Sunday, July 14, 2019

Explaining High Unemployment in ECCU Countries

A new IMF paper explains unemployment in ECCU countries:

“Unemployment rates in Grenada (GRD), St. Lucia (LCA), and St. Vincent and Grenadines (VCT) have been above 20 percent in recent years. Unemployment in Dominica (DMA) has also been high by international standards even before the natural disasters that recently hit the country. While it is likely that weak employment this decade was partly related to the impact of the global economic downturn, unemployment was already high prior to the global crisis in most of these countries, thus suggesting there are structural factors behind it. This paper evaluates factors that could explain high unemployment in ECCU countries, cyclical and structural.1 Our analysis systemically reviews demand, supply, and institutional factors that could foster unemployment. Within this framework, we analyze the potential impact of the global financial crisis, the downfall of the banana/sugar industries, the hurricanes that frequently hit these countries, the relatively rigid wage setting process, as well as factors that could increase reservation wages.”

A new IMF paper explains unemployment in ECCU countries:

“Unemployment rates in Grenada (GRD), St. Lucia (LCA), and St. Vincent and Grenadines (VCT) have been above 20 percent in recent years. Unemployment in Dominica (DMA) has also been high by international standards even before the natural disasters that recently hit the country. While it is likely that weak employment this decade was partly related to the impact of the global economic downturn,

Posted by at 4:36 PM

Labels: Inclusive Growth

Friday, July 12, 2019

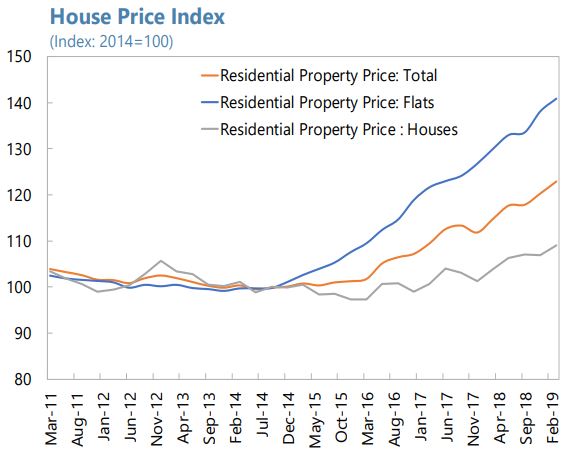

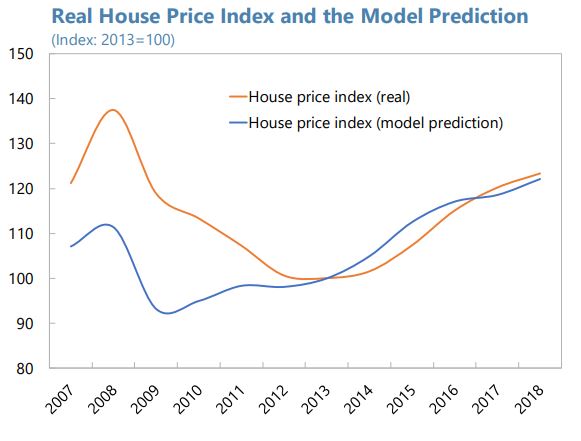

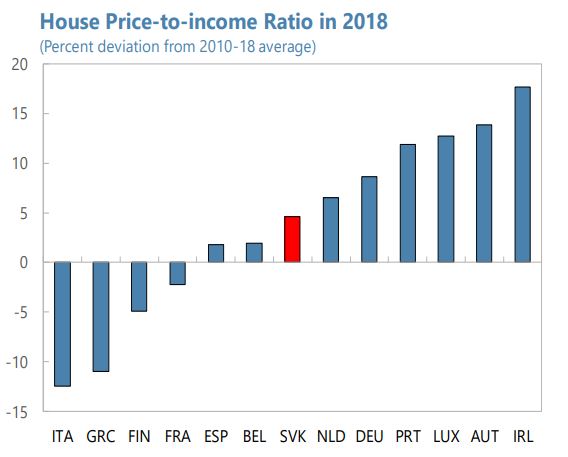

Housing Market in Slovak Republic

From the IMF’s latest report on Slovak Republic:

“There are early signs of a buildup of imbalances in the housing market. Overall house prices have increased in line with peers in the region. A regression-based assessment also shows that overall price increases since 2013 can largely be explained by economic fundamentals (…). Nonetheless, rising house price-to-income ratio shows a mild deviation from the historical average. Flat prices in urban areas have increased much more than the average house price, reflecting strong demand from domestic investors and migrant rural workers as well as supply constraints resulting from limited plot availability and lengthy processes to obtain construction permits. The underdevelopment of the rental housing market—counting only around 10 percent of the housing market— contributes to higher property prices.”

The authorities’ pro-active macroprudential policy stance is welcome and could be strengthened as follows.

- Reduce NPLs of less systemic institutions. The authorities’ initiative to require banks with high NPL ratios to develop an NPL reduction strategy is welcome and their efforts to reduce NPLs should be sustained. To contain credit risks, building societies should be required to increase the NPL coverage ratio. The recently introduced regulatory cap on the share of long-maturity loans in new loans extended by building societies (20 percent for loans with 20–30 years of maturity and 10 percent for loans with 25–30 years of maturity) should be complemented by a cap on the share of uncollateralized loans in total loans.

- Enhance capital buffers of weaker banks. Staff supported incremental use of the counter-cyclical capital buffers (CCyB) and supervisory (Pillar II) capital requirements to enhance resilience of banks to shocks and the authorities’ readiness to further increase the CCyB. In addition, considering the uneven asset quality across banks, the authorities should strongly consider imposing non-zero Pillar II capital guidance for less systemic institutions in 2019 taking into account supervisory stress test results.

- Allow the bank levy to expire. The bank levy, imposed on liabilities (less equity) of banks, weighs heavily on unprofitable banks—in some cases, claiming more than 30 percent of pre-tax income. As the initial targeted amount (EUR 750 million) has already been collected, the levy should be allowed to expire in 2021 as legislated to help these banks safeguard profitability and accumulate buffers.

- Better internalize mortgage credit risks. The average risk weights in the internal models of systemic foreign bank subsidiaries in Slovakia are lower than in most other EU peers reflecting historically low default rates. To discourage excessive risk taking, the authorities should strongly consider introducing a risk weight add-on on housing loans to require banks to better internalize credit risks, which can be complemented with a floor on risk weights on housing loans. The authorities should also be vigilant about possible risks that mortgage brokers may facilitate loosening lending standards of banks.

Considerations should be given to remove preferential tax treatment of housing related capital gains and link real-estate taxation to the market value of the property. These measures are expected to curb demand for real estate, particularly demand related to investment reasons, and add to fiscal revenues. Staff welcomed efforts to streamline regulatory procedures for construction permits, which could improve housing supply and ease price pressures. Legal frameworks governing the rental house market in Slovakia discourage the development of longterm rental market given strong protection of tenants’ rights for contracts beyond two years. Introducing a more balanced regulation of landlord-tenant rights could reduce demand for home ownership from over-leveraged or low-income households.

Continued efforts are needed to implement a robust AML/CFT framework. The authorities made efforts to transpose EU 4th AML Directive in 2018 and are now preparing the AML/CFT Action Plan 2019–22, based on the National Risk Assessment carried out in 2017–18. Sustained efforts are needed, including to improve disciplinary processes, step-up bank employee trainings, strengthen measures to support anti-corruption efforts, and enhance operational independence and effectiveness of the Financial Intelligence Unit.

Strong home-host cooperation should continue. Given the dominance of foreign banks in Slovak banking system, strong home-host cooperation including close engagements in Joint Supervisory Teams in SSM is critical. With limited domestic capacity to absorb bail-inable bonds, encouraging banks to have higher non-regulatory capital buffers may also help them meet minimum requirement for own funds and eligible liabilities (MREL). To fill the gaps identified at European level regulations by the recent euro area FSAP, the domestic regulatory regime should require banks to obtain authorities’ pre-approval in acquiring qualifying holdings of non-bank entities and to periodically report the ultimate beneficial owners of their qualifying holdings.”

From the IMF’s latest report on Slovak Republic:

“There are early signs of a buildup of imbalances in the housing market. Overall house prices have increased in line with peers in the region. A regression-based assessment also shows that overall price increases since 2013 can largely be explained by economic fundamentals (…). Nonetheless, rising house price-to-income ratio shows a mild deviation from the historical average. Flat prices in urban areas have increased much more than the average house price,

Posted by at 10:12 AM

Labels: Global Housing Watch

Is There a Relationship between Inflation and Unemployment?

From Econbrowser:

“Or, old fogey downloads data, finds a negative relationship, a.k.a. the Phillips Curve…

Much was made of the meeting of minds of AOC and Larry Kudlow regarding the Phillips Curve, to wit (from Bloomberg):

… Ocasio-Cortez said many economists are concerned that the formula “is no longer describing what is happening in today’s economy” — and Powell largely agreed.

“She got it right,” Kudlow told reporters at the White House later on Thursday. “He confirmed that the Phillips Curve is dead. The Fed is going to lower interest rates.”

Well, since I’ve been teaching the Phillips Curve for lo these thirty odd years, I thought I’d check to see if I’d missed something. First, it’s important to remember that while we talk about the negative relationship between inflation and unemployment, or the positive relationship between inflation and output, the actual model we use is the expectations augmented Phillips curve including input price shocks. My preferred specification is:

πt = πet + f(ut-4 – un,t-4) + θzt

Where π is 4 quarter inflation, πe is expected inflation, u is official unemployment rate, un is natural rate of unemployment [ so (u-un) is the unemployment gap], and z is an input price shock, in this case the 4 quarter inflation rate in import prices. Each of these series is available from FRED; using the FRED acronyms, PCEPI for the personal consumption expenditure deflator, MICH for University of Michigan’s 1 year inflation expectations, UNRATE for unemployment rate, NROU for natural rate of unemployment, and IR for import prices.

Estimate this relationship using OLS over the 1987-2019Q2 period (first two months of 2019Q2 used to proxy for Q2). This sample period, after accounting for lags, spans the “Great Moderation”.”

From Econbrowser:

“Or, old fogey downloads data, finds a negative relationship, a.k.a. the Phillips Curve…

Much was made of the meeting of minds of AOC and Larry Kudlow regarding the Phillips Curve, to wit (from Bloomberg):

… Ocasio-Cortez said many economists are concerned that the formula “is no longer describing what is happening in today’s economy” — and Powell largely agreed.

“She got it right,” Kudlow told reporters at the White House later on Thursday.

Posted by at 10:03 AM

Labels: Macro Demystified

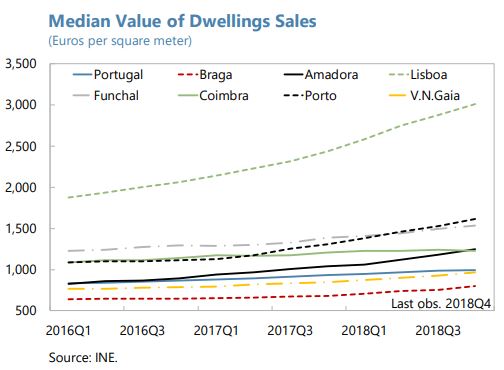

Real Estate Prices in Portugal

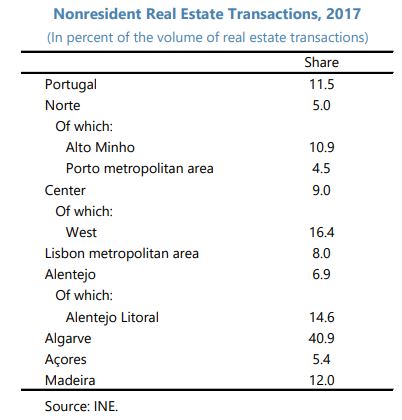

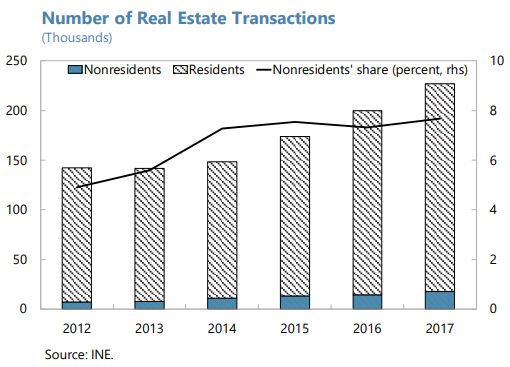

From the IMF’s latest report on Portugal:

“Growth of the Portuguese House Price Index (HPI) decelerated to 9.3 percent y-o-y in 2018:Q4 from its 12.2 percent y-o-y peak in 2018:Q1. Price increases have been more pronounced for existing dwellings, rising 9.5 percent y-o-y in 2018:Q4 and, in particular, in Lisbon and Porto, with the median value per square meter increasing more than 23 percent y-o-y in 2018:Q4. Data from the OECD (…) indicate that the price-to-rent and price-to-income ratios are slightly above their 2000:Q1–2018:Q3 averages, which suggests that housing markets are not significantly overvalued.

A significant part of the transactions driving real estate prices up in key locations are linked to the strong growth in the tourism sector and direct investments by non-residents. The share of purchases by nonresidents in the total number of transactions has strengthened from 2014 (…). Nonresidents were especially active in the higher end of the property market, with the share of nonresident purchases in the total value of transactions in the >€500k segment exceeding 35 percent during 2013–17. These indicators may understate the participation of foreign investors in the real estate market, because some buyers acquire resident status when they buy a property.”

From the IMF’s latest report on Portugal:

“Growth of the Portuguese House Price Index (HPI) decelerated to 9.3 percent y-o-y in 2018:Q4 from its 12.2 percent y-o-y peak in 2018:Q1. Price increases have been more pronounced for existing dwellings, rising 9.5 percent y-o-y in 2018:Q4 and, in particular, in Lisbon and Porto, with the median value per square meter increasing more than 23 percent y-o-y in 2018:Q4. Data from the OECD (…) indicate that the price-to-rent and price-to-income ratios are slightly above their 2000:Q1–2018:Q3 averages,

Posted by at 9:58 AM

Labels: Global Housing Watch

Housing View – July 12, 2019

On the US:

- Lots of folks over 65 are spending a lot on housing – Richard’s Real Estate and Urban Economics Blog

- To Encourage New Housing, Tax It – Wall Street Journal

- Meeting America’s Affordable Housing Needs Requires GSE Reform, and More – The Harvard Joint Center for Housing Studies

- Recession Signals: Home Sales Trend Lower in All Four Regions – Federal Reserve Bank of St. Louis

- A New Approach on Housing Affordability – New York Times

- Kamala Harris’ Plan To End the Racial Homeownership Gap Doubles Down on the Worst Aspects of U.S. Housing Policy – Reason

- Rebounds in Homeownership Have Not Reduced the Gap for Black Homeowners – The Harvard Joint Center for Housing Studies

- Democrats May Inflate Another Housing Bubble – Wall Street Journal

- Can This Factory Produce a Cheaper Apartment? – Citylab

- Don’t look now, but home equity delinquencies are rising – American Banker

On other countries:

- [Chile] Chile’s house prices are rising strongly – Global Property Guide

- [Portugal] Portugal Passes ‘Right to Housing’ Law As Prices Surge – Citylab

On the US:

- Lots of folks over 65 are spending a lot on housing – Richard’s Real Estate and Urban Economics Blog

- To Encourage New Housing, Tax It – Wall Street Journal

- Meeting America’s Affordable Housing Needs Requires GSE Reform, and More – The Harvard Joint Center for Housing Studies

- Recession Signals: Home Sales Trend Lower in All Four Regions – Federal Reserve Bank of St.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts