Friday, March 22, 2019

The Structural Determinants of the Labor Share in Europe

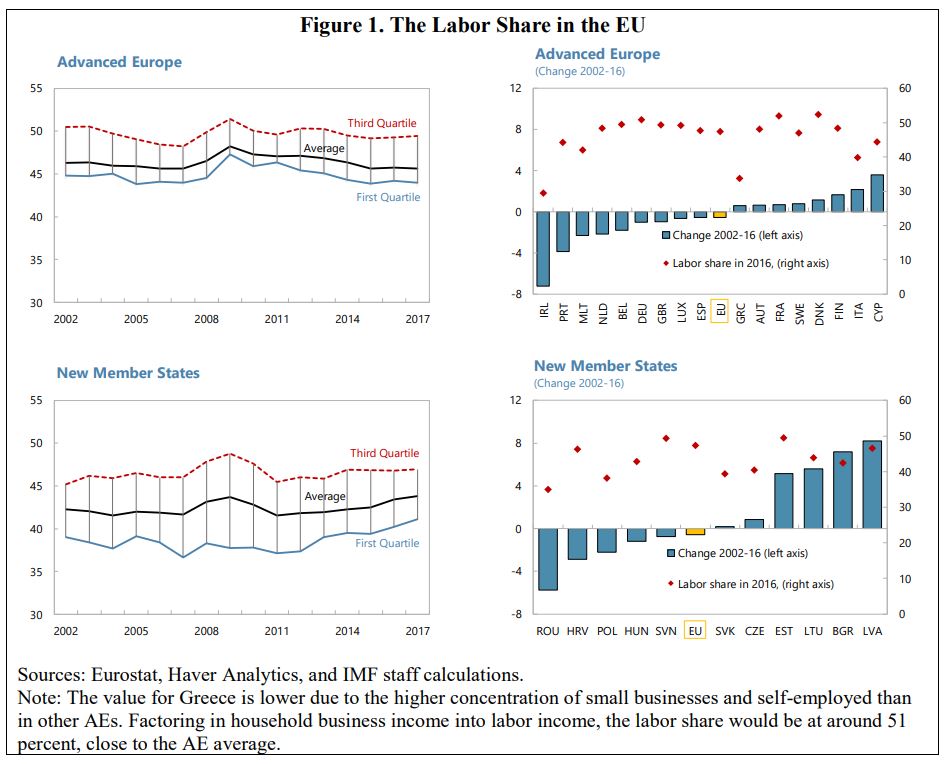

From a new IMF working paper by Dilyana Dimova:

“The labor share in Europe has been on a downward trend. This paper finds that the decline is concentrated in manufacture and among low- to mid-skilled workers. The shifting nature of employment away from full-time jobs and a rollback of employment protection, unemployment benefits and unemployment benefits have been the main contributors. Technology and globalization hurt sectors where jobs are routinizable but helped others that require specialized skills. High-skilled professionals gained labor share driven by productivity aided by flexible work environments, while low- and mid-skilled workers lost labor share owing to globalization and the erosion of labor market safety nets.

The value-added share accrued to labor commonly known as the labor share—the ratio of labor compensation (wages and benefits) to national income—has been on a downward trend in the EU in the last couple of decades (Figure 1). This trend is observed both in recession-hit Advanced Economies (AE) like Ireland, Portugal and Spain as well as in economically prosperous Germany and the Netherlands (Figure 1, upper panels), and began around 2012–13 after the Great Recession (GR). In New Member States (NMS), Estonia, Hungary, Latvia and Lithuania experienced a decline in 2009–15 and are on the rebound (Figure 1, lower panels). Other NMS economies such as Croatia, Poland and Romania have yet to return to their 2002 levels. The positive exception is Bulgaria whose labor share has been on an upward trend due to an economic deepening from relatively low levels.

This paper looks at the evolution of the labor share by industry and by skill level and considers the effect of various structural factors on the EU-wide stagnation and erosion of the labor share. Following Dao et al. (2017), first a shift-share analysis is used to demonstrate the extent to which the downward trend in the labor share is driven by within-sector/skill category declines or by changes across sectors/skill category. The analysis establishes that within-sector/skill category changes account for the majority of labor share fluctuations and provides justification for the structural factor analysis. Then the paper quantifies the extent to which structural drivers track changes in the labor share in 28 EU-member countries, representing both advanced economies and transitional economies, in a cross-country panel study that uses disaggregated data for twelve industry sectors and three skill categories.”

From a new IMF working paper by Dilyana Dimova:

“The labor share in Europe has been on a downward trend. This paper finds that the decline is concentrated in manufacture and among low- to mid-skilled workers. The shifting nature of employment away from full-time jobs and a rollback of employment protection, unemployment benefits and unemployment benefits have been the main contributors. Technology and globalization hurt sectors where jobs are routinizable but helped others that require specialized skills.

Posted by at 4:37 PM

Labels: Inclusive Growth

House Prices in Bulgaria

From the IMF’s latest report on Bulgaria:

“Credit growth has picked up. Both consumer and mortgage loan growth has been buoyant, accompanied by strong housing price increases (averaging 7.5 percent y/y since 2016). Credit to corporates has also been recovering and reached 5.4 percent y/y in 2018, the highest level since 2013, while credit standards have slightly tightened or remained unchanged recently. But non-financial corporate debt remains high among the new member states (NMS)—notwithstanding a marked decline from 106 percent of GDP in 2008 to 80 percent of GDP in 2017. Overall credit-to-GDP ratio remains below the historical trend, with the ratio substantially below the peak reached in 2010.”

From the IMF’s latest report on Bulgaria:

“Credit growth has picked up. Both consumer and mortgage loan growth has been buoyant, accompanied by strong housing price increases (averaging 7.5 percent y/y since 2016). Credit to corporates has also been recovering and reached 5.4 percent y/y in 2018, the highest level since 2013, while credit standards have slightly tightened or remained unchanged recently. But non-financial corporate debt remains high among the new member states (NMS)—notwithstanding a marked decline from 106 percent of GDP in 2008 to 80 percent of GDP in 2017.

Posted by at 4:32 PM

Labels: Global Housing Watch

The Remarkable Renaissance in US Fossil Fuel Production

From Conversable Economist:

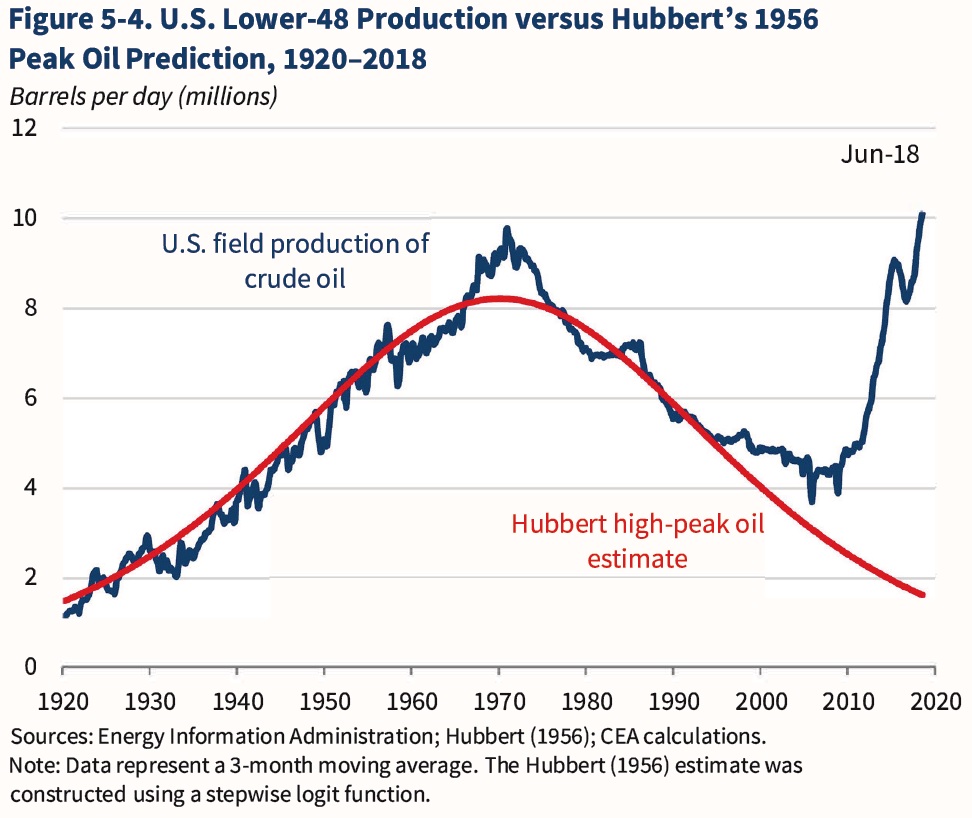

“M. King Hubbert was a big-name geologist who worked much of his career for Shell oil. Back in the 1970s, when OPEC taught the US that the price of oil was set in global markets, discussions of US energy production often began with the “Hubbert curve,” based on a 1956 paper in which Hubbert predicted with considerable accuracy that US oil production would peak around 1970. The 2019 Economic Report of the President devotes a chapter to energy policy, and offers a reminder what happened with Hubbert’s curve.

The red line shows Hubbert’s predicted oil production curve from 1956. The blue line shows actual US oil production in the lower 48 states. At the time of Hubbert’s death in 1989, his forecast looked spot-on. Even by around 2010, his forecast looked pretty good. But for those of us who had built up a habit since the 1970s of looking at US oil production relative to Hubbert’s prediction, the last decade has been a dramatic shock.

Continue reading here.

From Conversable Economist:

“M. King Hubbert was a big-name geologist who worked much of his career for Shell oil. Back in the 1970s, when OPEC taught the US that the price of oil was set in global markets, discussions of US energy production often began with the “Hubbert curve,” based on a 1956 paper in which Hubbert predicted with considerable accuracy that US oil production would peak around 1970. The 2019 Economic Report of the President devotes a chapter to energy policy,

Posted by at 9:29 AM

Labels: Energy & Climate Change

Housing View – March 22, 2019

On cross-country:

- The Total Risk Premium Puzzle – NBER

- Book review: Order without Design: How Markets Shape Cities by Alain Bertaud – New Geography

- New driveway? Home improvements lead AI to hidden gentrification – Reuters

- Inclusionary Housing Policies in Gothenburg, Sweden, and Stuttgart, Germany: The importance of Norms and Institutions – Nordic Journal of Surveying and Real Estate Research

- We don’t have enough to buy a house. How can we invest with similar returns to real estate? – Globe and Mail

On the US:

- The Fed has exacerbated America’s new housing bubble – Financial Times

- The Affordable Home Crisis Continues, But Bold New Plans May Help – Citylab

- US new home sales fall more than forecast in January – Financial Times

- RE Lending Risks Monitor – Federal Reserve Bank of San Francisco

- Do Credit Conditions Move House Prices? – MIT

- Mortgage Loss Severities: What Keeps Them So High? – Federal Reserve Bank of Philadelphia

- Part 3: Renting Vs. Buying. How Important Is Owning A Home? – wbur

- Bay Area leads charge on fixing housing crisis. Will it work for the rest of California? – Los Angeles Times

- Storper Challenges Blanket Upzoning as Solution to Housing Crisis – UCLA

- How Do Homeowners Spend Their Remodeling Dollars? – Harvard Joint Center for Housing Studies

On other countries:

- [Australia] Property, Debt and Financial Stability – Reserve Bank of Australia

- [Australia] Australia’s falling home prices not yet a threat to banks: RBA – Reuters

- [Australia] Australian Housing Slide Deepens as RBA Worries About Consumers – Bloomberg

- [Australia] Australia’s Housing Slump Isn’t Fazing Mortgage Bond Investors – Bloomberg

- [Australia] How Do Crime Rates Affect Property Prices? – Infrastructure Victoria

- [Australia] Foreign investment in Australian residential properties: House prices and growth of housing construction sector – University of Technology, Melbourne

- [Canada] The Age of Leverage – Bank of Canada

- [Canada] Previous housing data understated amount of non-resident buyers in Vancouver and Toronto – Globe and Mail

- [Canada] Trudeau Targets Home-Buying Millennials With Equity Plan – Bloomberg

- [Canada] Not in my neighbour’s back yard? Laneway homes and neighbours’ property values – University of British Columbia

- [China] Housing Policy and Economic Growth in China – Reserve Bank of Australia

- [China] Deeper Cracks in China’s Housing Foundations – Wall Street Journal

- [China] China new house prices pick up pace in February – Financial Times

- [Czech Republic] Czech apartment price rise continues – ING

- [Iceland] Iceland’s house prices rises decelerating rapidly – Global Property Guide

- [India] As property prices rise, more Indian women claim inheritance – Reuters

- [Ireland] Irish house prices cool further as wider inflation remains muted – Reuters

- [Italy] Renaissance Venice had its own “Airbnb problem”—and a solution … – Quartz

- [Japan] Japan’s Regional Land Prices Rise for First Time Since Property Bubble Burst in ’90s – Bloomberg

- [Malaysia] Housing prices in peninsular Malaysia: supported by income, foreign inflow or speculation? – Tunku Abdul Rahman University College

- [Mexico] Mexico’s housing market is strengthening – Global Property Guide

- [Netherlands] Amsterdam Is Trying to Crack Down on Its Rentals Market – Bloomberg

- [Slovak Republic] Slovak Republic’s house price rises continue – Global Property Guide

- [Switzerland] World’s Lowest Interest Rate Brews Trouble for Swiss Property – Bloomberg

- [United Kingdom] Revealed: the fastest ‘double your money’ years for UK property – Financial Times

- [United Kingdom] Properties, prices and pesky Instagrammers – Financial Times

- [United Kingdom] Elephant and Castle shifts from social housing to ‘build to rent’ – Financial Times

- [United Kingdom] How does the land supply system affect the business of UK speculative housebuilding? – UK Collaborative Centre for Housing Evidence

- [Venezuela] Crisis en Venezuela: la tentadora oferta de viviendas de lujo a precio de saldo (y qué tiene que ver el “efecto Guaidó”) – BBC

On cross-country:

- The Total Risk Premium Puzzle – NBER

- Book review: Order without Design: How Markets Shape Cities by Alain Bertaud – New Geography

- New driveway? Home improvements lead AI to hidden gentrification – Reuters

- Inclusionary Housing Policies in Gothenburg, Sweden, and Stuttgart, Germany: The importance of Norms and Institutions – Nordic Journal of Surveying and Real Estate Research

- We don’t have enough to buy a house.

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, March 20, 2019

Fundamental and Speculative Demands for Housing

From a new IMF working paper by Weicheng Lian:

“This paper separates the roles of demand for housing services and belief about future house prices in a house price cycle, by utilizing a feature of user-cost-of-housing that it is sensitive to demand for housing services only. Optimality conditions of producing housing services determine user-cost-of-housing and the elasticity of substitution between land and structures in producing housing services. I find that the impact of demand for housing services on house prices is amplified by a small elasticity of substitution, and demand explained four fifths of the U.S. house price boom in the 2000s.”

From a new IMF working paper by Weicheng Lian:

“This paper separates the roles of demand for housing services and belief about future house prices in a house price cycle, by utilizing a feature of user-cost-of-housing that it is sensitive to demand for housing services only. Optimality conditions of producing housing services determine user-cost-of-housing and the elasticity of substitution between land and structures in producing housing services. I find that the impact of demand for housing services on house prices is amplified by a small elasticity of substitution,

Posted by at 9:03 AM

Labels: Global Housing Watch

Subscribe to: Posts