Monday, December 20, 2021

VIDEO: Discussing Global Recovery from the Pandemic with Gita Gopinath

The National Council of Applied Economic Research (NCAER) recently hosted Dr. Gita Gopinath, currently serving as the Chief Economist at the IMF for a discussion on the outlook for global growth in 2022. Among other things, the discussion touched upon topics like vaccination for protection against Covid-19, inflationary pressures in several countries, and the unique set of challenges before policymakers.

Watch the full video here.

The National Council of Applied Economic Research (NCAER) recently hosted Dr. Gita Gopinath, currently serving as the Chief Economist at the IMF for a discussion on the outlook for global growth in 2022. Among other things, the discussion touched upon topics like vaccination for protection against Covid-19, inflationary pressures in several countries, and the unique set of challenges before policymakers.

Watch the full video here.

Posted by at 9:12 AM

Labels: Inclusive Growth, Macro Demystified

Sunday, December 19, 2021

Where Can Residential Real Estate Investors Find the Most Potential ROI?

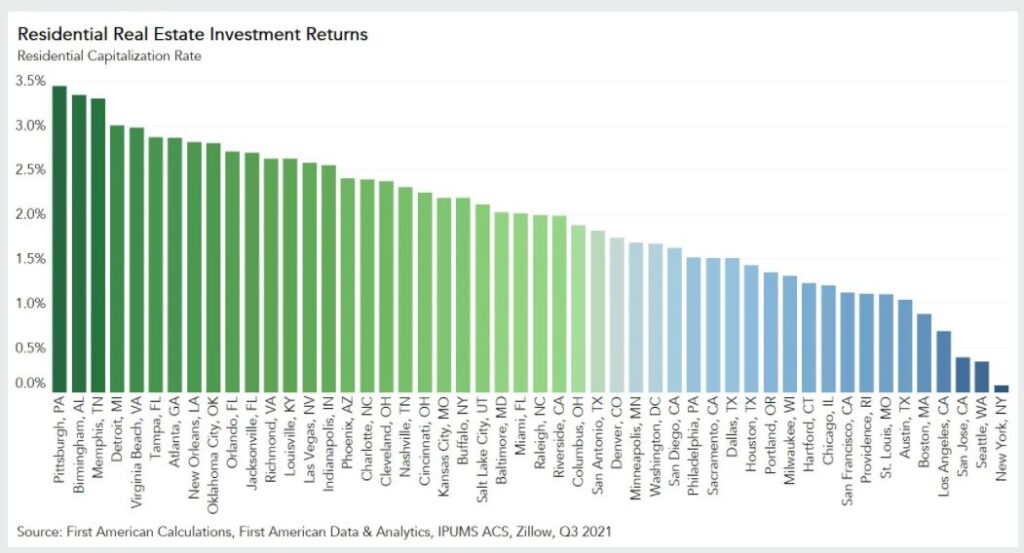

From First American:

“Over the past year, increasing investor activity in residential real estate, particularly in single-family homes, has drawn a lot of attention. News of large institutional investors snapping up single-family homes underscored this summer’s historically hot housing market. Investors now own an estimated 2 percent of single-family rental housing units in the U.S., but investor activity varies significantly across markets. Adapting a metric commonly used for measuring the return on investment for commercial real estate can help identify the most attractive markets for residential real estate investors.

Housing’s Investment Return

Investors in commercial real estate often use a concept called the capitalization rate (cap rate) to calculate their potential rate of return on a real estate investment. The cap rate measures the net operating income of a property – its rental income less any operating costs, such as property taxes, insurance, and maintenance and repair costs – compared to the value of the property. Similar to the yield on a bond or the rate of return on an investment, the higher the cap rate, the more profitable the investment. While commonly calculated for commercial real estate transactions, it can be applied to residential real estate as well.

To calculate the typical market-level residential cap rate, take the median residential market rent and assume that the property will be vacant for three of the 12 months of the year (the typical vacancy assumption mortgage lenders use when underwriting a residential investment property), leaving an investor with nine months of collected rent. After accounting for property costs – property taxes, maintenance costs and annual homeowner’s insurance premium – we are left with estimated total rental income. Dividing the estimated total rental income by the median home sale price in each market yields a residential cap rate.

Which Markets Offer the Highest Return?

Breaking down the cap rate for the median single-family home in each of the top 50 U.S. markets reveals the residential housing markets that are potentially the most profitable from a real estate investment perspective. Of the top 50 U.S. markets, the five markets with the highest cap rates in the third quarter of 2021 were Pittsburgh (3.4 percent), Birmingham, Ala. (3.3 percent), Memphis, Tenn. (3.3 percent), Detroit (3 percent), and Virginia Beach, Va. (3 percent). The five markets with the lowest cap rates were New York (0.1 percent), San Jose, Calif. (0.3 percent), San Francisco (0.4 percent), Los Angeles (0.7 percent), and Boston (0.9 percent).”

Continue reading here.

From First American:

“Over the past year, increasing investor activity in residential real estate, particularly in single-family homes, has drawn a lot of attention. News of large institutional investors snapping up single-family homes underscored this summer’s historically hot housing market. Investors now own an estimated 2 percent of single-family rental housing units in the U.S., but investor activity varies significantly across markets. Adapting a metric commonly used for measuring the return on investment for commercial real estate can help identify the most attractive markets for residential real estate investors.

Posted by at 9:14 AM

Labels: Global Housing Watch

Interview with Edward Glaeser on Urban Evolution

From Conversable Economist:

“David A. Price interviews Edward Glaeser, with the subheading “On urbanization, the future of small towns, and “Yes In My Back Yard” (Econ Focus, Federal Reserve Bank of Richmond, Fourth Quarter 2021, pp. 19-23). Here are a few comments that caught my eye.

On centripetal and centrifugal forces in cities

I see urban growth as almost uniformly a dance between technologies that pull us together and ones that push us apart.

Technologies of the 19th century, like the skyscraper — which is really the combination of a steel frame and an elevator — the streetcar, the steam engine, all of these things enabled the growth of 19th century cities. They brought people together. This was a centripetal age.

In the mid-20th century, we had technologies that were major jumps forward in transportation cost. In transportation technology, like the car, and in technology for transporting ideas and entertainment — television and radio — these were centrifugal forces that basically flattened the Earth and made it easier to live in far-flung suburbs or even rural areas. Those centrifugal technologies … were the backdrop for the exodus of people from dense cities that had been built around streetcars and subways and to suburbs that were built around the car.

But then in the late 20th century and early 21st century, the tides turned again. … We’ve started to see the electronic cottages become a force during the pandemic, and suburbanization has continued, but downtowns are vastly stronger than they were in the 1980s. And I think the primary reason is that globalization and new technologies have radically increased the returns to being smart, and we are a social species that gets smart by being around other smart people. That’s why people are willing to pay so much to be in the heart of Silicon Valley and why they’re willing to pay so much for downtown real estate in Chicago or New York or London.

On the shift to a rental market in single family homes

Traditionally, single-family homes were overwhelmingly owner-occupied in the U.S. More than 85 percent, I think, of homes were owner-occupied. The usual view of the housing economics community was that the agency problems involved in renting them out were huge. There are estimates that suggest that renting out for a year involves a 1 percent decline in the value of the house, or something like that, because the renter just doesn’t treat it properly. By contrast, traditionally more than 85 percent of multi-family housing was rented, at least once you get to over five stories. It’s much easier to manage a multi-unit building when you have one owner. One roof, one owner, because otherwise you’ve got the problems of coordination of the condo association or the co-op board, which can be more fractious.

So those were the things, I think, that were responsible for tying ownership type and structure type so closely together. We are starting to see that break down, which is quite interesting. I don’t know if these buyers have fully internalized their difficulties with the maintenance that goes into rental houses as a long-run issue. Or if technology has changed in such a way that they think that they can actually solve that agency problem and that they can figure out ways to deal with the maintenance costs in some efficient fashion. I’m happy to see an emergence of a healthy rental market in single-family detached housing, but I’m keenly aware of the limitations and difficulties of doing that. So, we’ll have to see how this plays out. I can’t help thinking some part of it just has to be that investors are simply searching for new investment products.”

Continue reading here.

From Conversable Economist:

“David A. Price interviews Edward Glaeser, with the subheading “On urbanization, the future of small towns, and “Yes In My Back Yard” (Econ Focus, Federal Reserve Bank of Richmond, Fourth Quarter 2021, pp. 19-23). Here are a few comments that caught my eye.

On centripetal and centrifugal forces in cities

I see urban growth as almost uniformly a dance between technologies that pull us together and ones that push us apart.

Posted by at 7:49 AM

Labels: Global Housing Watch

Saturday, December 18, 2021

Reversing the Pandemic’s Education Losses

David Malpass, President of the World Bank Group, and Henrietta H Fore, Executive Director of UNICEF write about mitigating educational challenges of the Covid-19 pandemic in a recent opinion piece (December 2021) for Project Syndicate. Excerpts from the article:

“According to World Bank estimates, pandemic-related school closures could drive up “learning poverty” – the share of 10-year-olds who cannot read a basic text – to around 70% in low- and middle-income countries. This learning loss could cost an entire generation of schoolchildren $17 trillion in lifetime earnings. Throughout the pandemic, marginalized children have struggled the most. When classrooms around the world reopened this fall, it became clear that these children had fallen even further behind their peers. Before the pandemic, gender parity in education was improving. But school closures placed an estimated ten million more girls at risk of early marriage, which practically guarantees the end of their schooling.”

Further, they discuss prospects for higher investment in education, some best practices, and access to digital learning as a “great equalizer”.

Click here to read the full article.

David Malpass, President of the World Bank Group, and Henrietta H Fore, Executive Director of UNICEF write about mitigating educational challenges of the Covid-19 pandemic in a recent opinion piece (December 2021) for Project Syndicate. Excerpts from the article:

“According to World Bank estimates, pandemic-related school closures could drive up “learning poverty” – the share of 10-year-olds who cannot read a basic text – to around 70% in low- and middle-income countries. This learning loss could cost an entire generation of schoolchildren $17 trillion in lifetime earnings.

Posted by at 10:47 AM

Labels: Inclusive Growth

Buildings key to achieving Europe’s climate goals

From Social Europe:

“There are fears the revised directive on energy performance due from the European Commission will not be adequate to the task.

The revision of the Energy Performance of Buildings Directive (EPBD), expected from the European Commission today, as part of the Fit for 55 package, is a legislative milestone which cannot go under the radar.

In the bloc’s effort to achieve climate neutrality and fulfil its international climate commitments, the building sector has a systemic role to play. The EPBD is the main policy instrument regulating buildings across the European Union.

Since its first adoption in 2002, the legislation has been key to improving the energy performance of the European building stock, by fostering energy efficiency and aiming at long-term decarbonisation. But given the need to take decisive action in this decade to tackle the climate emergency, the time has come for a comprehensive revision, to fill gaps and raise ambition.

Profound transformations are urgently needed to decarbonise buildings, ensuring that the sector contributes to the efforts to limit temperature rise to 1.5C. Indeed, the homes and offices which surround us today are among the main culprits of the climate crisis, accounting for around 40 per cent of all energy consumed and 36 per cent of energy-related greenhouse-gas emissions in the EU.”

Continue reading here.

From Social Europe:

“There are fears the revised directive on energy performance due from the European Commission will not be adequate to the task.

The revision of the Energy Performance of Buildings Directive (EPBD), expected from the European Commission today, as part of the Fit for 55 package, is a legislative milestone which cannot go under the radar.

In the bloc’s effort to achieve climate neutrality and fulfil its international climate commitments,

Posted by at 7:15 AM

Labels: Global Housing Watch

Subscribe to: Posts