Friday, March 13, 2020

Housing View – March 13, 2020

On cross-country:

- Europe’s great house price boom continues, but sharp slowdown in North America, the Middle East and most of Asia-Pacific – Global Property Guide

- World’s priciest homes: How Australian house prices compare to the rest of the world – RealEstate

On the US:

- Urbanization and its Discontents – NBER

- The housing affordability crisis is a reality: Lawmakers need to act, but responsibly – The Hill

- Real Estate and the Wealth of a Nation – American Institute for Economic Research

- Housing Finance At A Glance: A Monthly Chartbook, February 2020 – Urban Institute

- However You Measure It, Parents of White College Graduates Are about 10 Times Wealthier Than Their Black Counterparts – Urban Institute

- The Termination of LIBOR An Update on Implications for the Mortgage Market – Urban Institute

- Institutional Investors Brought Higher Home Prices and Lower Vacancies to the Housing Recovery – Urban Institute

- Five Facts about Our Housing Supply Explain High Rents and Home Prices – Urban Institute

- Is housing a better investment than education? – Quartz

- Plunging Mortgage Rates Might Not End U.S. Housing Doldrums – Wall Street Journal

- Coronavirus Looms Over Crucial Spring Season for Housing Market – Wall Street Journal

On other countries:

- [Germany] Capital Flows, Real Estate, and Local Cycles: Evidence from German Cities, Banks, and Firms – NBER

- [Hong Kong] Hong Kong’s housing market remains resilient – Global Property Guide

- [Lithuania] Lithuania’s house price continues to rise – Global Property Guide

- [Mexico] Mexico’s housing market remains robust – Global Property Guide

- [Romania] Romania’s housing market continues to grow – Global Property Guide

- [Russia] Russia’s housing market getting better – Global Property Guide

- [Thailand] Thailand’s house prices continue to rise – Global Property Guide

On cross-country:

- Europe’s great house price boom continues, but sharp slowdown in North America, the Middle East and most of Asia-Pacific – Global Property Guide

- World’s priciest homes: How Australian house prices compare to the rest of the world – RealEstate

On the US:

- Urbanization and its Discontents – NBER

- The housing affordability crisis is a reality: Lawmakers need to act,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, March 6, 2020

Operationalizing Inclusive Growth: Per-Percentile Diagnostics to Inform Redistribution Policies

A new IMF working paper by Alexei Kireyev and Andrei Leonidov;

“Inclusive growth, narrowly defined in this paper as growth that helps reduce inequality, is achieved if consumption of the poor increases faster than consumption of the rich. The paper presents a simple accounting framework for a per-percentile consumption diagnostics that could inform redistribution policies. The proposed framework is illustrated in application to Iraq and Tunisia.”

A new IMF working paper by Alexei Kireyev and Andrei Leonidov;

“Inclusive growth, narrowly defined in this paper as growth that helps reduce inequality, is achieved if consumption of the poor increases faster than consumption of the rich. The paper presents a simple accounting framework for a per-percentile consumption diagnostics that could inform redistribution policies. The proposed framework is illustrated in application to Iraq and Tunisia.”

Posted by at 4:52 PM

Labels: Inclusive Growth

Housing View – March 6, 2020

On cross-country:

- Decoding the New Housing Reality – Housing Europe

On the US:

- The Great Wall Street Housing Grab – New York Times

- How the Democratic Candidates Would Tackle the Housing Crisis – New York Times

- How Bloomberg, Sanders and Warren Responded to a Survey on Housing – New York Times

- Evidence Shows Military Service Reduces the Racial Homeownership Gap – Urban Institute

- Why Do Black College Graduates Have a Lower Homeownership Rate Than White People Who Dropped Out of High School? – Urban Institute

- Reverse Mortgage Use Differs by Race and Ethnicity. Here’s Why It Matters – Urban Institute

- Is the Sudden Increase in Black Homeownership Too Good to Be True? – Urban Institute

- Breaking Down the Black-White Homeownership Gap – Urban Institute

- Vacant “Zombie” Foreclosures Increase to 3.1 Percent Nationwide – ATTOM

- For Those Living in Public Housing, It’s a Long Way to Work – Citylab

- Housing Discrimination and Pollution Exposures in the United States – NBER

- Does Information About Climate Risk Affect Property Values? – NBER

- Vote Warren for a Pro-Housing President – Harvard Political Review

- Digging Deeper into the Story: The Widespread Implications of the Growth in High Income Renters on Low- and Middle-Income Renter Households – Harvard Joint Center for Housing Studies

On other countries:

- [Chile] Property prices in Chile continue to rise – Global Property Guide

- [Ireland] Ireland’s central banker warns on homes spending spree – Financial Times

- [Slovak Republic] Slovak Republic’s house price rising continuously – Global Property Guide

On cross-country:

- Decoding the New Housing Reality – Housing Europe

On the US:

- The Great Wall Street Housing Grab – New York Times

- How the Democratic Candidates Would Tackle the Housing Crisis – New York Times

- How Bloomberg, Sanders and Warren Responded to a Survey on Housing – New York Times

- Evidence Shows Military Service Reduces the Racial Homeownership Gap – Urban Institute

- Why Do Black College Graduates Have a Lower Homeownership Rate Than White People Who Dropped Out of High School?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, March 5, 2020

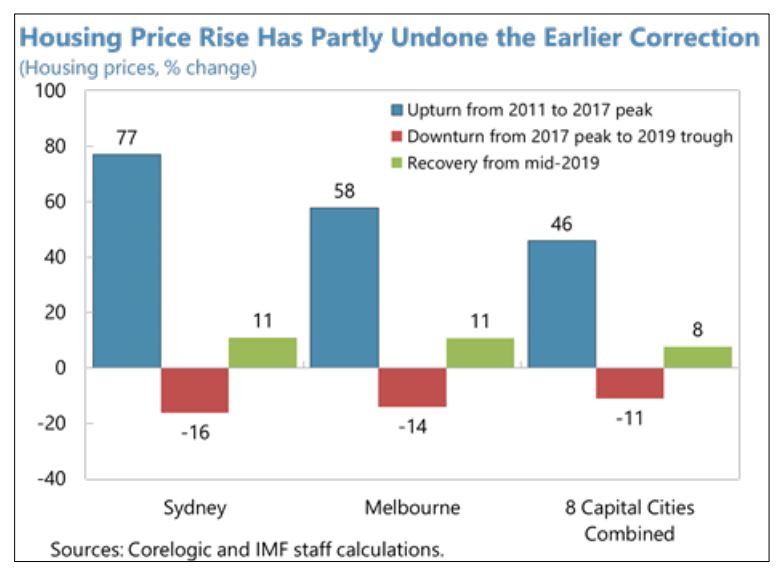

House Prices in Australia

From the IMF’s latest report on Australia:

“The fast increase in housing prices since mid-2019 has partly undone earlier price declines. As such, despite lower mortgage rates, there has only been a limited improvement in housing affordability for many households since the peak in housing prices in 2017.

Staff’s Views

Housing supply reforms are critical for restoring affordability. More efficient long-term planning, zoning, and local government reforms that promote housing supply growth, along with a focus on infrastructure development, remain critical to meet the needs of a growing urban population. Initiatives such as “City and Regional Deals” that aim to integrate transport, housing and land use polices to create the opportunity for coordinated action to maximize the value of infrastructure investment, should help meet growing demand for housing.

Broader tax reforms could reinforce the effectiveness of supply-side measures. Transitioning from a housing transfer stamp duty to a general land tax would improve efficiency by easing entry into the housing market and promoting labor mobility, while providing a more stable revenue source for the states. Such reforms could be complemented by reducing structural incentives for leveraged investment by households, including limiting negative gearing in residential real estate. Nonetheless, major changes affecting investment decisions and underlying demand for housing should be gradual, and such reforms should not be undertaken in isolation. In addition, housing policy measures discriminating against nonresidential buyers, such as state-level foreign purchaser duty surcharges on residential property, should be replaced by alternative, non-discriminatory measures, such as a general surcharge on vacant property or surcharges on all investor-owned housing transactions.

Authorities’ Views

The authorities saw potential risks linked to a possible reemergence of rapid housing price growth. With population growth projected to remain strong, the ongoing weakness in building approvals following the past decline in housing prices and tighter credit supply for developers could result in a shortage of new housing and renewed rapid housing price growth, with the risk that this would, in turn, lead to stronger growth in household debt.

The authorities stressed that they would continue to facilitate housing supply reforms and other measures to improve housing affordability. They highlighted that the Commonwealth government provides annual housing-related funding such as rental subsidy for individuals through the Commonwealth Rent Assistance (CRA), funding to states and territories to improve Australians’ access to affordable housing through the National Housing and Homelessness Agreement (NHHA), and the First Home Loan Deposit Scheme to provide loan guarantee to lenders for first-time home buyers. Housing has also been a priority in the City and Regional Deals. The authorities thought that tax policy was not the right tool to address potential speculative behavior in housing markets, as negative gearing applies across investments and investments in residential housing are relatively highly taxed, and that macroprudential policy should instead be employed as needed.”

From the IMF’s latest report on Australia:

“The fast increase in housing prices since mid-2019 has partly undone earlier price declines. As such, despite lower mortgage rates, there has only been a limited improvement in housing affordability for many households since the peak in housing prices in 2017.

Staff’s Views

Housing supply reforms are critical for restoring affordability. More efficient long-term planning, zoning, and local government reforms that promote housing supply growth,

Posted by at 5:39 PM

Labels: Global Housing Watch

Monday, March 2, 2020

Transitory and Permanent Shocks in the Global Market for Crude Oil

From a new IMF working paper by Nooman Rebei and Rashid Sbia:

“This paper documents the determinants of real oil price in the global market based on SVAR model embedding transitory and permanent shocks on oil demand and supply as well as speculative disturbances. We find evidence of significant differences in the propagation mechanisms of transitory versus permanent shocks, pointing to the importance of disentangling their distinct effects. Permanent supply disruptions turn out to be a bigger factor in historical oil price movements during the most recent decades, while speculative shocks became less influential.”

From a new IMF working paper by Nooman Rebei and Rashid Sbia:

“This paper documents the determinants of real oil price in the global market based on SVAR model embedding transitory and permanent shocks on oil demand and supply as well as speculative disturbances. We find evidence of significant differences in the propagation mechanisms of transitory versus permanent shocks, pointing to the importance of disentangling their distinct effects. Permanent supply disruptions turn out to be a bigger factor in historical oil price movements during the most recent decades,

Posted by at 10:24 AM

Labels: Energy & Climate Change

Subscribe to: Posts