Monday, January 28, 2019

A Comparison of Alternative Programs for Climate Policies

From a new paper by Tarek Atalla, Simona Bigerna and Carlo Andrea Bollino:

“In the global carbon policy debate, pricing is considered to be a key instrument to achieving the desired levels of emissions reductions.

The Pigouvian tax is theoretically the best solution to tax carbon emissions, in order to achieve emissions reduction through financial investment, but it has not proved to be politically viable. A Pigouvian tax sets out to correct negative externalities, or consequences for society – such as the consequences of climate change – by levying additional taxes. However, from the viewpoint of the private sector, such taxation imposes a deadweight loss with respect to the original private equilibrium. This generates political resistance that may impede achieving the theoretical optimal solution.

Most international policy meetings since the Kyoto Protocol agreement have resulted in lukewarm commitments from developed economies and strong resistance from emerging economies over the fair economic allocation of the burden associated with the various calls for emissions reduction. This kind of situation suggests the need for alternative formulations, in the realm of what economists call ‘second-best options,’ to tackle the issue of realistically financing alternative policies.

This paper considers alternative policy formulation aimed at funding investment for climate policies, based on the principle of minimizing deadweight losses associated with taxation and on consumer preferences. (A deadweight loss is the added burden placed on consumers and suppliers when the market equilibrium is altered because of tax, for example. It results when supply and demand are out of equilibrium.)

The policy proposal we examine here is a Ramsey allocation, which aims at designing an economically optimal taxation scheme for financing climate mitigation investments. A Ramsey pricing policy, applied to energy prices, would mean that efficient taxation should be inversely proportional to the consumer (household) energy demand elasticity of the individual country. In other words, the more inelastic a country’s consumer energy demand, the higher the efficient taxation should be in that country. The overall taxation scheme is optimal because it minimizes the deadweight loss.

This strategy is not aimed at directly reducing emissions, and hence energy consumption. It can, in a more general way, help to assist with providing efficient funding for a wider range of policies, such as carbon sequestration, alternative fuels, energy efficiency, and the earth’s albedo enhancing. In this framework, notice that carbon sequestration and artificially enhancing the earth’s albedo represent technological solutions aimed at reducing carbon dioxide (CO2) concentration and adding sunlight reflecting aerosol in the soil

or stratosphere, thereby cooling the climate in a different way than reducing carbon emissions (NAS 1992). The strategy makes explicit use of household preferences, as expressed through their energy demand behavior, econometrically estimated at the world level.A Ramsey allocation can be integrated into the general principle of mutual cooperation that motivates climate agreements, as it reflects a common but differentiated burden of all parties.”

From a new paper by Tarek Atalla, Simona Bigerna and Carlo Andrea Bollino:

“In the global carbon policy debate, pricing is considered to be a key instrument to achieving the desired levels of emissions reductions.

The Pigouvian tax is theoretically the best solution to tax carbon emissions, in order to achieve emissions reduction through financial investment, but it has not proved to be politically viable. A Pigouvian tax sets out to correct negative externalities,

Posted by at 9:46 AM

Labels: Energy & Climate Change

Commodity Terms of Trade: A New Database

From a new IMF working paper by Bertrand Gruss and Suhaib Kebhaj:

“This paper presents a comprehensive database of country-specific commodity price indices for 182 economies covering the period 1962-2018. For each country, the change in the international price of up to 45 individual commodities is weighted using commodity-level trade data. The database includes a commodity terms-of-trade index which proxies the windfall gains and losses of income associated with changes in world price as well as additional country-specific series, including commodity export and import price indices. We provide indices that are constructed using, alternatively, fixed weights (based on average trade flows over several decades) and time-varying weights (which can account for time variation in the mix of commodities traded and the overall importance of commodities in economic activity). The paper also discusses the dynamics of commodity terms of trade across country groups and their influence on key macroeconomic aggregates.”

From a new IMF working paper by Bertrand Gruss and Suhaib Kebhaj:

“This paper presents a comprehensive database of country-specific commodity price indices for 182 economies covering the period 1962-2018. For each country, the change in the international price of up to 45 individual commodities is weighted using commodity-level trade data. The database includes a commodity terms-of-trade index which proxies the windfall gains and losses of income associated with changes in world price as well as additional country-specific series,

Posted by at 9:39 AM

Labels: Energy & Climate Change

Friday, January 25, 2019

Ukraine: Residential Property Price Index

The IMF’s latest report on Ukraine:

“A technical assistance (TA) mission was conducted during June 18–22, 2018 to support the State Statistics Service of Ukraine (SSSU) in improving the residential property price indexes (RPPI) for Ukraine. This was the second of a series of SECO2 RPPI-funded TA missions to take place until mid-2019 that will assist in building staff capacity for further development of the RPPI. RPPIs have been identified as critical ingredients for financial stability policy analysis. The indexes are used by policy makers as an input into design of macroprudential policies, that is, those policies aim to reduce systemic risks arising from “excessive” financial procyclicality (such as asset bubbles). RPPIs are also used by policy makers to inform monetary policy and inflation targeting.

In line with the recommendations from the previous mission, and ahead of schedule, an experimental overall national RPPI has been compiled. The authorities have used administrative data on the size of properties registered, combined with a survey covering the construction of new homes, to estimate the relative sizes of primary and secondary markets. The estimated weights remain susceptible to outliers, in particular, errors in the size registered. The SSSU should continue to work on addressing these errors.

It was agreed that a number of other improvements to the existing methodology can be implemented. Within the current methodology, the stratification design will be modified, with construction material to be dropped, significantly reducing the number of strata with zero or few returns each quarter. A standardized procedure for imputation where there are no returns in a stratum will be introduced. This is in addition to the existing procedures, where survey returns are reviewed to identify outliers that could affect results.

To further improve the RPPIs in the medium term, the underlying methodology will switch from stratification to hedonic methods. As a result of discussions during the mission, it was agreed that, given the constraints of the existing survey, hedonic methods represent the best option for reliable RPPIs, particularly, if data sources are improved in the future. The authorities remain enthusiastic about switching from the current stratification method to a hedonic regression method, and, therefore, building staff capacity in this area is a priority. Intensive training on the hedonic method and its relation to the existing methods was provided to the authorities during the mission. Additionally, three staff members will participate in the RPPI training seminar to be held at the Joint Vienna Institute (JVI) during August 2018. Work on developing an experimental hedonic model will be undertaken in 2019.

A switch to comprehensive administrative data will require cooperation of stakeholders elsewhere in the policy system. Existing survey data underpinning the RPPIs are limited, as responses are not legally mandatory. In line with best practice elsewhere, the use of survey data should be replaced by comprehensive administrative data. However, while the authorities can now access information in the registry of property transactions maintained by the State Enterprise Information Center (SEIC), entry of transaction price is not required in the registry, and often the recorded price is the assessed value, rather than the market price. If administrative data are to be used, this will require cooperation of other stakeholders, including the Ministry of Justice (the SEIC’s parent department), so that information recorded in the registry is suitable for use in the compilation of RPPIs.”

The IMF’s latest report on Ukraine:

“A technical assistance (TA) mission was conducted during June 18–22, 2018 to support the State Statistics Service of Ukraine (SSSU) in improving the residential property price indexes (RPPI) for Ukraine. This was the second of a series of SECO2 RPPI-funded TA missions to take place until mid-2019 that will assist in building staff capacity for further development of the RPPI. RPPIs have been identified as critical ingredients for financial stability policy analysis.

Posted by at 2:15 PM

Labels: Global Housing Watch

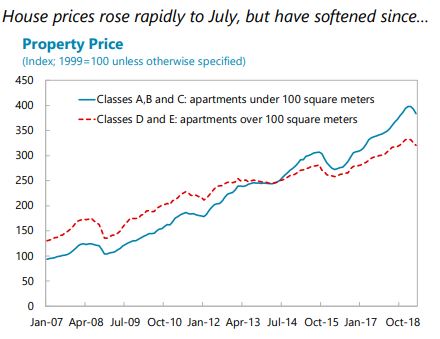

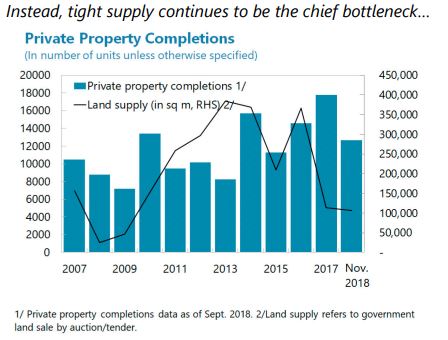

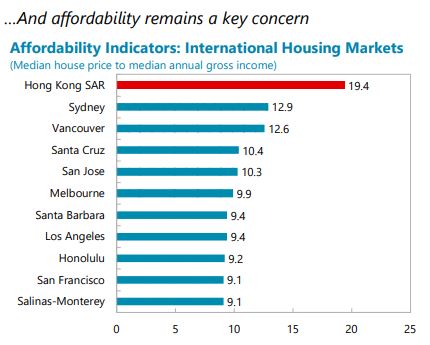

Housing Market in Hong Kong

The IMF’s latest report on Hong Kong says:

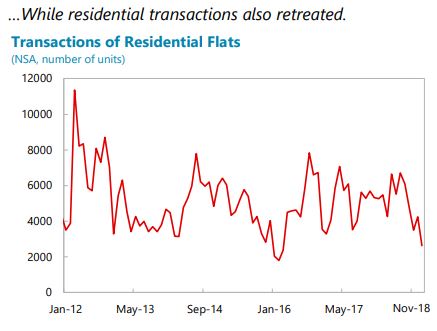

“The three-pronged strategy, comprised of macroprudential measures, stamp duties, and measures to boost housing supply, remains appropriate and should continue in place, and be adjusted as financial stability risks evolve. However, ultimately resolving the imbalances in the housing market requires expanding supply and further efforts are needed in this area.”

“The authorities’ strategy to contain the housing boom using tight macroprudential measures and stamp duties remains appropriate, but more needs to be done to raise housing supply. The authorities’ three-pronged approach relies on a mix of macroprudential policies, stamp duties to contain excessive demand, and measures to increase housing supply. While macroprudential measures have allowed for building buffers in the financial system against a correction, housing prices rose until recently, and affordability deteriorated. A significant increase in housing supply remains the most needed course of action. Given affordability concerns, the authorities could also consider increasing spending on public housing and allocating a larger share of new housing stock for public housing.

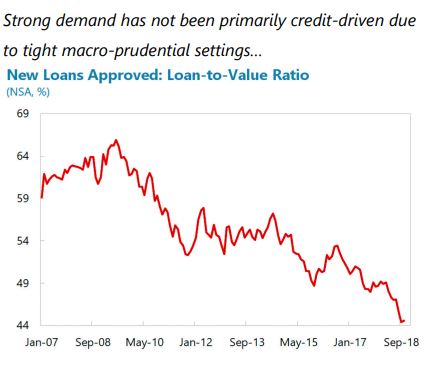

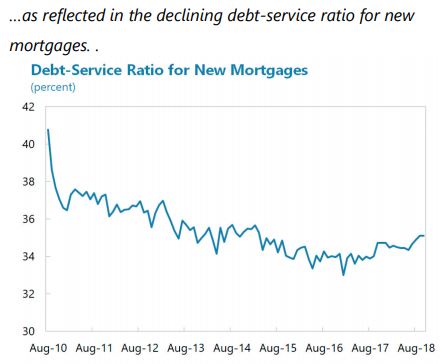

Tight macroprudential regulations have helped contain systemic risks and should remain in place. These include: LTV and debt service-toincome (DSR) ratios that vary with the residence type (primary vs. other) and the source of borrower’s income (originating in vs. outside of Hong Kong SAR); stress tests on the DSR to ensure affordability if interest rates increase; and floors on risk weights on property loans.6 These measures, together with stringent regulation and supervision, allowed banks to build significant buffers that should help cushion the impact of house price declines. While the mix should be reassessed on a regular basis, the authorities should cautiously await more signs of a sustained decline before considering loosening macroprudential and demand-side measures. At the same time, if prices rebound, further tightening of macroprudential measures would likely result in leakages to unregulated non-bank financial institutions as borrowers secure mortgage financing outside regular bank channels (e.g., property developers offering financing to potential buyers).

Stamp duties on real estate have helped contain systemic risks and should be retained for now but phased out when these risks dissipate.

- The government maintains three types of stamp duties on purchase of residential properties: Ad Valorem Stamp Duty on all purchases except of primary residences of permanent residents who do not have any other local residential property at the time of purchase (called previously Doubled Ad Valorem Stamp Duty/currently New Residential Stamp Duty), Special Stamp Duty (SSD) on resale of residential properties within 36 months, and Buyer’s Stamp Duty (BSD) on purchases by non-residents.7 Staff analysis indicates that stamp duties have been effective in curbing house price increases by as much as 9 percent, and, consequently, helped limit household indebtedness and the buildup of systemic risks in the banking sector.

- The DSD/NRSD is levied at a higher rate on non-residents and is assessed to be a capital flow management measure and macroprudential measure under the IMF’s Institutional View of Capital Flows. It continues to be assessed as appropriate given that it: i) was imposed to stem the inflow of capital into the property market; ii) was not used to substitute for the appropriate macroeconomic adjustment; and iii) was imposed because macroprudential measures did not apply to cash buyers, and their further tightening could have resulted in leakages to less regulated non-bank financial institutions. Moreover, the systemic financial risk remains elevated. Stamp duties should be phased out once systemic risks dissipate.

Efforts to further increase supply will be key to resolving the demand-supply imbalance and moderating further price increases.

- After a significant increase in the number of housing units in the early 2000s, the average annual housing production between 2006-2013 fell below 25,000 units. In 2014 the authorities adopted the Long-Term Housing Strategy, which aimed to provide 460,000 housing units over ten years. This was complemented by the Hong Kong 2030+ Strategy—a guide to long-term planning and development of land and infrastructure. While housing production has increased to around 30,000 units on average over 2015-17, it has been falling short of target by around 40 percent on average.

- The authorities are implementing new measures to boost housing supply. In April 2018, the Task Force on Land Supply presented options to increase the availability of land for residential housing, including reclaiming land in Victoria Harbor, and potential development of two strategic areas in East Lantau Metropolis and New Territories North. The “Lantau Tomorrow” reclamation project, as well as further development of brownfield sites, land sharing, and revitalization of existing buildings have been proposed in the 2018 Policy Address. Furthermore, the authorities announced plans to reform the pricing of subsidized housing, initiate a starter homes project, and set up a task force to assist with provision of transitional housing. In addition, a vacant property tax (“Special Rates” tax) of 200 percent of a flat’s “ratable” value (rental value estimated by the Rating and Valuation Revenue Department, roughly 5 percent of the property value) was proposed for unsold new residential units, and a requirement on developers to offer no less than 20 percent of flats during each sale to prevent the accumulation of unsold flats.

- The authorities should also review and—where possible—expedite the procedures guiding the process of identifying land and building sites, zoning, and conducting the necessary environmental, design, transportation, and other assessments to streamline the process.

Frequent reviews of eligibility for social housing could potentially help alleviate social pressures. Around 30 percent of households currently live in public rental housing, with eligibility based on income and wealth, and additional 15 percent of households live in subsidized sale flats. Wait time for public rental housing have increased significantly, from 1.8 years for general applicants and 1.1 years for the elderly in 2008, to 5.1 years and 2.8 years, respectively, in 2017 to ensure proper allocation of benefits, frequent reviews of eligibility should be conducted: in 2016, around 5½ percent of households in the highest income quantile lived in public rental housing.

The authorities agreed that increasing land and housing supply was fundamental to resolving the housing problem facing the community. Challenges in achieving the ten-year housing supply targets under the Long-Term Housing Strategy remain, tied to insufficient land for development and the necessary time to carry out due procedures. The authorities re-iterated that no efforts are being spared, as evidenced by the Government’s vision for the development of Lantau as outlined in the 2018 Policy Address, which should greatly increase land supply in the long-term. Macro-prudential and demand-side measures in the form of stamp duties have been conducive to a healthy development of the property market and will be maintained at this juncture. The authorities added that they could revisit measures as needed if warranted by changes in conditions. They underscored that the current state of the housing market is very different from that pre-Asian Financial Crisis: LTVs are much lower as are debt service burdens, supply is tighter, and banks, developers and households are much less leveraged now.”

The IMF’s latest report on Hong Kong says:

“The three-pronged strategy, comprised of macroprudential measures, stamp duties, and measures to boost housing supply, remains appropriate and should continue in place, and be adjusted as financial stability risks evolve. However, ultimately resolving the imbalances in the housing market requires expanding supply and further efforts are needed in this area.”

“The authorities’ strategy to contain the housing boom using tight macroprudential measures and stamp duties remains appropriate,

Posted by at 2:11 PM

Labels: Global Housing Watch

Housing View – January 25, 2019

On cross-country:

- 15th Annual Demographia International Housing Affordability Survey – Demographia

- Informal settlements and housing markets – International Growth Centre

- Eurozone house price growth squeezed by weaker Italian market – Financial Times

On the US:

- Microsoft’s Leap Into Housing Illuminates Government’s Retreat – New York Times

- Microsoft’s $500 million plan to fix Seattle’s housing problem, explained – VOX

- Dynamism Diminished: The Role of Housing Markets and Credit Conditions – NBER

- Fears of housing downturn may have been overblown – CNN

- US housing: Hopes for a turnaround? – ING

- The Housing Blues Won’t Be Over Soon – Wall Street Journal

- BofA Says Don’t Believe the Hype on a Housing Collapse – Bloomberg

- Housing Inventory Tracking – Calculated Risk

- Shiller: Trump is a ‘psychological boost’ to the housing market – Yahoo Finance

On other countries:

- [Czech Republic] Czech: Property price growth still outstrips EU average – ING

- [Egypt] Egypt’s house prices falling sharply again – Global Property Guide

- [Netherlands] Record House Prices, Jobs Growth Not Enough to Keep Dutch Happy – Bloomberg

- [Singapore] Singapore’s house price rises accelerating – Global Property Guide

- [Spain] Spanish Existing-Home Prices Jump 7.8% in 2018, Most in a Decade – Bloomberg

- [Switzerland] Slowdown inevitable for house prices in Switzerland – Global Property Guide

- [United Arab Emirates] UAE’s property prices fall further – Global Property Guide

- [United Kingdom] Are UK house prices heading for a post-Brexit meltdown? – Financial Times

- [United Kingdom] Whatever happens, Brexit is bad news for young house buyers – Financial Times

- [United Kingdom] Housing market outlook worst ‘for 20 years’ – BBC

- [United Kingdom] Smaller companies deliver better returns than property – Financial Times

- [United Kingdom] Tata Steel announces vision to combat growing housing crisis – Tata Steel

- [United Kingdom] ‘Brexit discount’ on London property fails to tempt US buyers – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- 15th Annual Demographia International Housing Affordability Survey – Demographia

- Informal settlements and housing markets – International Growth Centre

- Eurozone house price growth squeezed by weaker Italian market – Financial Times

On the US:

- Microsoft’s Leap Into Housing Illuminates Government’s Retreat – New York Times

- Microsoft’s $500 million plan to fix Seattle’s housing problem,

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts