Monday, February 19, 2018

Labor Market Duality in Korea

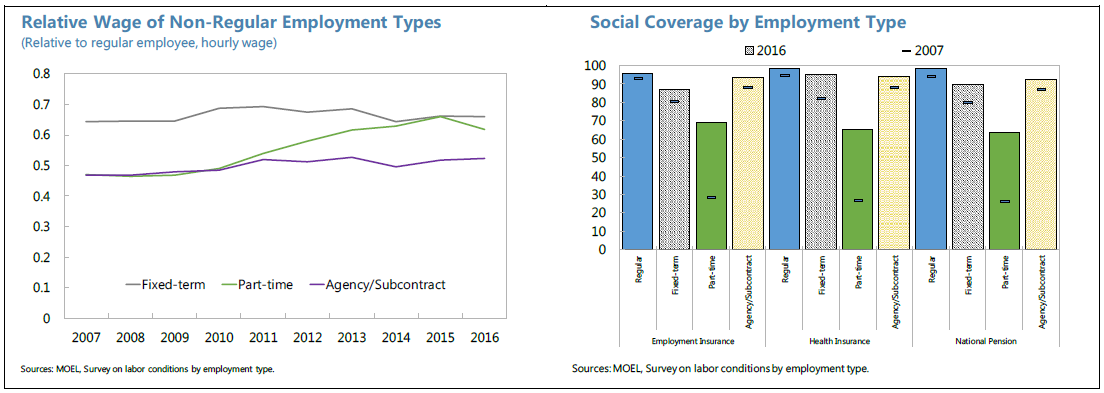

A new IMF report says that “Labor market duality in Korea is a complex issue, which encompasses various types of non-regular workers. Nonetheless, it is particularly prominent among SMEs and in the service sector and disproportionately affects women, the elderly and youth. On a macro level it has likely contributed to increasing inequality, low fertility rates and declining productivity growth. The two main drivers behind duality are various employment protection legislations and large productivity differentials in the product market. A general equilibrium search-and-matching model is applied to model duality and simulate the impact of flexicurity policies. It finds that a well-calibrated introduction of flexicurity could address a number of issues that Korea is facing, such as reducing duality and inequality, and raising productivity and welfare. For this it would be crucial to implement all three pillars to ensure gains are distributed among all individuals.”

A new IMF report says that “Labor market duality in Korea is a complex issue, which encompasses various types of non-regular workers. Nonetheless, it is particularly prominent among SMEs and in the service sector and disproportionately affects women, the elderly and youth. On a macro level it has likely contributed to increasing inequality, low fertility rates and declining productivity growth. The two main drivers behind duality are various employment protection legislations and large productivity differentials in the product market.

Posted by at 9:22 PM

Labels: Inclusive Growth

Friday, February 16, 2018

Housing View – February 16, 2018

On cross-country:

- Recent house price increases and housing affordability – European Central Bank

- European Mortgage Markets at Risk from Policy Tightening – Continuum 360

- Sovereign wealth funds quadruple investment in student housing – Financial Times

- Which foreign countries will grant me citizenship if I invest? – Financial Times

On the US:

- Housing Sentiment at New Survey High on Higher Home Price Expectations – Fannie Mae

- To increase employment among housing-assisted families, don’t pull the rug out from under them – Urban Institute

- Cut HUD, Fix Housing – Cato Institute

- Construction Wages: Who Makes the Most and Where? – BuildZoom

- A closer look at the fifteen-year drop in black homeownership – Urban Institute

- Mortgage Supply and Housing Rents – The Review of Financial Studies

On other countries:

- [Canada] British Columbia to curb housing speculation, crack down on tax cheats – Reuters

- [Canada] B.C. throne speech—government vows action on high house prices, but ignores their cause – Fraser Institute

- [Canada] Speculation is best hope for housing supply, developers say – Business Vancouver

- [China] China is trying new ways of skimming housing-market froth – Economist

- [Malaysia] Unsold homes in Malaysia rise to decade high in 2017 – Reuters

- [Sweden] Reduced housing construction is subduing GDP growth – Riksbank

- [Sweden] Household Finances Exposed to Falling House Prices – Continuum Economics

Photo by Aliis Sinisalu

On cross-country:

- Recent house price increases and housing affordability – European Central Bank

- European Mortgage Markets at Risk from Policy Tightening – Continuum 360

- Sovereign wealth funds quadruple investment in student housing – Financial Times

- Which foreign countries will grant me citizenship if I invest? – Financial Times

On the US:

- Housing Sentiment at New Survey High on Higher Home Price Expectations – Fannie Mae

- To increase employment among housing-assisted families,

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, February 14, 2018

UK’s Housing Market

From the IMF’s latest report on the UK:

“Housing supply. Efforts should continue to boost housing supply, including by easing planning restrictions and reforming property taxes to encourage more efficient use of the housing stock. Increasing supply would support near-term growth, facilitate labor mobility across regions, support financial stability by making homes more affordable, and promote social cohesion by reducing wealth inequality.”

From the IMF’s latest report on the UK:

“Housing supply. Efforts should continue to boost housing supply, including by easing planning restrictions and reforming property taxes to encourage more efficient use of the housing stock. Increasing supply would support near-term growth, facilitate labor mobility across regions, support financial stability by making homes more affordable, and promote social cohesion by reducing wealth inequality.”

Posted by at 10:17 AM

Labels: Global Housing Watch

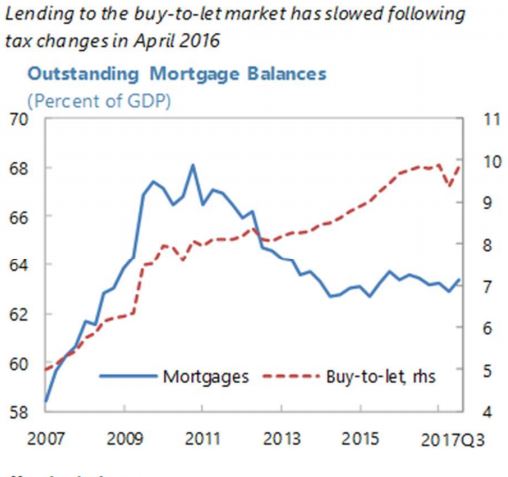

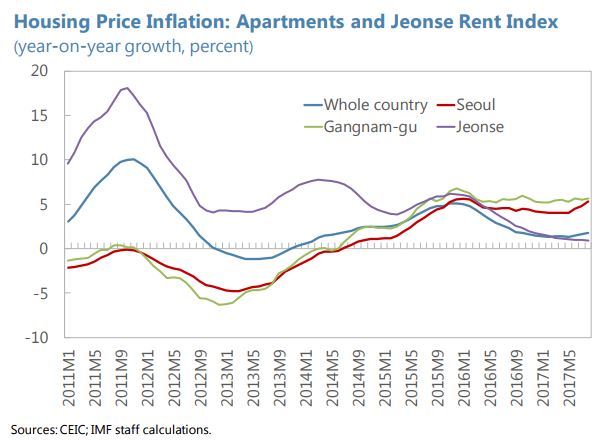

House Prices in Korea

From the IMF’s latest report on Korea:

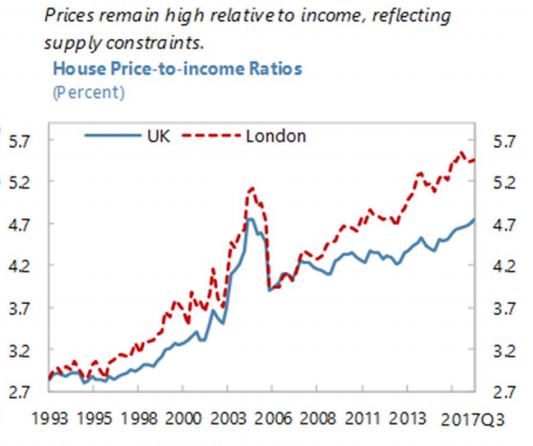

“The financial sector is sound, with high and rising household debt the main domestic financial stability risk. Household debt exceeds 90 percent of GDP, increasing vulnerability to both a housing price correction and a sharp rise in interest rates. A tightening of macroprudential measures has helped slow household credit growth to 7.8 percent year-on-year in October, from the 12-percent average annual growth rate in 2016. The increase in house prices nationally has slowed to about 1 percent year-over-year; but in Seoul apartment prices are still rising at a nearly 5-percent annual rate. Macroprudential policy measures, including some targeting speculative buying of apartments in Seoul, should help stabilize prices. According to staff analysis, the overall housing prices level is in line with fundamentals. However, there remains a risk of a price correction in the region around Seoul, which experienced larger price increase and where the surge in supply from the construction boom could weigh on prices.”

From the IMF’s latest report on Korea:

“The financial sector is sound, with high and rising household debt the main domestic financial stability risk. Household debt exceeds 90 percent of GDP, increasing vulnerability to both a housing price correction and a sharp rise in interest rates. A tightening of macroprudential measures has helped slow household credit growth to 7.8 percent year-on-year in October, from the 12-percent average annual growth rate in 2016.

Posted by at 10:03 AM

Labels: Global Housing Watch

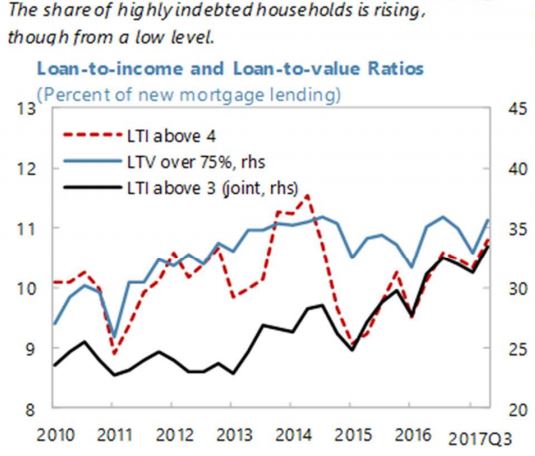

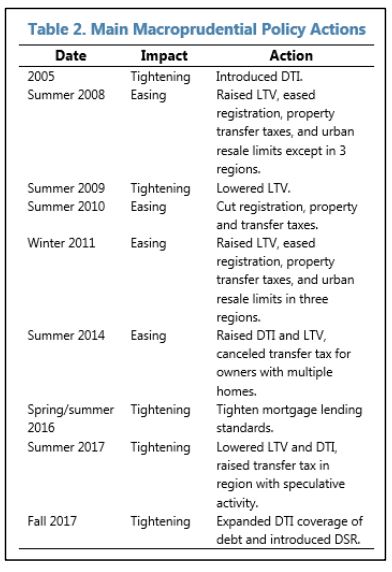

Korea: Macroprudential Policy and High Household Debt

From the latest IMF’s report on Korea:

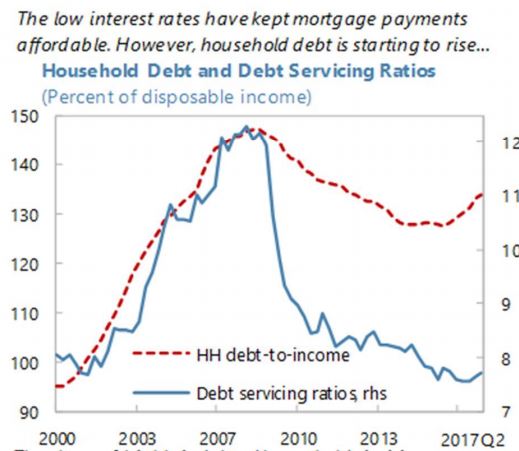

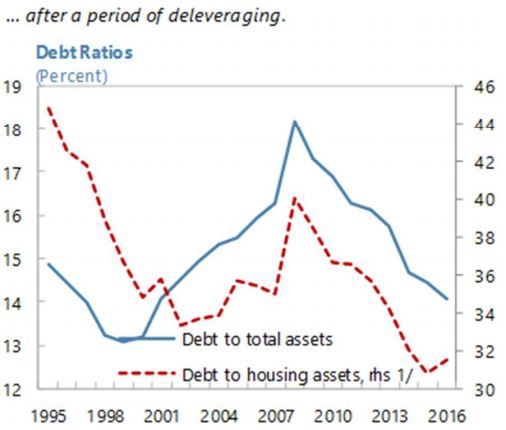

“Macroprudential policies are being extensively used to curb risks from high household debt and credit growth. A broad range of macroprudential instruments that have been tightened and new ones introduced (Table 2). The loan-to-value (LTV) and debt-to-income (DTI) ratios were reduced to record lows of 40 percent, and are now well below recent highs of 70 and 60 percent, respectively, to which they were increased in August 2014. And, a lower level of 30 percent was set for borrowers with multiple mortgages and in designated regions of speculative activity, mostly around Seoul. In October 2017, the DTI was effectively tightened further by broadening the range of debt subject to it. Also announced is a new, debt service ratio (DSR) with comprehensive coverage of all household debts, which will be implemented for banks in mid-2018; and then for NBFIs at the start of 2019.

Evidence suggests that this macroprudential tightening will be effective. The growth in credit to households has slowed significantly over the last few months. Moreover, speculative purchases of apartments before construction is has diminished. An event study analysis by Federal Reserve Board economists finds that hikes in LTVs and DTIs have been effective in slowing credit growth and housing price increases. New cross-country panel regression analysis show that use of LTVs and DTIs is effective in reducing real household credit growth across 34 advanced and emerging market economies, including Korea.”

From the latest IMF’s report on Korea:

“Macroprudential policies are being extensively used to curb risks from high household debt and credit growth. A broad range of macroprudential instruments that have been tightened and new ones introduced (Table 2). The loan-to-value (LTV) and debt-to-income (DTI) ratios were reduced to record lows of 40 percent, and are now well below recent highs of 70 and 60 percent, respectively, to which they were increased in August 2014.

Posted by at 9:55 AM

Labels: Global Housing Watch

Subscribe to: Posts