Thursday, July 25, 2019

Housing Market in France

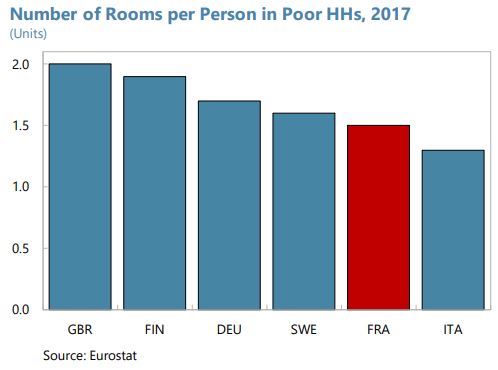

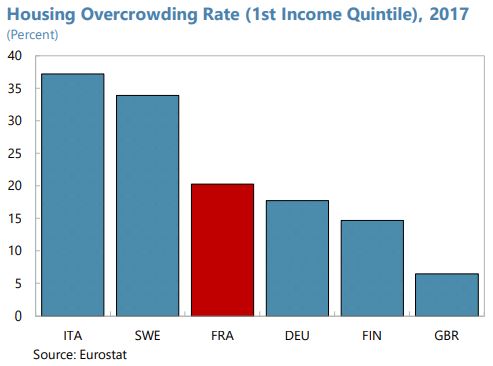

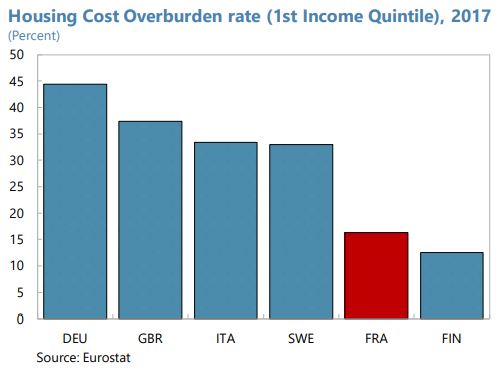

From the IMF’s latest report on France:

“Spending on housing is among the highest among European countries, with mixed outcomes for vulnerable groups (…). Similar to the UK, France spends 1.3 percent of GDP on housing development and housing benefits compared to 0.4 percent and 0.2 percent in Germany and Italy respectively. However, this is associated with mixed outcomes: while the overburden rate of poor households is among the lowest in France (16 percent compared to 37 percent in the UK), the number of rooms per person in poor households is lower in France than in the UK and in Germany, and houses of those at the lowest end of the income distribution in France are three times more overcrowded than in the UK.”

From the IMF’s latest report on France:

“Spending on housing is among the highest among European countries, with mixed outcomes for vulnerable groups (…). Similar to the UK, France spends 1.3 percent of GDP on housing development and housing benefits compared to 0.4 percent and 0.2 percent in Germany and Italy respectively. However, this is associated with mixed outcomes: while the overburden rate of poor households is among the lowest in France (16 percent compared to 37 percent in the UK),

Posted by at 4:31 PM

Labels: Global Housing Watch

Wednesday, July 24, 2019

Okun’s Law–Sectoral and Cross Country Differences

In a new paper, authors Eiji Goto and Constantin Burgi analyze the Okun’s law through sectoral and cross-country differences. The specific value add to existing research, according to the authors, is as follows:

“We contribute to the literature on cyclical differences by determining which category the Okun’s coefficient falls in. Specifically, we test whether the aggregate differences disappear if the sector sizes are the same across countries (e.g. if manufacturing has the same share of GDP for all countries) and we find that this can be rejected. We also examine whether all of the sectoral coefficients are proportional and we find that we cannot reject this. Next, we inspect whether any sector’s coefficient is the same as the aggregate’s and we find that this can also be rejected. Lastly, we decompose the Okun’s coefficient to determine whether the correlation between unemployment or the standard deviations of unemployment or GDP are driving the differences. We find that the standard deviation of unemployment is the main driver”

In a new paper, authors Eiji Goto and Constantin Burgi analyze the Okun’s law through sectoral and cross-country differences. The specific value add to existing research, according to the authors, is as follows:

“We contribute to the literature on cyclical differences by determining which category the Okun’s coefficient falls in. Specifically, we test whether the aggregate differences disappear if the sector sizes are the same across countries (e.g. if manufacturing has the same share of GDP for all countries) and we find that this can be rejected.

Posted by at 3:57 PM

Labels: Inclusive Growth

Tuesday, July 23, 2019

Costs of Recessions

From Stumbling and Mumbling:

“The Resolution Foundation’s James Smith has written a nice paper on the likelihood of recession and the fact that, with monetary less able to support the economy, we need to think about alternative ways of tackling recessions. I just want to amplify what he says in two ways.

First, there’s increasing evidence that recessions can do long-term damage, even if the economy appears to bounce back in the short-term. There are at least three mechanisms here:

– Education. Bryan Stuart shows that the 1980-82 recession in the US “generated sizable long-run reductions in education and income.” Parents who suffer a drop in income spend less on children’s books and educational trips, and this makes them less likely to go to college a few years later. Such effects are magnified if bad macro policy causes restraints upon public spending on schools and libraries.

– Productivity. Recessions increase uncertainty, which depresses investment in both capital and R&D, leading to lower productivity growth. The Bank of England’s Dario Bonciani and Joonseok Jason Oh say:

Shocks increasing macroeconomic uncertainty can lead to very persistent negative effects on economic activity that last well beyond the business cycle frequency.

– Scarring. A recent paper by Erin McGuire shows that people who grow up in hard times “invest less in risky assets throughout their lives, invest more in property, and are less likely to be self-employed.” This corroborates research (pdf) by Ulrike Malmendier and Stefan Nagel. Through this channel, recessions can reduce entrepreneurship and increase the cost of capital even decades later.

Against all this, it is theoretically possible that recessions have a beneficial “cleansing” (pdf) effect: in driving inefficient firms out of business, they make it easier for more efficient ones to expand, and this raises productivity growth.”

Continue reading here.

From Stumbling and Mumbling:

“The Resolution Foundation’s James Smith has written a nice paper on the likelihood of recession and the fact that, with monetary less able to support the economy, we need to think about alternative ways of tackling recessions. I just want to amplify what he says in two ways.

First, there’s increasing evidence that recessions can do long-term damage, even if the economy appears to bounce back in the short-term.

Posted by at 11:16 AM

Labels: Inclusive Growth

Monday, July 22, 2019

Mapped: The Countries With the Highest Housing Bubble Risks

From Visual Capitalist:

“With a decade-long bull market and an ultra low interest rate environment globally, it’s not surprising to see capital flock to housing assets.

For many investors, real estate is considered as good of a place as any to park money—but what happens when things get a little too frothy, and the fundamentals begin to slip away?

In recent years, experts have been closely watching several indicators that point to rising bubble risks in some housing markets. Further, they are also warning that countries like Canada and New Zealand may be overdue for a correction in housing prices.

Key Housing Market Indicators

Earlier this week, Bloomberg published results from a new study by economist Niraj Shah as he aimed to build a housing bubble dashboard.

It tracks four key metrics:

- House Price-Rent Ratio

The ratio of house prices to the annualized cost of rent- House Price-Income Ratio

The ratio of house prices to household income- Real House Prices

Housing prices adjusted for inflation- Credit to Households (% of GDP)

Amount of debt held by households, compared to total economic outputRanking high on just one of these metrics is a warning sign for a country’s housing market, while ranking high on multiple measures signals even greater fragility.”

Continue reading here.

From Visual Capitalist:

“With a decade-long bull market and an ultra low interest rate environment globally, it’s not surprising to see capital flock to housing assets.

For many investors, real estate is considered as good of a place as any to park money—but what happens when things get a little too frothy, and the fundamentals begin to slip away?

In recent years, experts have been closely watching several indicators that point to rising bubble risks in some housing markets.

Posted by at 9:54 AM

Labels: Global Housing Watch

Decoupling-Debunked

From the European Environmental Bureau:

“Is it possible to enjoy both economic growth and environmental sustainability? This question is a matter of fierce political debate between green growth and post-growth advocates. Over the past decade, green growth clearly dominated policy making with policy agendas at the United Nations, European Union, and in numerous countries building on the assumption that decoupling environmental pressures from gross domestic product (GDP) could allow future economic growth without end.

Considering what is at stake, a careful assessment to determine whether the scientific foundations behind this “decoupling hypothesis” are robust or not is needed. This report reviews the empirical and theoretical literature to assess the validity of this hypothesis. The conclusion is both overwhelmingly clear and sobering: not only is there no empirical evidence supporting the existence of a decoupling of economic growth from environmental pressures on anywhere near the scale needed to deal with environmental breakdown, but also, and perhaps more importantly, such decoupling appears unlikely to happen in the future.

It is urgent to chart the consequences of these findings in terms of policy-making and prudently move away from the continuous pursuit of economic growth in high-consumption countries. More precisely, existing policy strategies aiming to increase efficiency have to be complemented by the pursuit of sufficiency, that is the direct downscaling of economic production in many sectors and parallel reduction of consumption that together will enable the good life within the planet’s ecological limits. In the view of the authors of this report and based on the best available scientific evidence, only such strategies respect the EU’s ‘precautionary principle,’ the principle that when the stakes are high and the outcomes uncertain, one should err on the side of caution.

The fact that decoupling on its own, i.e. without addressing the issue of economic growth, has not been and will not be sufficient to reduce environmental pressures to the required extent is not a reason to oppose decoupling (in the literal sense of separating the environmental pressures curve from the GDP curve) or the measures that achieve decoupling – on the contrary, without many such measures the situation would be far worse. It is a reason to have major concerns about the predominant focus of policymakers on green growth, this focus being based on the flawed assumption that sufficient decoupling can be achieved through increased efficiency without limiting economic production and consumption.”

From the European Environmental Bureau:

“Is it possible to enjoy both economic growth and environmental sustainability? This question is a matter of fierce political debate between green growth and post-growth advocates. Over the past decade, green growth clearly dominated policy making with policy agendas at the United Nations, European Union, and in numerous countries building on the assumption that decoupling environmental pressures from gross domestic product (GDP) could allow future economic growth without end.

Posted by at 9:51 AM

Labels: Energy & Climate Change

Subscribe to: Posts