Friday, August 16, 2019

Good for the environment, good for business: Foreign acquisitions and energy intensity

From a VoxEU post by Arlan Brucal, Beata Javorcik, and Inessa Love:

“The link between foreign ownership and environmental performance remains a controversial issue. Data from the Indonesian manufacturing census show that plants undergoing foreign acquisitions reduce their energy intensity by about 30% two years after acquisition by multinationals. This column argues that foreign direct investment can serve as a channel for the international transfer of environmentally friendly technologies and practices, thus directly contributing not only to economic growth but also to environmental progress.

According to the 2018 report of the UN Intergovernmental Panel on Climate Change (IPCC), exceeding the global threshold of 1.5°C above the pre-industrial temperature level will mean increased risk of extreme drought, wildfires, floods, and food shortages for hundreds of millions of people. Keeping emissions below the crucial threshold would require widespread changes in energy, industry, buildings, transportation, and cities. Can multinationals be part of the solution? Can flows of foreign direct investment (FDI) help put a brake on emissions? Or would they exacerbate the already worsening global climate condition?

Environmentalists argue that highly polluting multinationals relocate to countries with weaker environmental standards to circumvent costly regulations in their home country (Hanna 2010, Millimet and Roy 2015, Cai et al. 2016). In this way, they increase pollution levels not only in host countries but also globally.

In contrast, supporters of globalisation point out that FDI has a positive effect on the natural environment because multinationals tend to use more efficient and cleaner technologies than their domestic counterparts. With the spectacular growth in FDI flows and the increasing importance of developing nations as host countries, the potential effect of FDI on the natural environment remains controversial (Kellenberg 2009, Cole et al. 2017).

In a forthcoming paper (Brucal et al. 2019), we contribute to this discussion by examining the impact of foreign acquisitions on energy consumption and CO2 emissions of acquired plants. The study is based on plant-level data from the Indonesian Manufacturing Census, covering the period 1983-2001. The data contains detailed information on plant-level use of various energy inputs (both in value and physical units) and thus can be used to calculate the expected CO2 emissions using standard conversion factors specific to each type of energy. We then compare the changes in these variables in the acquired plants and a carefully selected group of domestic plants that had not changed ownership.1

Why would we expect acquired plants to improve energy efficiency?

There are several reasons why foreign acquisitions may improve energy efficiency. First, foreign acquisitions tend to increase production volume by boosting productivity and facilitating access to foreign markets through the foreign parent’s distribution network (Arnold and Javorcik 2009). This makes investments in improving energy efficiency more worthwhile as the sales base becomes large enough to cover the fixed cost of investment.”

Continue reading here.

From a VoxEU post by Arlan Brucal, Beata Javorcik, and Inessa Love:

“The link between foreign ownership and environmental performance remains a controversial issue. Data from the Indonesian manufacturing census show that plants undergoing foreign acquisitions reduce their energy intensity by about 30% two years after acquisition by multinationals. This column argues that foreign direct investment can serve as a channel for the international transfer of environmentally friendly technologies and practices,

Posted by at 9:50 AM

Labels: Energy & Climate Change

Monday, August 12, 2019

House Prices in China

From IMF’s latest report on China:

“The property market trended down. Growth in real estate investment (excluding land purchases) was mostly negative in 2018, and both house price growth and sales growth slowed since late 2018. Housing inventories have started to build up in recent months, suggesting the housing cycle may still be in a downturn.”

From IMF’s latest report on China:

“The property market trended down. Growth in real estate investment (excluding land purchases) was mostly negative in 2018, and both house price growth and sales growth slowed since late 2018. Housing inventories have started to build up in recent months, suggesting the housing cycle may still be in a downturn.”

Posted by at 10:58 AM

Labels: Global Housing Watch

Wednesday, August 7, 2019

Labor Market Slack and the Output Gap: The Case of Korea

A new IMF working paper, by authors Niels-Jakob Hansen, Joannes Mongardini and Fan Zhang, discusses the labor market slack and outgap through the Korean experience :

“Output gap estimates are widely used to inform macroeconomic policy decisions, including in Korea. The main determinant of these estimates is the measure of labor market slack. The traditional measure of unemployment in Korea yields an incomplete estimate of labor market slack, given that many workers prefer involuntary part-time jobs or leaving the labor force rather than registering as unemployed. This paper discusses a way in which the measure of unemployment can be broadened to yield a more accurate measure of labor market slack. This broader measure is then used to estimate the output gap using a multivariate filter, yielding a more meaningful measure of the output gap.”

A new IMF working paper, by authors Niels-Jakob Hansen, Joannes Mongardini and Fan Zhang, discusses the labor market slack and outgap through the Korean experience :

“Output gap estimates are widely used to inform macroeconomic policy decisions, including in Korea. The main determinant of these estimates is the measure of labor market slack. The traditional measure of unemployment in Korea yields an incomplete estimate of labor market slack, given that many workers prefer involuntary part-time jobs or leaving the labor force rather than registering as unemployed.

Posted by at 12:46 PM

Labels: Inclusive Growth

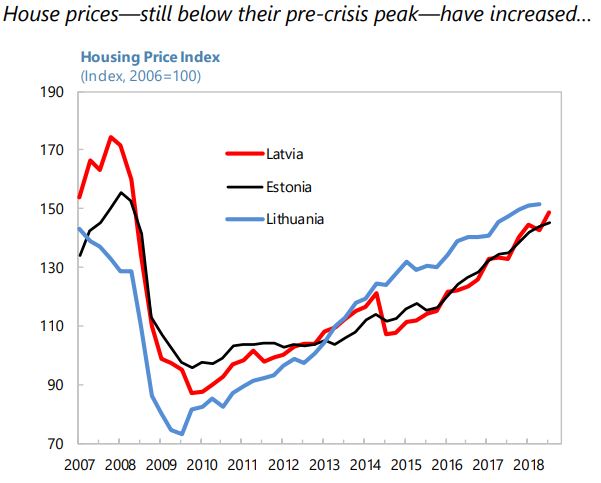

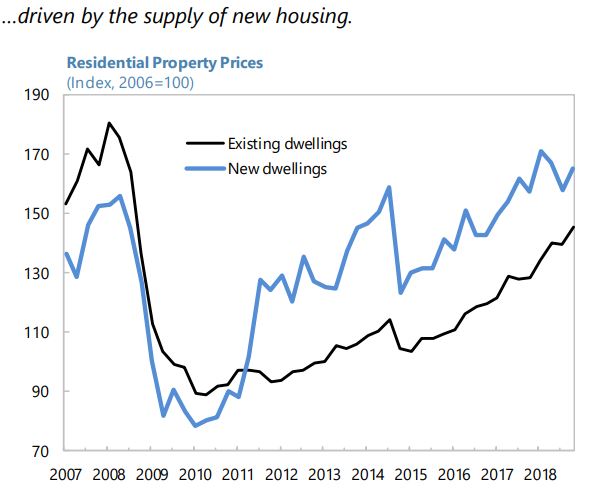

House Prices in Latvia

From the IMF’s latest report on Latvia:

“The rapid rise in property prices merits attention. Despite a shrinking population, real house prices have increased by more than 7 percent per year over the last three years due to a surge in construction costs and prices of new dwellings. Current valuation indicators (price-to-income and price-to-rent ratios and deviations from long-term fundamentals) signal potential vulnerability to overvaluation of housing prices over the medium term. Yet, there are no acute financial imbalances, as the house price index is still about 20 percent below its pre-crisis peak in 2008, and aggregate house price developments have not been spurred by credit growth. Outstanding mortgage loans have dropped below 20 percent of GDP at end-2018, far below the euro area average of about 38 percent of GDP.

Timely adoption of precautionary macroprudential measures can help contain medium-term balance sheet risks. The high share of variable rate mortgages raises the risk to debt service capacity if household leverage increases, while a slowing wage growth could reduce debt affordability. BSFCs’ re-orientation may also result in a deterioration of borrower quality if they loosen credit standards and increase household lending to maintain profitability amid falling margins. Latvia’s macroprudential measures are relatively lenient compared to those in other EU countries and could be preemptively adjusted. Lowering the current LTV ratio limit of 90 percent to 80 percent (closer to other European peers) for residential mortgage lending, imposing restrictions on home refinancing, introducing a debt service-to-income (DSTI) limit, and limiting the maximum maturity of mortgages and consumer loans would mitigate vulnerabilities related to real-estate exposures. Higher provisions for loans with LTV ratios above the limit and regular assessments of collateral valuation standards would prevent excessively risky lending. Finally, macroprudential measures should apply to leasing companies to prevent potential regulatory arbitrage between them and banks.”

From the IMF’s latest report on Latvia:

“The rapid rise in property prices merits attention. Despite a shrinking population, real house prices have increased by more than 7 percent per year over the last three years due to a surge in construction costs and prices of new dwellings. Current valuation indicators (price-to-income and price-to-rent ratios and deviations from long-term fundamentals) signal potential vulnerability to overvaluation of housing prices over the medium term.

Posted by at 9:50 AM

Labels: Global Housing Watch

Monday, August 5, 2019

Monetary Policy, Housing Rents and Inflation Dynamics

From a paper by Daniel A. Dias and João B. Duarte:

“In this paper we study the effect of monetary policy shocks on housing rents. Our main finding is that, in contrast to house prices, housing rents increase in response to contractionary monetary policy shocks. We also find that, after a contractionary monetary policy shock, rental vacancies and the homeownership rate decline. This combination of results suggests that monetary policy may affect housing tenure decisions (own versus rent). In addition, we show that, with the exception of the shelter component, all other main components of the consumer price index (CPI) either decline in response to a contractionary monetary policy shock or are not responsive. These findings motivated us to study the statistical properties of alternative measures of inflation that exclude the shelter component. We find that measures of inflation that exclude shelter have most of the statistical properties of the widely used measures of inflation, such as the CPI and the price index for personal consumption expenditures (PCE), but have higher standard deviations and react more to monetary policy shocks. Finally, we show that the response of housing rents accounts for a large proportion of the “price puzzle” found in the literature.”

From a paper by Daniel A. Dias and João B. Duarte:

“In this paper we study the effect of monetary policy shocks on housing rents. Our main finding is that, in contrast to house prices, housing rents increase in response to contractionary monetary policy shocks. We also find that, after a contractionary monetary policy shock, rental vacancies and the homeownership rate decline. This combination of results suggests that monetary policy may affect housing tenure decisions (own versus rent).

Posted by at 4:39 PM

Labels: Global Housing Watch

Subscribe to: Posts