Thursday, May 17, 2018

Biggest fear for world growth is fear itself as markets fret

A new Bloomberg post by Anchalee Worrachate and David Goodman says that: “While policy makers insist the global economy’s low-inflation expansion looks intact despite a first quarter slowdown, investors are presenting challenges. Rising bond yields, a jump in the price of oil beyond $70 a barrel, skittish stocks and cracks in credit could all end up undermining growth.” “The worry is that unless markets start buying into the more optimistic outlook, their pessimism will become self-fulfilling by causing consumers and companies to lose confidence and slow spending. The Bank for International Settlements warned last year that the next recession will perhaps be triggered by a financial cycle bust, mirroring the events of 2001 and 2008.”

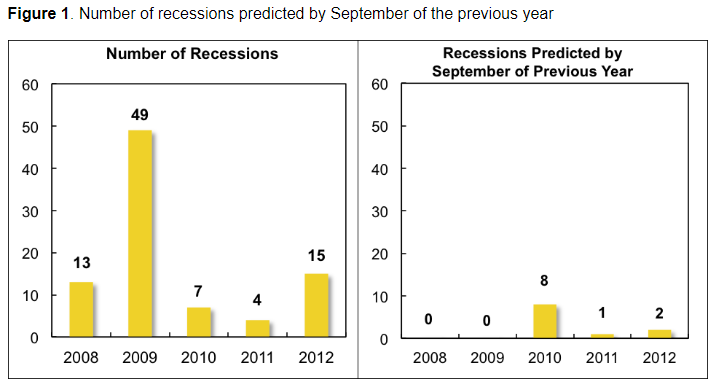

This post also notes my research that “the optimism of analysts may be cold comfort to some investors. A 2014 study by Prakash Loungani of the International Monetary Fund found that not one of 49 recessions suffered around the world in 2009 had been predicted by the consensus of economists a year earlier.”

Continue reading here. My Vox post is available here. My new paper on forecasting recessions is available here.

A new Bloomberg post by Anchalee Worrachate and David Goodman says that: “While policy makers insist the global economy’s low-inflation expansion looks intact despite a first quarter slowdown, investors are presenting challenges. Rising bond yields, a jump in the price of oil beyond $70 a barrel, skittish stocks and cracks in credit could all end up undermining growth.” “The worry is that unless markets start buying into the more optimistic outlook, their pessimism will become self-fulfilling by causing consumers and companies to lose confidence and slow spending.

Posted by at 11:08 AM

Labels: Forecasting Forum

IEO Releases an Update to its 2007 evaluation of Structural Conditionality in IMF-Supported Programs

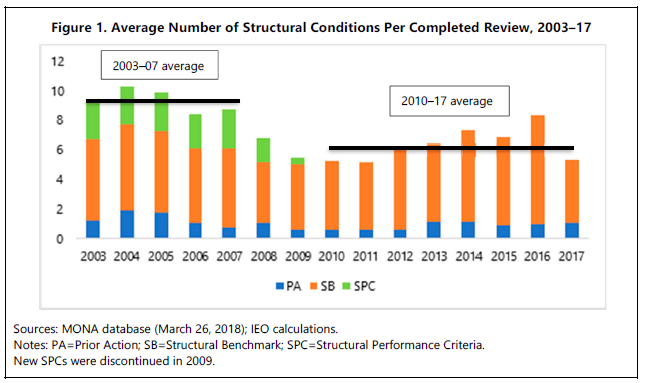

The IEO just released an Evaluation Update Report revisiting its 2007 evaluation of Structural Conditionality in IMF-Supported Programs. The report was published along with a statement by the Managing Director.

“The evaluation found that, notwithstanding the streamlining initiative launched in 2000, structural conditionality was still used extensively and program documents were not sufficiently clear about the criticality of structural conditions. Moreover, the report concluded that most structural conditions had little structural depth, only about half were implemented on time, and compliance was only weakly correlated with subsequent progress in structural reforms.”

“Following the evaluation, use of IMF lending surged in the context of the global financial crisis in 2008 and the euro area crisis in 2010. Use of structural conditionality in euro area crisis programs raised issues related to working with regional partners. Fund program design and implementation over this period was informed by revisions to staff guidance in 2008, 2010, and 2014, and the Review of Conditionality completed in 2012.”

The IEO just released an Evaluation Update Report revisiting its 2007 evaluation of Structural Conditionality in IMF-Supported Programs. The report was published along with a statement by the Managing Director.

“The evaluation found that, notwithstanding the streamlining initiative launched in 2000, structural conditionality was still used extensively and program documents were not sufficiently clear about the criticality of structural conditions. Moreover, the report concluded that most structural conditions had little structural depth,

Posted by at 10:54 AM

Labels: Inclusive Growth

Tuesday, May 15, 2018

Poverty and inequality in Latin America

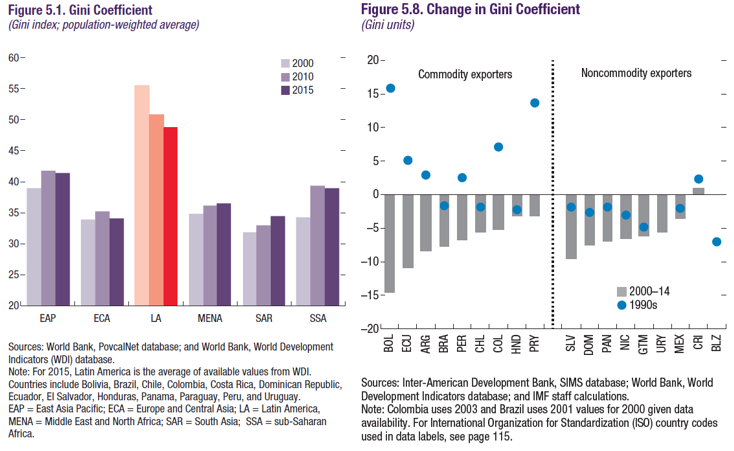

The new IMF Regional Economic Outlook says that “Latin America has made impressive progress in reducing inequality and poverty since the turn of the century, although it remains the most unequal region in the world. The declines in inequality and poverty were particularly pronounced for commodity exporters during the commodity boom. Much of the progress reflected real labor income gains for lower-skilled workers, especially in services, with a smaller but positive role for government transfers. With the commodity boom over, a tighter fiscal envelope, and poverty rates already edging up in some countries, policies will have to be carefully recalibrated to sustain social progress. Increasing personal income tax revenues while rebalancing spending could help maintain key social transfers and infrastructure spending. Better targeting of social transfers and reforming decentralization frameworks also have an important role to play.”

The new IMF Regional Economic Outlook says that “Latin America has made impressive progress in reducing inequality and poverty since the turn of the century, although it remains the most unequal region in the world. The declines in inequality and poverty were particularly pronounced for commodity exporters during the commodity boom. Much of the progress reflected real labor income gains for lower-skilled workers, especially in services, with a smaller but positive role for government transfers.

Posted by at 3:16 PM

Labels: Inclusive Growth

Fiscal Consolidation and Income Inequality in Latin America and the Caribbean

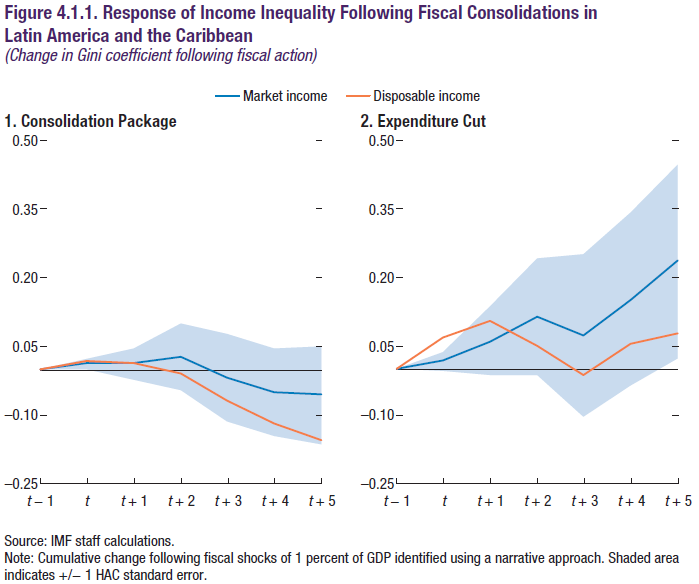

The new IMF Regional Economic Outlook finds that “Fiscal consolidations have very little effects on income inequality in LAC. Point estimates are positive but very small––the market Gini increases by 0.03 units after two years––and are not statistically significant (Figure 4.1.1, panel 1). This is despite a reduction in output of about 1 percent and an increase in unemployment of 0.3 of a percentage point, as demonstrated in the main text. Focusing on the distribution of disposable income does not affect these results, with the Gini coefficient being relatively insensitive to fiscal consolidation shocks.”

It also notes my previous works that “For advanced economies, there is evidence that fiscal consolidation tends to increase income inequality, with especially strong effects when the consolidation is spending-based (Ball and others 2013; Furceri, Jalles, and Loungani 2015; Woo and others 2017).”

Ball, Furceri, Leigh, and Loungani (2013) is available here. Furceri, Jalles, and Loungani (2015) is available here.

The new IMF Regional Economic Outlook finds that “Fiscal consolidations have very little effects on income inequality in LAC. Point estimates are positive but very small––the market Gini increases by 0.03 units after two years––and are not statistically significant (Figure 4.1.1, panel 1). This is despite a reduction in output of about 1 percent and an increase in unemployment of 0.3 of a percentage point, as demonstrated in the main text. Focusing on the distribution of disposable income does not affect these results,

Posted by at 2:48 PM

Labels: Inclusive Growth

The macroeconomic effects of fiscal consolidation in Latin America and the Caribbean

The new IMF Regional Economic Outlook finds that “fiscal multipliers in the region are estimated to lie between 0.5 and 1.1–suggesting that consolidation will be more contractionary than previously thought. Nevertheless, these estimates are small enough to suggest that consolidations will improve the region’s debt dynamics, even in the short run. Since expenditure multipliers vary according to the type of instrument used, consolidation plans should preserve public investment to support growth and employment.”

The new IMF Regional Economic Outlook finds that “fiscal multipliers in the region are estimated to lie between 0.5 and 1.1–suggesting that consolidation will be more contractionary than previously thought. Nevertheless, these estimates are small enough to suggest that consolidations will improve the region’s debt dynamics, even in the short run. Since expenditure multipliers vary according to the type of instrument used, consolidation plans should preserve public investment to support growth and employment.”

Posted by at 2:33 PM

Labels: Inclusive Growth

Subscribe to: Posts