policy or measure cannot be enough to tackle the materialisation of risks from the residential market, although macroprudential authorities, as the first line of defence, have a significant toolbox in their hands, that can help in containing these risks.”

Speech by Governor Constantinos Herodotou, Central Bank of Cyprus:

“The fact that not all euro area countries receive relevant warnings and recommendations by the ESRB is an indication that the Residential Market in the euro area is characterised by heterogeneity. In the upper right quartile of the chart, we find a number of countries that registered an accumulated increase in residential property prices of at least 25% in the last three years.

Posted by at 3:08 PM

Labels: Global Housing Watch

Friday, February 18, 2022

The Inaccuracy of Inflation Expectations

New post by Timothy Taylor on Conversable Economist posted on 17th February.

“The question of whether a burst of inflation turn into permanent inflation should depend, at least in part, on expectations about inflation. If workers and firms expect higher inflation, then the workers are more likely to press for higher wages to compensate–and firms are more likely to be amenable to such increases. An inflationary cycle can emerge where expectations of higher inflation lead to more price and wage increases, and those price and wage increases lead to higher inflation.”

Read more by clicking here.

New post by Timothy Taylor on Conversable Economist posted on 17th February.

“The question of whether a burst of inflation turn into permanent inflation should depend, at least in part, on expectations about inflation. If workers and firms expect higher inflation, then the workers are more likely to press for higher wages to compensate–and firms are more likely to be amenable to such increases. An inflationary cycle can emerge where expectations of higher inflation lead to more price and wage increases,

Posted by at 9:30 AM

Labels: Forecasting Forum

Housing View – February 18, 2022

On cross-country:

- ECB ‘cannot ignore’ house price surge in inflation assessment, says executive. Property boom adds to risks of acting too late to tighten monetary policy, says Isabel Schnabel – FT

- Surging housing costs boosting overall euro zone inflation: ECB – Reuters

- Watchdog sounds alarm on financial risks of Europe’s property boom. Banks at risk from soaring prices, loosening lending standards and rising household debt levels – FT and European Systemic Risk Board

- Germany and Austria told to curb boom in home prices – Reuters

- The true cost of empty offices. Property investors are sitting on big losses – The Economist

- The Economics Implications of House Price Capitalization: A Synthesis – London School of Economics

- Inflation may push more families to become Airbnb hosts, chief says. Lodging platform touts ‘economic opportunity’ while investors worry about limited supply as travel rebounds – FT

- Private Cities: Implications for Urban Policy in Developing Countries – World Bank

On the US:

- How to fix America’s broken housing systems – Brookings

- Housing Supply May Remain Constrained – Bloomberg

- Lacker on Rising Rates and Housing Market. Rising interest and mortgage rates will put a damper on housing demand, and also potentially on the supply of new homes, according to former Richmond Fed President Jeffrey Lacker. – Bloomberg

- Lessons from a Modern Master of Low-Rise Housing. Cities looking to boost density and affordability should look to the work of architect Louis Sauer, who designed stylish modernist housing in the 1960s and ’70s. – Bloomberg

- Why your rent is going up – Axios

- Renting a Home Is Even Harder Than Buying One in Unrelentingly Hot U.S. Market. Rental prices for single-family homes grew 7.8% in 2021, an all-time high, according to CoreLogic. – Bloomberg

- Blackstone expands further into rental housing in the United States. The private equity firm said it would acquire Preferred Apartment Communities, a real estate investment trust, for $6 billion as it seeks a hedge against inflation. – New York Times

- U.S. Housing Affordability Worsens. Median sales price for single-family existing homes was higher in fourth quarter versus year ago in 181 of 183 metro areas – Wall Street Journal

- Out-of-Town Home Buyers Will Pay 30% More Than Locals in Hottest U.S. Markets. In cities including Nashville, Philadelphia, Atlanta and Miami, people migrating from elsewhere are willing to pay way more than asking price. – Bloomberg

- Real-Estate Investors Head South, Bid Up Sunbelt Apartment Buildings. Dallas and Atlanta see more investment than other U.S. cities, as landlords chase job growth – Wall Street Journal

- Renters across US face sharp increases – averaging up to 40% in some cities. Americans face having to move or pay much bigger slice of income to stay in their homes as prices outstrip wages – The Guardian

- Remote Work Opens Up Cheaper Housing Options. House hunters are searching to move from expensive larger cities to smaller cheaper ones. – New York Times

- How the Federal Government’s policies are crowding out lower income Americans out of the housing market. And how federal agencies and regulators are in the process of doubling down on failed policies, putting low-income and minority borrowers needlessly in harm’s way – AEI

- Where Did All the Homes Go? Here Are the Cities With the Most Places for Sale—and the Ones With the Fewest – Realtor.com

- U.S. mortgage rates jump to two-year high, further squeezing buyers – Reuters

- San Francisco is the latest city to consider tackling its housing crisis by taxing empty homes – Quartz

- Amid a housing crisis, renters challenge firms they say are being exploitative – NPR

- With evictions on the rise, House Democrats team up to push new housing protections – NPR

- Natural disasters can wipe out affordable housing for years. And when communities lose affordable housing, it’s harder for businesses—and the entire economy—to recover from those disasters. – Fast Company

- Landmark housing discrimination settlement with Fannie Mae sets key precedent – Reuters

- Home prices: high, but not rising – FT

- Buying a Home Is as Frustrating as You Think It Is. Housing prices continue to skyrocket as potential buyers feel increasingly insecure about their personal finances. It’s easy to feel a little hopeless. – Bloomberg

- Is GSE Reform Dead? – Harvard Joint Center for Housing Studies

- Will Rising Rents Push Up Future Inflation? – San Francisco Fed

- Where in the US are homes most affordable? – Quartz

On China

- Chinese developers selling off more London property to raise cash. Shanghai-based Greenland is latest to exit with £40mn sale of Ram Brewery site – FT

On other countries:

- [Australia] Australian families are giving up on the suburban dream – but are new apartments up to the job? More and more Australians are likely to live in flats as the price of houses soars beyond their means. But design standards have allowed too many substandard blocks to go up – The Guardian

- [Australia] Major banks predict 14% drop in house prices. They’re wrong – Yahoo Finance

- [Australia] Land and Housing Supply Indicators. A summary of research undertaken by the ABS investigating indicators to measure the relationship between land-use regulation and housing supply – Australian Bureau of Statistics

- [Hong Kong] Hong Kong Home Sellers Cut Asking Prices as Covid Curbs Tighten – Bloomberg

- [New Zealand] New Zealand’s housing crisis is worsening. That is bad news for a government which promised miracles – The Economist

- [New Zealand] House prices continue to increase, slowdown expected – RNZ

- [New Zealand] New Zealand homes sales and prices ease in January – Reuters

- [New Zealand] Tighter lending among factors slowing house price growth – REINZ – RNZ

- [Netherlands] Complex Methods in Economics: An Example of Behavioral Heterogeneity in House Prices – Central Bank of Netherlands

- [South Korea] As house prices soar, ordinary South Koreans learn to love stocks. Asia’s fourth-largest economy is overcoming a historical aversion to financial assets and embracing the stock market. – Al Jazeera

- [United Kingdom] House Prices 30 Years Ago Determine Who Gets U.K. Energy Rebates. Britons are relying on arcane system to get 150 pounds of aid. Millions who don’t need help will be eligible for the relief – Bloomberg

- [United Kingdom] UK needs 230,000 new rental homes to meet growing demand. With more people renting for longer, UK will face a shortfall in private rented property, analysis shows – The Guardian

On cross-country:

- ECB ‘cannot ignore’ house price surge in inflation assessment, says executive. Property boom adds to risks of acting too late to tighten monetary policy, says Isabel Schnabel – FT

- Surging housing costs boosting overall euro zone inflation: ECB – Reuters

- Watchdog sounds alarm on financial risks of Europe’s property boom. Banks at risk from soaring prices, loosening lending standards and rising household debt levels – FT and European Systemic Risk Board

- Germany and Austria told to curb boom in home prices – Reuters

- The true cost of empty offices.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts