Wednesday, May 9, 2018

Low Inflation in Asia

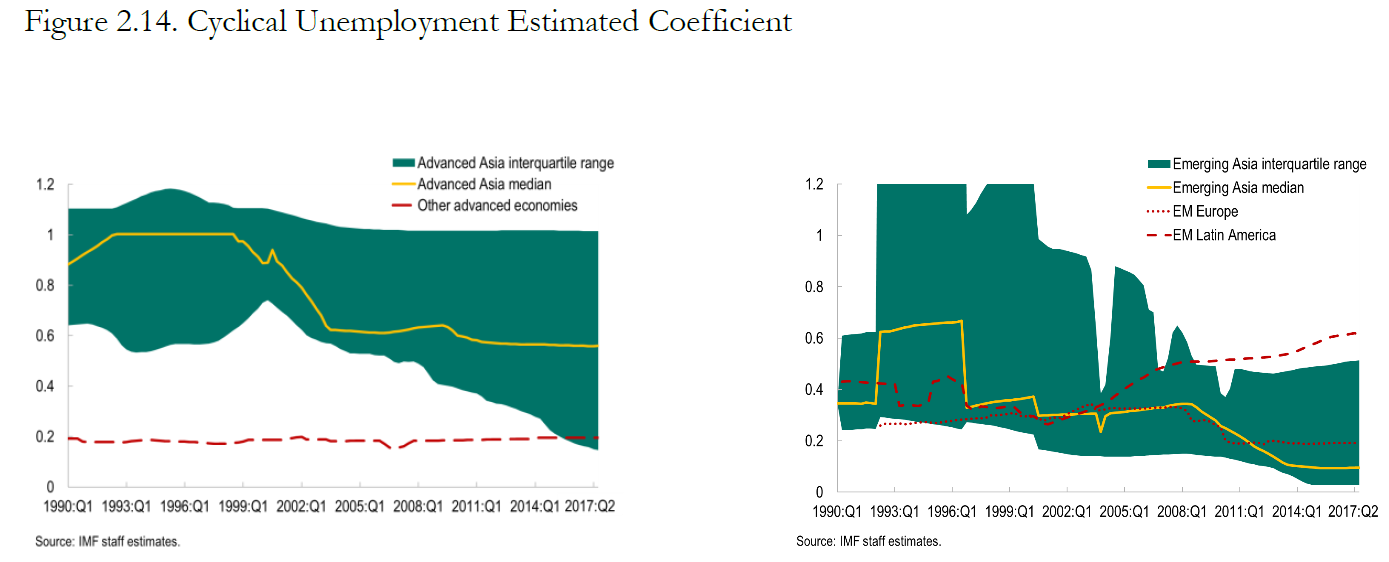

From the new IMF Regional Economic Outlook for Asia Pacific:

“The main findings are as follows:

- Recent low inflation has been driven mainly by temporary forces, including imported inflation. Phillips curve estimation indicates that weaker import prices, including low commodity prices, contributed to half of the undershooting of inflation targets in advanced Asia and most of the undershooting in emerging Asia in recent years. In addition, China seems to have played an important role in driving both global and regional inflation. More generally, an analysis looking at temporary and trend components suggests that temporary shocks have accounted for the bulk of the recent reduction in inflation.

- The inflation process has become more backward-looking. While inflation expectations are generally relatively well anchored, especially in advanced Asia and in economies with inflation-targeting frameworks, the importance of expectations in driving inflation has declined in recent years with past inflation playing a larger role.

- The sensitivity of inflation to the unemployment gap has declined. There seems to be a flattening of the Phillips curve compared to the 1990s in advanced Asia and a similar but more continuous flattening in emerging Asia. Outside of Asia, the slope of the Phillips curve seems to have been more stable.”

“The main policy implications of the findings are:

- Central banks should be vigilant in responding to early signs of inflationary pressure, including from global factors. A sudden increase in inflation may then persist, and disinflating may be costly if sensitivity of inflation to the unemployment gap has declined.

- It will be important to strengthen monetary policy frameworks and improve central bank communications in order both to increase the role of expectations in driving inflation and to maintain expectations anchored to targets.

- To mitigate the role of imported inflation, exchange rates should be allowed to adjust more flexibly.

- In principle, the monetary policy response to commodity price shocks should be to accommodate first- round effects but not the second-round effects.”

From the new IMF Regional Economic Outlook for Asia Pacific:

“The main findings are as follows:

- Recent low inflation has been driven mainly by temporary forces, including imported inflation. Phillips curve estimation indicates that weaker import prices, including low commodity prices, contributed to half of the undershooting of inflation targets in advanced Asia and most of the undershooting in emerging Asia in recent years. In addition, China seems to have played an important role in driving both global and regional inflation.

Posted by at 3:38 PM

Labels: Inclusive Growth

Tuesday, May 8, 2018

21st-century Indian economists

For a list of 21st-century Indian economists, click here.

For a list of 21st-century Indian economists, click here.

Posted by at 1:09 PM

Labels: Profiles of Economists

20th-century Indian economists

For a list of 20th-century Indian economists, click here.

For a list of 20th-century Indian economists, click here.

Posted by at 10:27 AM

Labels: Profiles of Economists

Saturday, May 5, 2018

Is inflation dead?

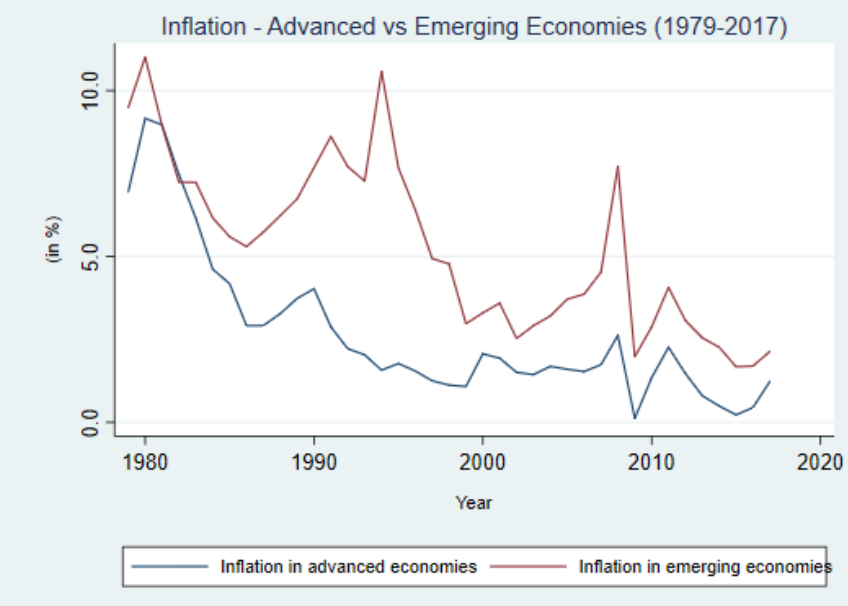

From a presentation by Surjit S Bhalla:

“Some facts to consider about CPI inflation:

- Inflation in the US averaged 1.9 % between 1996 and 2009; and 70 basis points lower over the next eight years.

- A little appreciated inflation fact is that the mean inflation rate in 21 Advanced Economies (AE) excluding the US, averaged some 25 bp less than the US.

- Charts 1 and 2 document median inflation in the Advanced, and the Rest, economies from 1979 to 2017, and 1996 to 2017.

- Note that inflation decline set in prior to 2007 , and in reality started somewhere in the mid-1990s.”

“Explanations for the inflation slowdown:

- Fiscal deficit trends provide zero clues about this slowdown in inflation.

- World GDP growth [IMF weights] was the highest 1996-2007.

- World growth has moved inversely to world inflation.

- Output gap, or considerations thereof, do not explain, inflation slowdown.

- Demography (changes in dependency ratio) does explain some of the decline in inflation.

- However, the most consistent explanation for the decline in inflation is the large increase in college graduates in the Rest of the world compared to such supply in the West (Advanced Economies)”

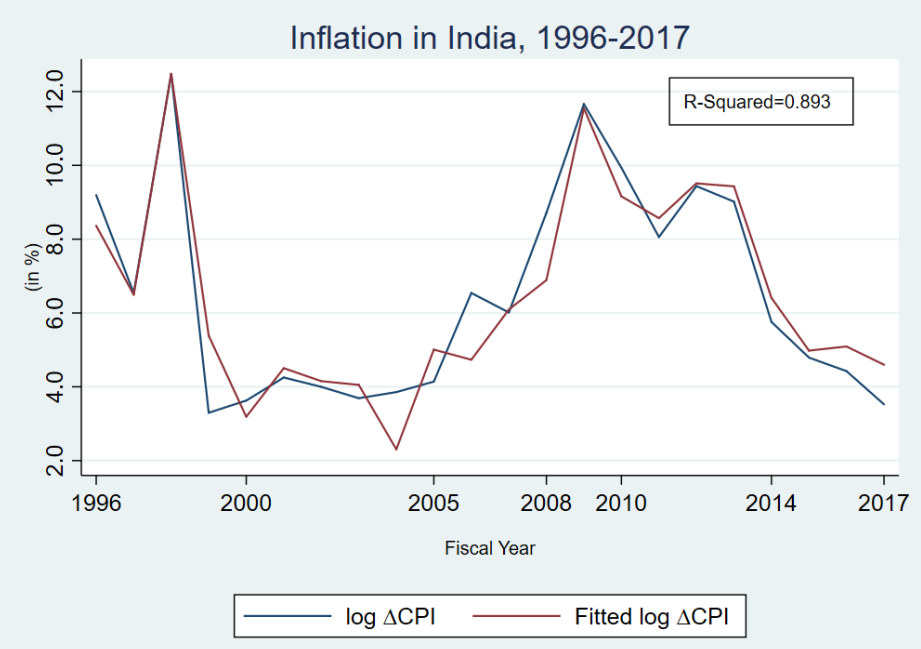

“What explains Indian inflation? – Procurement prices and rural wage growth:

- Procurement prices and rural wage growth matters for Indian inflation, not much else.

- Further, the impact of procurement prices is diminishing over time, especially over the last three years.

- Each 1% increase in (lagged) procurement prices leads to a 12 bp increase in inflation.

- Each 1 % increase in rural wages leads to a 28 bp increase in inflation.

- The model is able to explain 89 % of the variation in log inflation, 1996-2017.”

In my recent paper with Sangyup Choi, Davide Furceri, Saurabh Mishra, and Marcos Poplawski-Ribeiro, we study the dynamic impact of global oil price shocks on domestic inflation. We find that a 10 percent increase in global oil inflation increases domestic inflation by about 0.4 percentage point on impact, with the effect vanishing after two years and being similar between advanced and developing economies. My paper is available here. The working paper version is available here.

From a presentation by Surjit S Bhalla:

“Some facts to consider about CPI inflation:

- Inflation in the US averaged 1.9 % between 1996 and 2009; and 70 basis points lower over the next eight years.

- A little appreciated inflation fact is that the mean inflation rate in 21 Advanced Economies (AE) excluding the US, averaged some 25 bp less than the US.

- Charts 1 and 2 document median inflation in the Advanced,

Posted by at 2:19 PM

Labels: Inclusive Growth

Spring 2018 Journal of Economic Perspectives is Online

From a new post by Timothy Taylor:

“I was hired back in 1986 to be the Managing Editor for a new academic economics journal, at the time unnamed, but which soon launched as the Journal of Economic Perspectives. The JEP is published by the American Economic Association, which back in 2011 decided–to my delight–that it would be freely available on-line, from the current issue back to the first issue. Here, I’ll start with Table of Contents for the just-released Spring 2018 issue, which in the Taylor household is known as issue #124. Below that are abstracts and direct links for all of the papers. I will blog more specifically about some of the papers in the next week or two, as well.”

From a new post by Timothy Taylor:

“I was hired back in 1986 to be the Managing Editor for a new academic economics journal, at the time unnamed, but which soon launched as the Journal of Economic Perspectives. The JEP is published by the American Economic Association, which back in 2011 decided–to my delight–that it would be freely available on-line, from the current issue back to the first issue.

Posted by at 1:15 PM

Labels: Macro Demystified

Subscribe to: Posts