Wednesday, September 18, 2019

House prices in Mongolia

From the IMF’s latest report on Mongolia:

Posted by at 11:08 AM

Labels: Global Housing Watch

Tuesday, September 17, 2019

Evaluating housing affordability policies: What works?

Global Housing Watch Newsletter: September 2019

In this interview, Stijn Van Nieuwerburgh talks about his new paper on “Affordable Housing and City Welfare”. Stijn Van Nieuwerburgh is the Earle W. Kazis and Benjamin Schore Professor of Real Estate and Professor of Finance at Columbia University’s Graduate School of Business. The paper is co-authored with Jack Y Favilukis (University of British Columbia) and Pierre Mabille (New York University).

Hites Ahir: The “housing affordability crisis” has been in the headlines in many parts of the world. How serious is this crisis?

Stijn Van Nieuwerburgh: One commonly agreed upon metric to quantify the lack of affordability is the fraction of renters that spend more than 30 percent of their income on rent. Among the 50 largest metropolitan areas in the United States, half of all renter households are rent burdened. Another popular metric is house price to average income ratio. The price-to-income ratios have been going up in every major city in the world. In my view, this is the leading challenge for local policy makers.

Hites Ahir: Your new paper builds a framework to evaluate four housing policy tools—zoning changes, rent control, housing vouchers, and tax credits—that policymakers employ to tackle housing affordability issues. In layman’s terms, could you describe the framework?

Stijn Van Nieuwerburgh: The framework is adapted from modern macro-economics and finance: a large group of households that differ in age and labor productivity make choices about how much to consume, save, and work, whether to own or rent a house, the size of the house, and how large a mortgage to get–if they own. Savings are invested in a bond or in rental housing. We introduce a spatial dimension in this macro model: the city has a center where people work, but only some live there. The rest commutes from the suburbs and outer boroughs of the city to the center. Commuting has a time cost and a financial cost. Households can choose their location in each period. Developers decide how much housing to build in each location but are subject to zoning rules, which are particularly strict in the center. This makes housing supply much less elastic in the center.

Developers are subject to an affordable housing mandate capturing the realities of mandatory inclusionary housing: when they build rental housing, developers must set aside a percent of the total square feet for housing that rents at below-market rates. These affordable housing units are allocated by lottery, but subject to an income qualification requirement. Once a household gains access to an affordable housing unit, it is allowed to stay there without having to satisfy the income requirement.

The model captures three main costs of affordable housing. First, supply reductions because developers face lower prices and rents. Second, misallocation of housing across the income and wealth distribution both because some underserving households gain access to affordable units despite having fairly high income or wealth and because they do not move out once their income rises. Misallocation also takes the form of distortions in the size of the housing unit chosen with some consuming more housing and others less than they would in the free market, and spatial misallocations. Third, a reduction in labor supply.

The model also captures a key benefit of affordable housing units: it acts as insurance device in the presence of income risk. When households fall on hard times, these affordable housing units provide shelter at low rents which improves housing stability. Because most models that deal with affordable housing do not model households’ income risk, households’ risk aversion, and market incompleteness, they miss this insurance benefit.

In sum, affordable housing policies have costs and benefits. Dialing the knobs of these policies up or down shifts the economy along the efficiency-equality tradeoff curve. Since a policy usually benefits some households at the expense of others, we need to take a stance on how to aggregate individual households’ welfare. We choose a utilitarian social welfare criterion which weighs every household equally. But because poor households have higher marginal utility, there is more social benefit to helping them. How much more depends on the curvature of the utility function and how much residual risk they face given the social insurance programs already in place.

Hites Ahir: What are the main findings?

Stijn Van Nieuwerburgh: We calibrate the model to the New York metropolitan area, and show that the model does a good job matching the observed income, housing, and financial wealth inequality, house price and rent levels, and home ownership rates. The model also captures current zoning policy and the share of affordable housing units currently in place. With this “status quo” as our baseline, we explore various policy changes.

The first main result is that reducing the misallocation of affordable housing units can lead to large welfare gains, about 3.6 percent of lifetime wealth. Specifically, we lower the income qualification threshold for affordable housing unit lottery winners, and force existing tenants to requalify every 4 years. By rotating out higher-income tenants and bringing in low-income tenants, we improve access to the insurance provided by affordable housing units. We can do so without dramatically reducing housing stability. Of all policies we analyze, reducing the misallocation of affordable housing units creates the largest welfare gains for society. This policy does not expand the number of affordable housing units.

The second main policy experiment studies an expansion of the affordable housing mandate. Developers now must set aside a larger percentage of square feet of affordable rental units of the total square feet of market rentals they build. This policy is akin to an expansion of rent control–as recently transpired in New York State and Oregon–since a larger fraction of rental units will be affordable. We contemplate a fifty percent expansion, which results in 30 percent rather than 20 percent of the rental stock being rented at a 50 percent discount to the market rent This policy creates modest welfare gains of 0.66% of permanent consumption. This gain is only about 1/6th as large as reducing the misallocation in the existing affordable housing stock but comes at great expense to the developers in the form of billions of dollars in lost rents. The reason for the modest gain is that while the policy helps more needy households, it also creates more housing and labor supply distortions, and more housing misallocation.

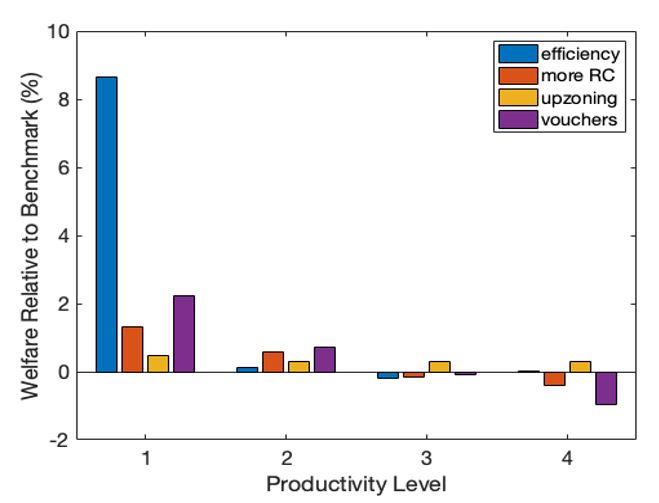

The third main experiment studies an upzoning policy, which increases the amount of residential housing that can be built in the city center by 10%. This policy has the intended effect of lowering rents and house prices by increasing housing supply. It also saves on commuting costs since more households can now live in the city center. But the welfare gain it creates is modest: 0.37%, or about half of the gain from the expansion of rent control. In contrast to the previous policies, zoning is much less redistributive in nature. It benefits all ages, income groups, and wealth groups, even most existing homeowners (who do suffer house price declines). By the same token, it fails to generate large welfare gains for the poor, which is where most of the bang for the buck lies in terms of welfare gains.

The fourth experiment expands housing vouchers, such as Section 8 vouchers. These are cash transfers earmarked for housing. In the model, the additional vouchers must be paid for with additional taxes. Since the tax system is progressive, the rich see their taxes rise. Because labor income taxation is distortionary, this results in a non-trivial reduction in labor supply. The city’s economic output falls as a result. Nevertheless, the voucher expansion is well targeted on the poor and creates a sizeable welfare gain of 1.0 percent.

Figure 1 shows the welfare gains of the policies for households of different productivity levels. It clearly shows the redistributive nature of the policies that make affordable housing more efficient, that expand rent control, and that increase vouchers. The upzoning policy creates smaller, but more uniformly distributed benefits.

In the paper we also consider low-income housing tax credits, which we find to be fairly ineffective since they create modest rent reductions but are financed with distortionary taxation.

One final experiment worth mentioning is that moving all affordable housing units from the city center to the rest of the MSA leads to a welfare gain, but only if it is accompanied by subsidies for transportation. The financial cost of commuting is an important factor for low-income households.

Figure 1.

Hites Ahir: In the paper, you point out that standard affordability metrics do not capture the improved availability of affordable housing. Why?

Stijn Van Nieuwerburgh: In a spatial equilibrium model, households may respond to policy changes by moving. This changes the average income of a neighborhood. While rents may be falling in response to a policy change, average rent-to-income ratios may be rising if the policy attracts lower income households to the neighborhood. The policy experiment that creates more affordable housing units, for example, results in a rise in the average rent-to-income ratio in both zones. A policy maker defining housing affordability by the average rent-to-income ratio would erroneously conclude affordability had gone down.

Hites Ahir: What are the policy implications of your findings?

Stijn Van Nieuwerburgh: They follow directly from the welfare gain calculations. We need more efficiency in the affordable housing system with a renewed focus on helping the neediest. Allowing people who make more than $200,000 stay in their affordable housing unit, like in the new New York rent control law, is the wrong reform. We do not require a massive expansion in the scope of the affordable housing stock, but modest expansions can help in combination with reductions in misallocation. We also need to expand supply, but cannot expect miracles from that approach alone.

Hites Ahir: What kind of questions you would like future research on housing affordability to address?

Stijn Van Nieuwerburgh: We hope the framework is useful as a jumping-off board for others to model more place-based policies, such as investments in transportation infrastructure.

Global Housing Watch Newsletter: September 2019

In this interview, Stijn Van Nieuwerburgh talks about his new paper on “Affordable Housing and City Welfare”. Stijn Van Nieuwerburgh is the Earle W. Kazis and Benjamin Schore Professor of Real Estate and Professor of Finance at Columbia University’s Graduate School of Business. The paper is co-authored with Jack Y Favilukis (University of British Columbia) and Pierre Mabille (New York University).

Posted by at 9:21 AM

Labels: Global Housing Watch

Friday, September 13, 2019

Manufacturing Jobs and Inequality: Why is the U.S. Experience Different?

From a new IMF working paper by Natalija Novta and Evgenia Pugacheva:

“We examine the extent to which declining manufacturing employment may have contributed to increasing inequality in advanced economies. This contribution is typically small, except in the United States. We explore two possible explanations: the high initial manufacturing wage premium and the high level of income inequality. The manufacturing wage premium declined between the 1980s and the 2000s in the United States, but it does not explain the contemporaneous rise in inequality. Instead, high income inequality played a large role. This is because manufacturing job loss typically implies a move to the service sector, for which the worker is not skilled at first and accepts a low-skill wage. On average, the associated wage cut increases with the overall level of income inequality in the country, conditional on moving down in the wage distribution. Based on a stylized scenario, we calculate that the movement of workers to low-skill service sector jobs can account for about a quarter of the increase in inequality between the 1980s and the 2000s in the United States. Had the U.S. income distribution been more equal, only about one tenth of the actual increase in inequality could have been attributed to the loss of manufacturing jobs, according to our simulations.”

From a new IMF working paper by Natalija Novta and Evgenia Pugacheva:

“We examine the extent to which declining manufacturing employment may have contributed to increasing inequality in advanced economies. This contribution is typically small, except in the United States. We explore two possible explanations: the high initial manufacturing wage premium and the high level of income inequality. The manufacturing wage premium declined between the 1980s and the 2000s in the United States,

Posted by at 5:09 PM

Labels: Inclusive Growth

House Prices in Namibia

From the IMF’s latest report on Namibia:

Private sector credit and house prices growth decelerated, while private sector indebtedness remained elevated. After years of double digit increases, nominal credit growth to the private sector sharply declined in 2017 and stabilized at around 6.8 percent in 2018.6 With liquidity easing, the deceleration was mostly driven by weak demand from a highly-leveraged private sector and the implementation of some macroprudential measures (…). Weak credit and economic conditions contributed reducing the growth rate in residential house prices to 1.7 percent (9¾ percent average over the past five years). The economic slowdown began affecting the banking sector’s asset quality. Over the last two years, NPLs more than doubled, although from very low levels. More recently, banks have started tightening lending conditions. With government’s financing needs still high, banks’ direct exposures to the public sector continued rising and reached about 10 percent of banks’ total assets (7 percent in 2016).”

From the IMF’s latest report on Namibia:

Private sector credit and house prices growth decelerated, while private sector indebtedness remained elevated. After years of double digit increases, nominal credit growth to the private sector sharply declined in 2017 and stabilized at around 6.8 percent in 2018.6 With liquidity easing, the deceleration was mostly driven by weak demand from a highly-leveraged private sector and the implementation of some macroprudential measures (…). Weak credit and economic conditions contributed reducing the growth rate in residential house prices to 1.7 percent (9¾ percent average over the past five years).

Posted by at 10:31 AM

Labels: Global Housing Watch

Housing View – September 13, 2019

On the US:

- First Reactions: The Treasury Plan for GSE Reform by Administrative Means – Joint Center for Housing Studies

- The Trump administration’s new plan to privatize Fannie Mae and Freddie Mac, explained – VOX

- Trump’s housing finance plan will make mortgages more expensive, especially for black borrowers, housing groups say – Washington Post

- Subduing the Housing Godzillas – Wall Street Journal

- The fall housing market expected to be more of the same – Washington Post

- Housing Sentiment Inches Higher, Driven by Mortgage Rate Outlook – Fannie Mae

- Campaign 2020: How to fix America’s housing policies – Brookings

- Housing finance reform battle lines drawn in Senate hearing – Market Watch

- The Share Economy Can Help Lower Housing Prices If We Let It – Forbes

- California Rent Control Bill Advances, Fueled by Housing Crisis – New York Times

- How State and Local Governments are Responding to the Affordability Crisis – Harvard Joint Center for Housing Studies

- A Real Housing Economist Speaks – Forbes

- California lawmakers move to reinstate, revamp local affordable housing program – Los Angeles Times

- California Approves Statewide Rent Control to Ease Housing Crisis – New York Times

On other countries:

- [Australia] Australia mortgage lending surges on relaxation of rules – Financial Times

- [Russia] Russia’s housing market improving – Global Property Guide

- [Singapore] Singapore Unveils Changes to Make Public Housing More Affordable – Bloomberg

- [South Korea] South Korea’s housing market remains sluggish – Global Property Guide

- [Thailand] Thailand’s modest house price rises – Global Property Guide

- [United Kingdom] Tackling the UK housing crisis: is supply the answer? – UK Collaborative Centre for Housing Evidence

- [Ukraine] Ukraine’s housing market remains depressed – Global Property Guide

On the US:

- First Reactions: The Treasury Plan for GSE Reform by Administrative Means – Joint Center for Housing Studies

- The Trump administration’s new plan to privatize Fannie Mae and Freddie Mac, explained – VOX

- Trump’s housing finance plan will make mortgages more expensive, especially for black borrowers, housing groups say – Washington Post

- Subduing the Housing Godzillas – Wall Street Journal

- The fall housing market expected to be more of the same – Washington Post

- Housing Sentiment Inches Higher,

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts