Wednesday, November 17, 2021

From recovery to expansion, amid headwinds: The Commission’s Autumn 2021 Forecast

From VoxEU.com by Maarten Verwey, Oliver Dieckmann, Przemyslaw Wozniak posted on 16 November 2021

“The growth outlook for the EU is for a continued economic expansion. With large shares of the population currently protected against severe COVID-19 cases and deaths (ECDC 2021), the EU economy is assumed to avoid lockdowns and to continue benefitting from the reopening momentum. As a result, the EU and the euro area, which were in the third quarter just a notch below their pre-pandemic output levels, are set to transition from recovery to expansion (Figure 1). This projection implies reaching the Commission’s extrapolated pre-pandemic forecast path within the forecast years, and approaching the pre-crisis growth trend much faster than after previous recessions. After the Global Financial Crisis in 2008-09, for example, it took the EU economy more than four years for just returning to the pre-crisis level of output. The atypical nature of the recession and the substantial policy support, including NGEU/RRF, were essential for this result.”

Continue reading here.

From VoxEU.com by Maarten Verwey, Oliver Dieckmann, Przemyslaw Wozniak posted on 16 November 2021

“The growth outlook for the EU is for a continued economic expansion. With large shares of the population currently protected against severe COVID-19 cases and deaths (ECDC 2021), the EU economy is assumed to avoid lockdowns and to continue benefitting from the reopening momentum. As a result, the EU and the euro area, which were in the third quarter just a notch below their pre-pandemic output levels,

Posted by at 9:57 AM

Labels: Forecasting Forum

Oil Price Futures and Forecasts

From Econbrowswer –

“Chinn and Coibion (2014) and subsequent analyses find futures do a fairly good job at prediction. Chinn and Coibion examined data up to 2012, for WTI, while Kwas and Rubszek (Forecasting, 2021) examined both WTI and Brent for 2000-March 2021. As noted in this post, futures improve upon a random walk for both RMSFE and direction of change at horizons up to a year.”

Continue reading here.

From Econbrowswer –

“Chinn and Coibion (2014) and subsequent analyses find futures do a fairly good job at prediction. Chinn and Coibion examined data up to 2012, for WTI, while Kwas and Rubszek (Forecasting, 2021) examined both WTI and Brent for 2000-March 2021. As noted in this post, futures improve upon a random walk for both RMSFE and direction of change at horizons up to a year.”

Posted by at 9:49 AM

Labels: Forecasting Forum

When Residential Real Estate Turned Commercial: Working from Home

From Conversable Economist:

“Everyone knows that lots of people have ended up working from home, either part-time or full-time, since the start of the pandemic. But I’m not sure many of us have appreciated how extraordinary that shift has been. In effect, an enormous amount of what economists would classify as “residential capital” was converted to commercial real estate almost overnight: that is, people used their places of residence along with capital that had often been installed at their place of residence mostly for other purposes (like entertainment) to do their work.

The size of the shift is remarkable. Janice C. Eberly, Jonathan Haskel and Paul Mizen discuss “Potential Capital: Working From Home, and Economic Resilience” (NBER Working Paper 29431, October 2021, subscription needed). They compare the drop in economic output from the workplace in the first two quarters of 2020 to the overall drop in economic output: in the US economy, for example, they find that output in the workplace fell by about 17%, but total economic output actually fell about 9%. Work done outside the conventional workplace made up the difference.

This built-in resilience of the economy may now seem pretty obvious, but it wasn’t obvious (at least to me) before the pandemic hit. The magnitudes here are enormous. According the US Bureau of Economic Analysis, the value of residential real estate in 2020 was almost $25 trillion. Privately owned nonresidential structures were worth almost $16 trillion, while the equipment in those structures was another $7 trillion. In short, trillions of dollars of residential capital replaced trillions of dollars of nonresidential capital in a very short time. The transition was far from seamless or painless, of course, but the fact that it happened at all is worth a gasp.”

Continue reading here.

From Conversable Economist:

“Everyone knows that lots of people have ended up working from home, either part-time or full-time, since the start of the pandemic. But I’m not sure many of us have appreciated how extraordinary that shift has been. In effect, an enormous amount of what economists would classify as “residential capital” was converted to commercial real estate almost overnight: that is, people used their places of residence along with capital that had often been installed at their place of residence mostly for other purposes (like entertainment) to do their work.

Posted by at 6:34 AM

Labels: Global Housing Watch

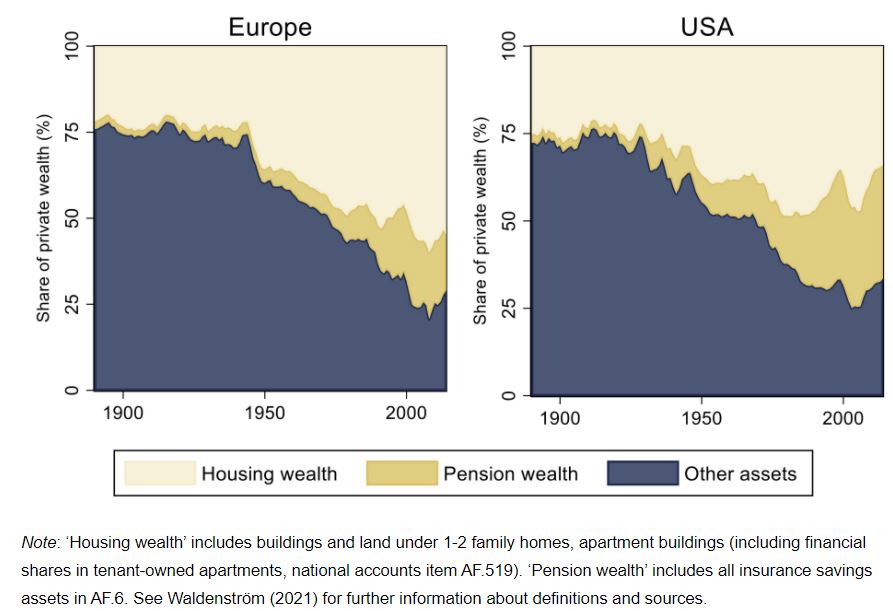

The post-war rise of popular wealth

From a VoxEU post by Daniel Waldenström:

“Since 1950, private wealth-income ratios have grown steadily around the Western world, accelerating after 1990. Figure 3 examines this development by decomposing private wealth into three asset groups: housing wealth, pension wealth, and other wealth.

The main result is that private wealth underwent a structural shift over the 20th century. Around 1900, wealth was dominated by agricultural estates and corporate wealth, assets predominantly held by the rich. During the post-war period, wealth accumulation came mainly in housing and funded pensions, which are assets held by ordinary people. This compositional trend had important distributional implications.”

Figure 3 Decomposing aggregate wealth-income ratios since 1890

Continue reading here.

From a VoxEU post by Daniel Waldenström:

“Since 1950, private wealth-income ratios have grown steadily around the Western world, accelerating after 1990. Figure 3 examines this development by decomposing private wealth into three asset groups: housing wealth, pension wealth, and other wealth.

The main result is that private wealth underwent a structural shift over the 20th century. Around 1900, wealth was dominated by agricultural estates and corporate wealth, assets predominantly held by the rich.

Posted by at 6:30 AM

Labels: Global Housing Watch

Tuesday, November 16, 2021

Macrofinancial Causes of Optimism in Growth Forecasts

New IMF Working paper by Yan Carrière-Swallow and José Marzluf

“We analyze the causes of the apparent bias towards optimism in growth forecasts underpinning the

design of IMF-supported programs, which has been documented in the literature. We find that

financial variables observable to forecasters are strong predictors of growth forecast errors. The

greater the expansion of the credit-to-GDP gap in the years preceding a program, the greater its

over-optimism about growth over the next two years. This result is strongest among forecasts that

were most optimistic, where errors are also increasing in the economy’s degree of liability

dollarization. We find that the inefficient use of financial information applies to growth forecasts more

broadly, including the IMF’s forecasts in the World Economic Outlook and those produced by

professional forecasters compiled by Consensus Economics. We conclude that improved

macrofinancial analysis represents a promising avenue for reducing over-optimism in growth

forecasts.”

New IMF Working paper by Yan Carrière-Swallow and José Marzluf

“We analyze the causes of the apparent bias towards optimism in growth forecasts underpinning the

design of IMF-supported programs, which has been documented in the literature. We find that

financial variables observable to forecasters are strong predictors of growth forecast errors. The

greater the expansion of the credit-to-GDP gap in the years preceding a program, the greater its

over-optimism about growth over the next two years.

Posted by at 4:26 PM

Labels: Forecasting Forum

Subscribe to: Posts