Wednesday, January 16, 2019

Special Issue: The Appropriate Role of Government in U.S. Mortgage Markets

From the Federal Reserve Bank of New York:

“A decade after the financial crisis, the U.S. mortgage finance system remains largely untouched by legislative reforms. Policy deliberations have focused on Fannie Mae and

Freddie Mac—the two enormous government-sponsored enterprises (GSEs) that were placed into federal conservatorship in September 2008. The conservatorships were initially thought of as a temporary arrangement during which U.S. mortgage markets could be stabilized and function as intended, while providing time for Congress to consider the appropriate long-term federal role in the secondary mortgage market. To date, however, legislators have yet to resolve some basic issues: Should government guarantees continue to be available for a large swath of loans? If so, what types of institutions should have direct access to guarantees and how would their access be facilitated and regulated?This special issue of the Federal Reserve Bank of New York’s Economic Policy Review presents a set of articles that developed from presentations given at “The Workshop on the Appropriate Government Role in U.S. Mortgage Markets,” held at the Bank on April 27-28, 2017. The workshop was organized in association with the Board of Governors, the Federal Reserve Bank of Atlanta, the Anderson School of Management at the University of California–Los Angeles, and the Wharton School of the University of Pennsylvania. We emphasize at the outset that the opinions expressed in the articles are those of the authors and do not necessarily reflect the views of any of the organizing institutions. In this introduction, we provide some context for the workshop and highlight the articles’ key findings.”

Introduction

W. Scott Frame and Joseph TracyGSE Guarantees, Financial Stability, and Home Equity Accumulation

Wayne Passmore and Alexander H. von HafftenThe FHA and the GSEs as Countercyclical Tools in the Mortgage Markets

Wayne Passmore and Shane M. SherlundPricing Government Credit: A New Method for Determining Government Credit Risk Exposure

Brent W. Ambrose and Zhongyi YuanPeas in a Pod? Comparing the U.S. and Danish Mortgage Finance Systems

Jesper Berg, Morten Bækmand Nielsen, and James VickeryCredit Risk Transfer and De Facto GSE Reform

David Finkelstein, Andreas Strzodka, and James VickeryCredit Risk Transfer, Informed Markets, and Securitization

Susan M. WachterHousing Affordability: Recommendations for New Research to Guide Policy

Jane DokkoLong-Term Outcomes of FHA First-Time Homebuyers

Donghoon Lee and Joseph Tracy

From the Federal Reserve Bank of New York:

“A decade after the financial crisis, the U.S. mortgage finance system remains largely untouched by legislative reforms. Policy deliberations have focused on Fannie Mae and

Freddie Mac—the two enormous government-sponsored enterprises (GSEs) that were placed into federal conservatorship in September 2008. The conservatorships were initially thought of as a temporary arrangement during which U.S. mortgage markets could be stabilized and function as intended, while providing time for Congress to consider the appropriate long-term federal role in the secondary mortgage market.

Posted by at 11:21 AM

Labels: Global Housing Watch

Resource Booms and the Macroeconomy: The Case of U.S. Shale Oil

A new working paper by Nida Cakir Melek, Michael Plante, Mine K. Yucel:

“We examine the implications of the U.S. shale oil boom for the U.S. economy, trade balances, and the global oil market. Using comprehensive data on different types of crude oil, and a two-country general equilibrium model with heterogenous oil and refined products, we show that the shale boom boosted U.S. real GDP by 1 percent and improved the oil trade balance as a share of GDP by more than 1 percentage points from 2010 to 2015. The boom led to a decline in oil and fuel prices, and a dramatic fall in U.S. light oil imports. In addition, we find that the crude oil export ban, which was in place during a large part of this boom, was a binding constraint, and would likely have remained a binding constraint thereafter had the policy not been removed at the end of 2015.”

A new working paper by Nida Cakir Melek, Michael Plante, Mine K. Yucel:

“We examine the implications of the U.S. shale oil boom for the U.S. economy, trade balances, and the global oil market. Using comprehensive data on different types of crude oil, and a two-country general equilibrium model with heterogenous oil and refined products, we show that the shale boom boosted U.S. real GDP by 1 percent and improved the oil trade balance as a share of GDP by more than 1 percentage points from 2010 to 2015.

Posted by at 11:02 AM

Labels: Energy & Climate Change

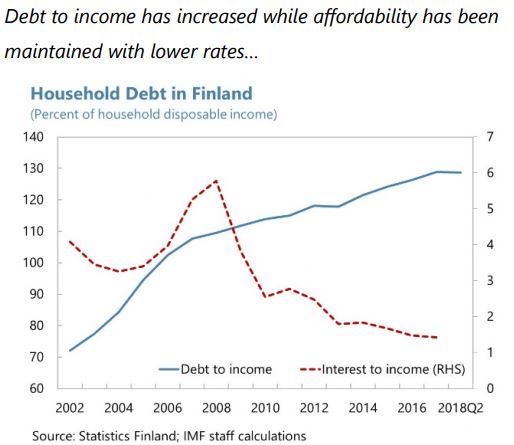

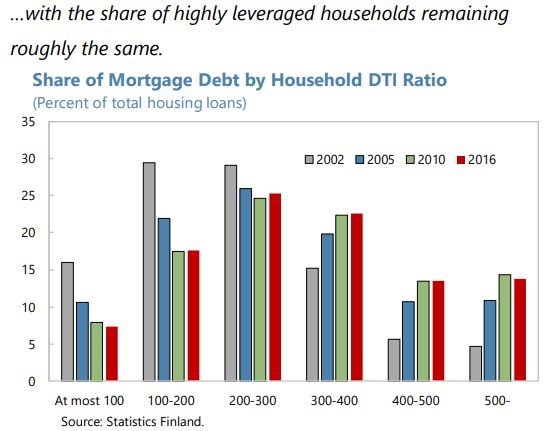

Housing Market in Finland

The IMF’s latest report on Finland says:

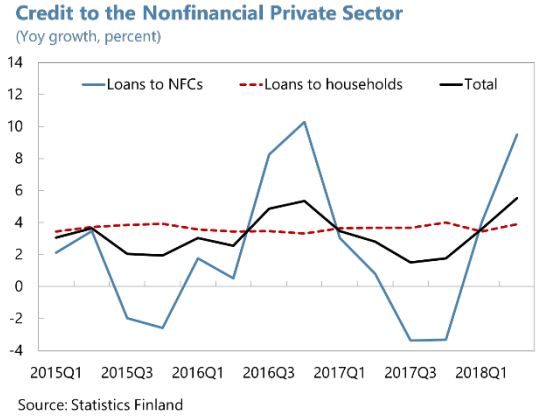

“Credit has expanded moderately overall, but housing corporation loans and consumer credit have been rising more rapidly. Total loan growth to the private nonfinancial sector has remained broadly constant at around 3½ percent for the past five years. Most lending to households has been in the form of secured lending for housing, which has grown around 4 percent. Corporate loan growth has rebounded strongly in the second quarter of the year after a sharp contraction in the second half of 2017. Two lending categories stand out:

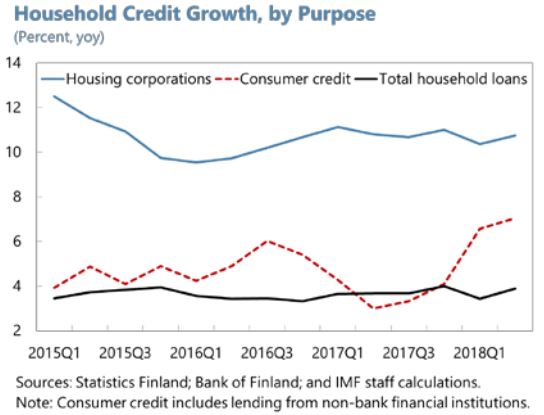

Loans to housing corporations have been expanding rapidly—above 10 percent—for many years. The drivers—expansion of the housing stock and renovation of rental properties—are

healthy. But the shareholders of housing corporations include homeowners, making these de facto indirect loans to households, and households might thereby be tempted to take on more debt than can easily be repaid.Consumer credit has been increasing steadily—above 7 percent y/y in the second quarter of 2018—and now accounts for 12 percent of aggregate household debt, driven by credit

institutions easing lending standards and a rapid increase in non-bank lending. The expansion has been associated with an increase in payment defaults.Household debt has been increasing steadily, despite the increase in real disposable incomes. Saving rates are lower than peers, although some of the difference is attributable to Finland’s public pension system. Household debt remains lower than Nordic peers, but is expected to increase further. Highly-indebted households (i.e. those with debt greater than four times their income) accounted for over a quarter of borrowing in 2016; preliminary survey data for 2017 indicate that the typical new borrower for housing purchases is taking on leverage of 4½ times income. The share of floating rate loans in household lending is high, exacerbating households’ vulnerabilities to interest rate and/or income shocks, although this is mitigated by the prevalence of mortgages with annuity repayments.

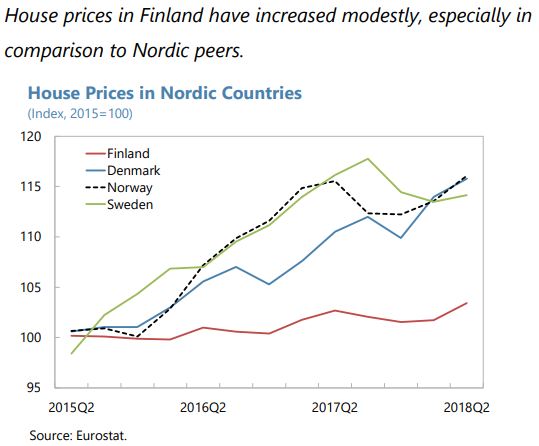

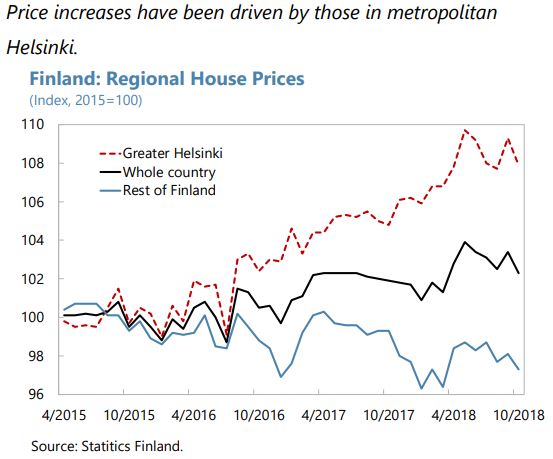

Residential real estate markets do not seem overheated overall, but demand still exceeds supply in major metropolitan areas, and commercial real estate may expose the economy to shocks. Housing starts and completions have been elevated, but price increases in greater Helsinki suggest demand still outstrips supply. Across the whole country, house price increases have been modest, especially in comparison to Nordic peers, with house price deflation in regions outside greater Helsinki. Price-to-income and price-to-rent ratios have not risen much during the recent economic recovery. Low and declining yields in commercial real estate suggest relatively high valuations.

The authorities have tightened credit policies. A floor of 15 percent on the average risk weight for housing loans took effect in January for institutions using internal risk-based (IRB) models. Effective July, the maximum loan-to-collateral (LTC) ratio for housing loans (excluding loans on first homes) was cut from 90 to 85 percent.

The recent tightening is appropriate, but policy could be more effective if the toolkit were modified. Although overall household debt and leverage are not high in comparison with other Nordic countries, there are some cohorts that are increasingly vulnerable to income and/or interest rate shocks—which, in view of the concentration of total lending in real estate, opens the financial system to risks.

The current cap on mortgage loans relative to collateral could usefully be replaced with a cap relative to the value of the property, as is common in other countries. And because the

underlying problem is more the level of debt than housing valuations, it would be useful for the authorities to have debt-based macroprudential tools (such as debt-to-income or debt-service to-income caps) at their disposal should leverage become more stretched. Applying such tools well depends on accurate information. Staff supports the recent Justice Ministry recommendation for the establishment of a “positive credit register”—i.e. a database that credit firms and the FINFSA could use to obtain real-time information about customers’ debt and income levels. A new challenge arises from non-bank lending, including online platforms such as peer-to-peer lending, which is not being recorded in credit statistics and registers.The growing reliance on consumer credit, especially that provided by non-banks and via digital platforms, raises additional concerns. Some of these outlets are not regulated and provide cross border financing. Attempts were made to circumvent legally-binding interest rate caps, raising the question of whether borrowers—especially those dealing with non-bank lenders—are sufficiently informed about the conditions of their loans. The authorities are amending the legislation on interest rate caps to close loopholes. Additional consumer protection measures are needed and require more data collection, especially on consumer lending provided through digital platforms. Tighter prudential requirements to demonstrate creditworthiness could also be considered.

Macroprudential authority tools should not be expected to solve underlying supply problems. The authorities have already implemented measures to expand housing supply in urban areas, including Helsinki. The government provides considerable support for social housing, which should make it easier to move across regions. But property taxation could be deterring mobility: recurrent property taxes collected by municipalities tend to be low, with some exceptions, while transaction tax rates are steeper at 4 percent.”

The IMF’s latest report on Finland says:

“Credit has expanded moderately overall, but housing corporation loans and consumer credit have been rising more rapidly. Total loan growth to the private nonfinancial sector has remained broadly constant at around 3½ percent for the past five years. Most lending to households has been in the form of secured lending for housing, which has grown around 4 percent. Corporate loan growth has rebounded strongly in the second quarter of the year after a sharp contraction in the second half of 2017.

Posted by at 10:56 AM

Labels: Global Housing Watch

Tuesday, January 15, 2019

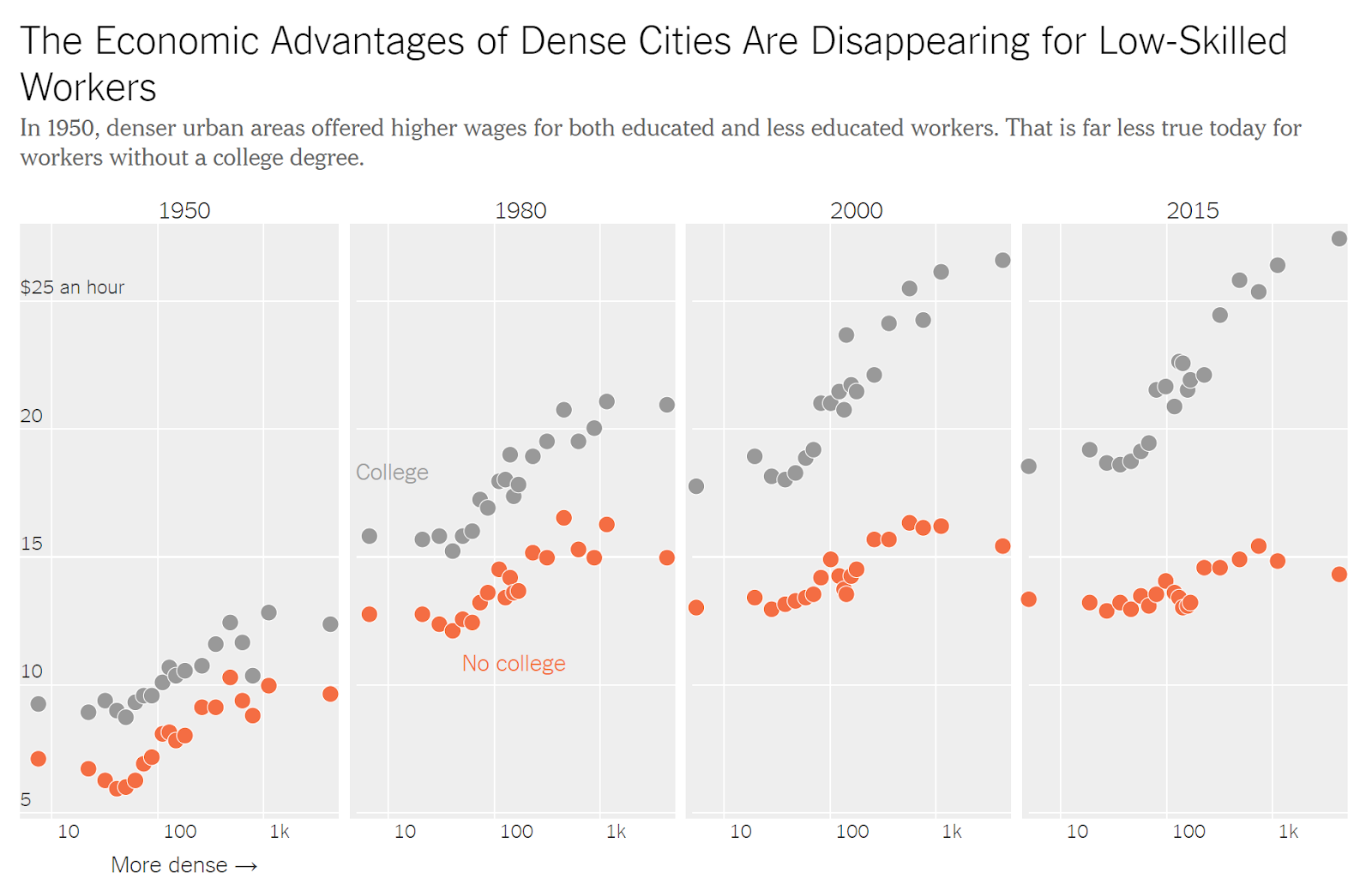

The Key to Gentrification

From EconoSpeak:

“In the world of urban politics, there is probably no more potent populist rallying cry than the demand to halt gentrification. Activists have fought it on multiple fronts: zoning, development subsidies, permitting, rent control—every lever housing policies afford. But what if they’re mistaking cause for effect, hacking away at the visible manifestations of the problem while leaving the problem itself intact?

Pivot to an important article in today’s New York Times, reporting on recent research David Autor of MIT presented at the economics meetings in Atlanta earlier this month. It’s all summed up in this set of charts:

As you can see from the tiny print at the top, the data are being read horizontally within each chart, from less dense regions (rural areas) on the left to high density cities on the right. The question being asked in the article is, if you live in a rural area or a small town, how much benefit can you get from moving to a big city? In the early post-WWII period, the answer was “a lot” for both the majority holding only a high school diploma and the few with a college BA. By 2015 the situation had changed: it was still a good move for college grads but there was little to be gained by those with only a high school education—and probably even less when you factor in the increased cost of living. That’s an interesting story.

But there’s another way to read these charts, vertically, comparing wage gaps at any particular time and place between these two education-defined groups. In 1950 the gap was relatively small; in the densest cities the college crowd made about 30% more per hour than the high schoolers. By 2015 they made almost twice as much. And don’t forget that the rise of inequality is virtually fractal: similar gaps have opened up within the top 20%, and within the top 5%, 1% and .01%. The whole rightward tail of the distribution has elongated, pulling ever further from the median.”

Continue reading here.

From EconoSpeak:

“In the world of urban politics, there is probably no more potent populist rallying cry than the demand to halt gentrification. Activists have fought it on multiple fronts: zoning, development subsidies, permitting, rent control—every lever housing policies afford. But what if they’re mistaking cause for effect, hacking away at the visible manifestations of the problem while leaving the problem itself intact?

Pivot to an important article in today’s New York Times,

Posted by at 10:46 AM

Labels: Global Housing Watch, Inclusive Growth

Chart of the day…. or century?

Posted by at 10:36 AM

Labels: Macro Demystified

Subscribe to: Posts