Thursday, June 21, 2018

Differences in consumption baskets across households and the distributional consequences of monetary policy

From a new VOX post:

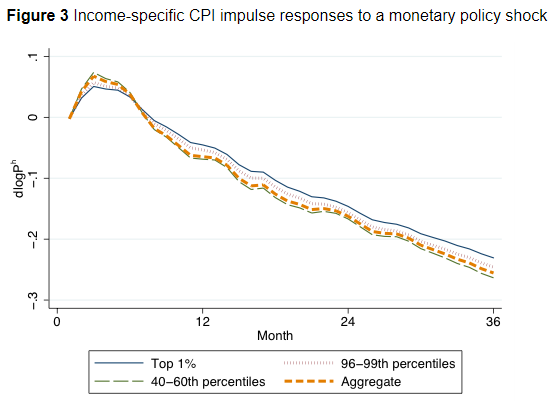

“Monetary policy shocks can affect different types of agents differently. These distributional effects can have important consequences for policy effectiveness. Using US data, this column explores how shocks differentially affect the prices faced by households with different incomes. The results suggest that middle-income households’ consumption baskets have more volatile prices than those of high-income households, and they are therefore more exposed to monetary policy shocks.”

“[…] Figure 3 plots the impulse responses for selected income percentile-specific CPIs. The monetary policy shock is a 25 basis-point increase in the Federal Funds rate on impact, thus a contraction. The consumption price indices of the high-income households react substantially less to monetary policy shocks than those for the middle of the income distribution. The difference is economically meaningful. After 12 months, the top 1% households’ CPI responds by 34% less, and the 96-99th percentile households by 22% less, than the CPI of the households in the middle of the income distribution (40th-60th percentiles). After 24 months, the differences are still 12% and 6%, respectively.”

From a new VOX post:

“Monetary policy shocks can affect different types of agents differently. These distributional effects can have important consequences for policy effectiveness. Using US data, this column explores how shocks differentially affect the prices faced by households with different incomes. The results suggest that middle-income households’ consumption baskets have more volatile prices than those of high-income households, and they are therefore more exposed to monetary policy shocks.”

Posted by at 9:41 AM

Labels: Inclusive Growth

Alongside rising top incomes, the level of living of America’s poorest has fallen

From a new VOX posts:

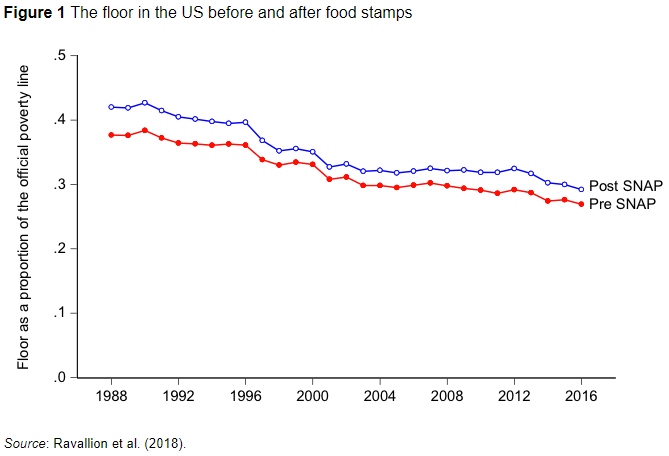

“When the poorest gain, the lower bound, or ‘floor’, of the distribution of living standards rises. Using microdata spanning the last 30 years, this column argues that the floor in the US has been sinking, alongside rising top incomes. The floor would have fallen further without public spending on food stamps, which helped protect the poorest in the wake of the 2008 financial crisis.”

“Figure 1 gives our estimates of the floor before and after SNAP. Since the official poverty thresholds vary by family size and composition, it is simpler to express the floor as a proportion of the threshold. The mean post-SNAP floor is about 36% of the official threshold. For a family of four, with two adults and two children, the threshold was about $16.50 per person per day in 2015. The floor in that year’s prices is $5.89 a day post-SNAP, while the pre-SNAP value is $5.40. ”

From a new VOX posts:

“When the poorest gain, the lower bound, or ‘floor’, of the distribution of living standards rises. Using microdata spanning the last 30 years, this column argues that the floor in the US has been sinking, alongside rising top incomes. The floor would have fallen further without public spending on food stamps, which helped protect the poorest in the wake of the 2008 financial crisis.”

“Figure 1 gives our estimates of the floor before and after SNAP.

Posted by at 9:38 AM

Labels: Inclusive Growth

Wednesday, June 20, 2018

Coping with Natural Disaster Risks in Sri Lanka

From the IMF’s latest report on Sri Lanka:

“Sri Lanka has been prone to weather-related natural disasters, possibly reflecting climate change. While the government has started to build up resiliency against disasters by introducing disaster insurance schemes and increasing mitigation spending, it can further improve disaster preparedness by undertaking policy measures in the near term. First, a contingency budget for emergency cash support and infrastructure rehabilitation can be introduced within the budget. Second, the planned introduction of an automatic pricing mechanism for electricity, combined with well-targeted safety nets, can contain fiscal risks from droughts. Third, the risk management of disaster insurance schemes can be improved to maximize its effectiveness for post-disaster reconstruction while minimizing costs. Beyond the near term, there is a need to develop a comprehensive disaster risk financing strategy that is consistent with Sri Lanka’s debt sustainability, and build up capacity for innovative risk transfer approaches such as parametric insurance.”

From the IMF’s latest report on Sri Lanka:

“Sri Lanka has been prone to weather-related natural disasters, possibly reflecting climate change. While the government has started to build up resiliency against disasters by introducing disaster insurance schemes and increasing mitigation spending, it can further improve disaster preparedness by undertaking policy measures in the near term. First, a contingency budget for emergency cash support and infrastructure rehabilitation can be introduced within the budget.

Posted by at 1:53 PM

Labels: Energy & Climate Change

Female Labor Force Participation: A New Engine of Growth for Sri Lanka?

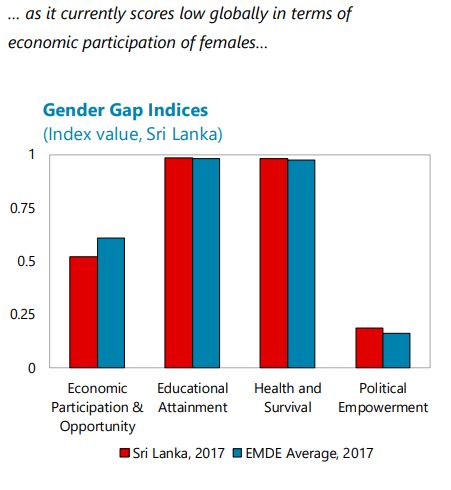

From the IMF’s latest report on Sri Lanka:

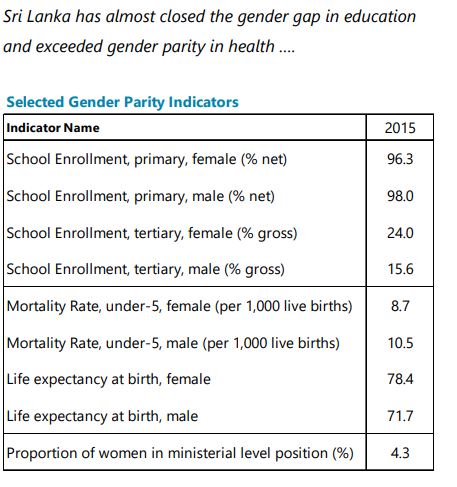

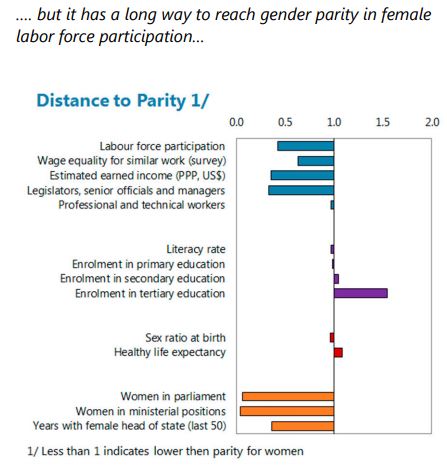

“Sri Lanka has been a trendsetter in the region in advancing gender parity in education and health. Yet, this has not been reflected in more active female labor force participation (FLFP), which is low compared to its emerging market peers and even some low-income developing countries in the region. Closing this gap is especially important as Sri Lanka faces an aging population with a labor force that could start shrinking as early as 2026. Given the potential for significant economic gains from integrating the female labor force into the labor market, the authorities’ Vision 2025 identifies policies to bridge this gap. Specifically, the Sri Lankan authorities aim to provide child care facilities, improve access to transportation, facilitate part-time and flexible work arrangements, improve maternity benefits for private sector employees, and increase access to tertiary education and vocational training. While these measures are steps in the right direction, Sri Lanka may also benefit from a more systematic approach through implementing gender responsive budgeting.”

From the IMF’s latest report on Sri Lanka:

“Sri Lanka has been a trendsetter in the region in advancing gender parity in education and health. Yet, this has not been reflected in more active female labor force participation (FLFP), which is low compared to its emerging market peers and even some low-income developing countries in the region. Closing this gap is especially important as Sri Lanka faces an aging population with a labor force that could start shrinking as early as 2026.

Posted by at 1:49 PM

Labels: Inclusive Growth

Housing Market in Sri Lanka

From the IMF’s latest report on Sri Lanka:

- “Credit growth decelerated gradually to 14.7 percent (y/y) in December 2017 from its 28.5 percent peak in July 2016. However, credit to construction continued to grow rapidly at around 22.5 percent in 2017, reflecting buoyant real estate markets for both personal and commercial properties. Land prices in Colombo appreciated by 10.4 percent (y/y) in December 2017. Real lending rates stood at above 5 percent for most of 2017 but increased to about 7 percent in February 2018 with the deceleration in inflation. “

- “The authorities viewed the financial system as well-capitalized and stable. They did not see systemic risks arising from credit to the construction sector but agreed on the need to remain vigilant, especially in high segments of the real estate market. “

From the IMF’s latest report on Sri Lanka:

- “Credit growth decelerated gradually to 14.7 percent (y/y) in December 2017 from its 28.5 percent peak in July 2016. However, credit to construction continued to grow rapidly at around 22.5 percent in 2017, reflecting buoyant real estate markets for both personal and commercial properties. Land prices in Colombo appreciated by 10.4 percent (y/y) in December 2017. Real lending rates stood at above 5 percent for most of 2017 but increased to about 7 percent in February 2018 with the deceleration in inflation.

Posted by at 1:31 PM

Labels: Global Housing Watch

Subscribe to: Posts