Monday, June 25, 2018

The Macroeconomic and Distributional Implications of Fiscal Consolidations in Low-income Countries

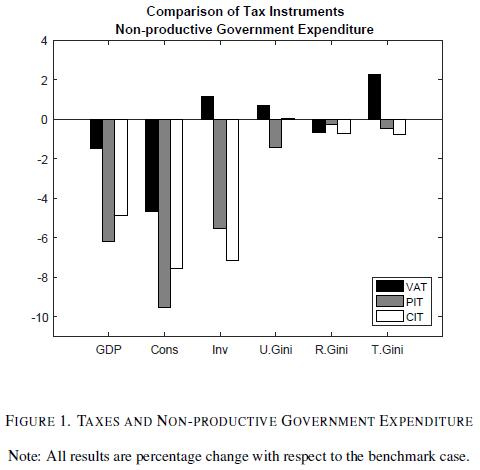

From a new IMF working paper:

“In this paper, we quantitatively investigate the macroeconomic and distributional impacts of fiscal consolidations in low-income countries through VAT, PIT, and CIT. We find that VAT has the least efficiency costs but is highly regressive, while PIT and CIT lead to higher output and consumption drop, but have better distributional implications. Further, we find that cash transfers targeting rural households are able to mitigate the negative distributional impacts of VAT, while public investment shows almost no distributional impacts.”

“Our results suggest that low-income countries indeed face very different equity-efficiency tradeoffs comparing to advanced economies due to their unique economic structure. It therefore is important to investigate quantitatively the impacts of other tax instruments that have been extensively studied under the environment of advanced economies. For instance, we believe that the optimal progressivity of income tax is also a critically important feature in low-income countries. It is also interesting to study whether and how will classical optimal taxation results under complete markets change when migrated to an economy resembling low-income countries. Another limitation of our study is the omission of transitional dynamics in our model, which is important to the evaluation of short-run welfare effects. We leave these extensions to future work.”

From a new IMF working paper:

“In this paper, we quantitatively investigate the macroeconomic and distributional impacts of fiscal consolidations in low-income countries through VAT, PIT, and CIT. We find that VAT has the least efficiency costs but is highly regressive, while PIT and CIT lead to higher output and consumption drop, but have better distributional implications. Further, we find that cash transfers targeting rural households are able to mitigate the negative distributional impacts of VAT,

Posted by at 9:40 AM

Labels: Inclusive Growth

Christopher Pissarides: “I knew the route to happiness was a good job”

From LSE Business Review:

“Q: What’s your personal interest in the Future of Work?

From my late teens – well before ‘good work’ became the fashionable concept that it is today – I knew the route to happiness was a good job. Work is where most of us spend most of our waking time and it is at the heart of family life. It’s also the driving force behind our local and national economies. Work connects the experiences and living standards of individuals to the economic and social health of the country. Knowing this has driven my own working life. I’ve researched employment, unemployment and job creation for over 40 years now, concentrating on the social and economic conditions needed to create good and long-lasting work.’

Continue reading here. Also see my profile of Christopher Pissarides here.

From LSE Business Review:

“Q: What’s your personal interest in the Future of Work?

From my late teens – well before ‘good work’ became the fashionable concept that it is today – I knew the route to happiness was a good job. Work is where most of us spend most of our waking time and it is at the heart of family life. It’s also the driving force behind our local and national economies.

Posted by at 9:39 AM

Labels: Profiles of Economists

Friday, June 22, 2018

The Effects of Weather Shocks on Economic Activity: What are the Channels of Impact?

From a new IMF working paper:

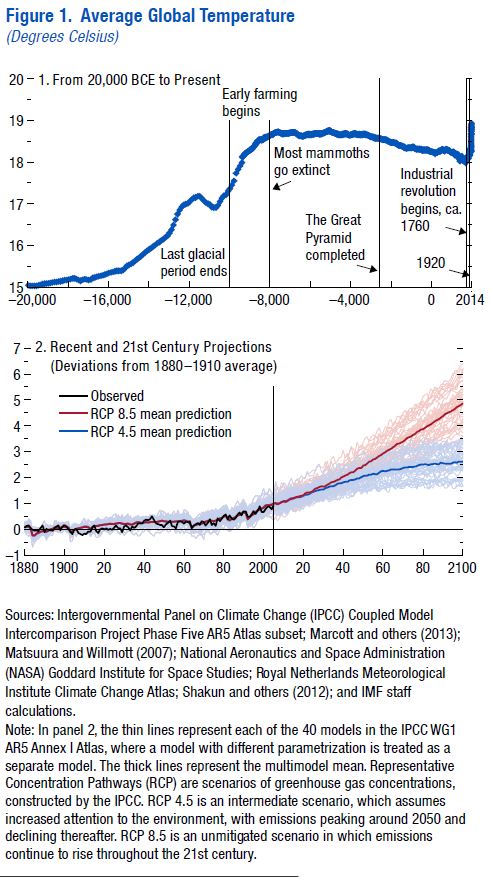

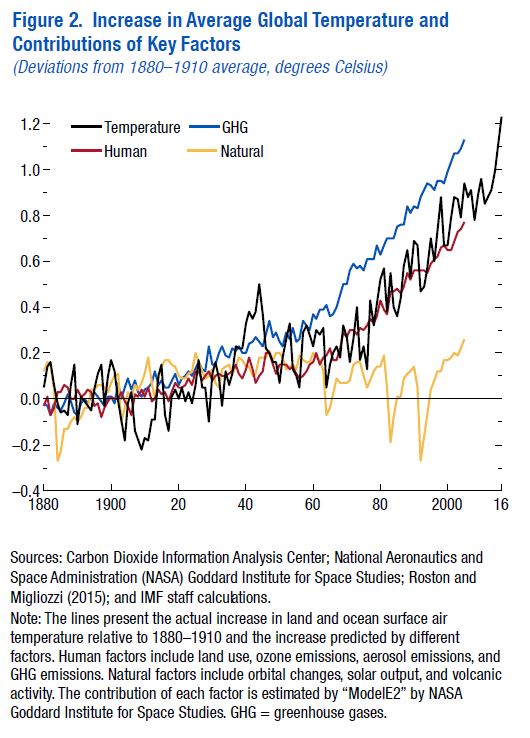

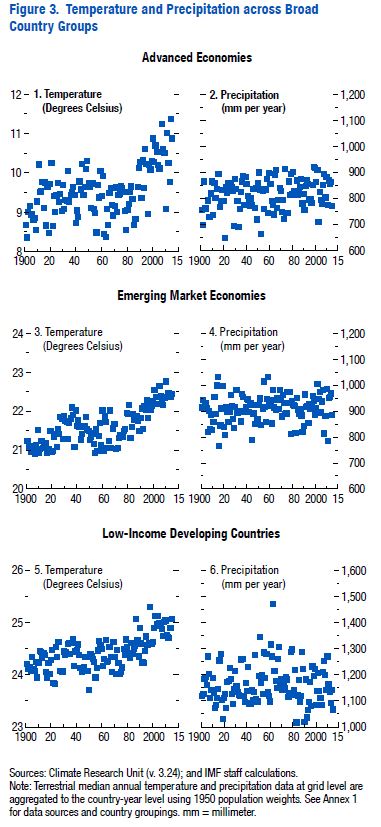

“Global temperatures have increased at an unprecedented pace in the past 40 years. This paper finds that increases in temperature have uneven macroeconomic effects, with adverse consequences concentrated in countries with hot climates, such as most low-income countries. In these countries, a rise in temperature lowers per capita output, in both the short and medium term, through a wide array of channels: reduced agricultural output, suppressed productivity of workers exposed to heat, slower investment, and poorer health. In an unmitigated climate change scenario, and under very conservative assumptions, model simulations suggest the projected rise in temperature would imply a loss of around 9 percent of output for a representative low-income country by 2100.”

From a new IMF working paper:

“Global temperatures have increased at an unprecedented pace in the past 40 years. This paper finds that increases in temperature have uneven macroeconomic effects, with adverse consequences concentrated in countries with hot climates, such as most low-income countries. In these countries, a rise in temperature lowers per capita output, in both the short and medium term, through a wide array of channels: reduced agricultural output,

Posted by at 6:02 PM

Labels: Energy & Climate Change

Housing View – June 22, 2018

Journal of Housing Economics (June 2018 Volume)

- Race and the City by Ingrid Gould Ellen, Stephen L. Ross

- Are inclusionary housing programs color-blind? The case of Montgomery County MPDU program by Adji Fatou Diagne, Haydar Kurban, Benoit Schmutz

- The Visible Host: Does race guide Airbnb rental rates in San Francisco? by Venoo Kakar, Joel Voelz, Julia Wu, Julisa Franco

- Racial climate and homeownership by Timothy F. Harris, Aaron Yelowitz

- The non-financial costs of violent public disturbances: Emotional responses to the 2011 riots in England by Panka Bencsik

- Are central cities poor and non-white? by Jenny Schuetz, Jeff Larrimore, Ellen A. Merry, Barbara J. Robles, Arturo Gonzalez

- Racial segregation in the United States since the Great Depression: A dynamic segregation approach by Trevor Kollmann, Simone Marsiglio, Sandy Suardi

- The paradox of expanding ghettos and declining racial segregation in large U.S. metropolitan areas, 1970–2010 by Janice Fanning Madden, Matt Ruther

- Does segregation matter for Latinos? by Jorge De la Roca, Ingrid Gould Ellen, Justin Steil

- There’s no place like home: Racial disparities in household formation in the 2000s by Sandra Newman, Scott Holupka, Stephen L. Ross

On cross-country:

- The unaffordable city: Housing and transit in North American cities – Cities

- Rethinking Urban Sprawl: Moving Towards Sustainable Cities – OECD

- Innovando la política de vivienda a través del alquiler: de la ‘casa propia’ a una vivienda que sirva – Inter-American Development Bank

- How cities can lead the way in bridging the global housing gap – World Economic Forum

- Real Estate & Aging – UBS

On the US:

- Housing Wealth Effects: The Long View – NBER

- Don’t Blame Expensive Housing for Falling Fertility – Citylab

- The 0.25% Fed Rate Increase Doesn’t Mean Mortgage Rates Will Increase 0.25% – Forbes

- Climate Change May Already Be Hitting the Housing Market – Bloomberg

- Zillow Data Used To Project Impact Of Sea Level Rise On Real Estate – NPR

- The High Cost of Low Credit – Zillow

- Negative Equity Dips Below 10 Percent for First Time Since the Bottom of the Market – Zillow

- Birth Rates are Falling Most where Homes are Appreciating Fastest – Zillow

- Californians Are Leaving, Where Are They Looking to Go? – Trulia

- Housing: The Case for YIMBY (Yes, In My Back Yard!) – Foundation for Economic Education

- Threading the Needle of Fair Housing Law in a Gentrifying City with a Legacy of Discrimination – University of San Francisco

- S. Home Prices at Least Affordable Level Since Q3 2008 – ATTOM

On other countries:

- [China] China’s Home Prices Rise at Faster Pace Despite Curbs – Bloomberg

- [Ireland] Surging Irish Home Prices to Cool Off, Central Bank Chief Says – Bloomberg

- [Netherlands] Sizzling Amsterdam Housing Market Pushes People to Other Cities – Bloomberg

- [Spain] New Build Residential Snapshot – Q1 2018 – Knight Frank

- [United Arab Emirates] Dubai / Abu Dhabi Residential Property Price Indices: May 2018 Results – REIDIN

Photo by Aliis Sinisalu

Journal of Housing Economics (June 2018 Volume)

- Race and the City by Ingrid Gould Ellen, Stephen L. Ross

- Are inclusionary housing programs color-blind? The case of Montgomery County MPDU program by Adji Fatou Diagne, Haydar Kurban, Benoit Schmutz

- The Visible Host: Does race guide Airbnb rental rates in San Francisco? by Venoo Kakar, Joel Voelz, Julia Wu, Julisa Franco

- Racial climate and homeownership by Timothy F.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, June 21, 2018

Housing Market in Denmark

The IMF’s latest report on Denmark says that:

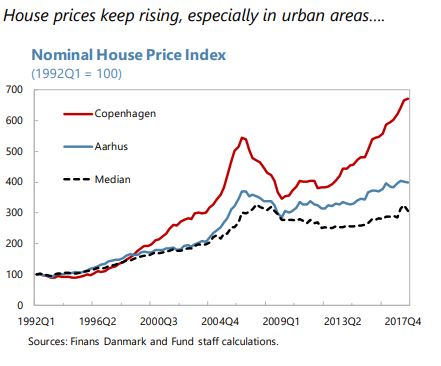

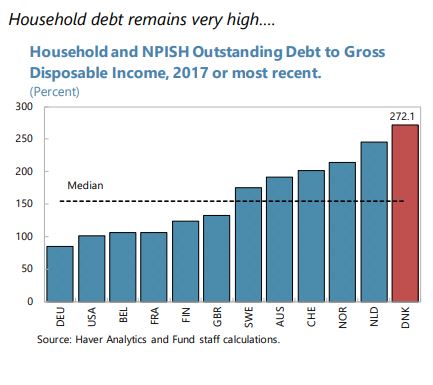

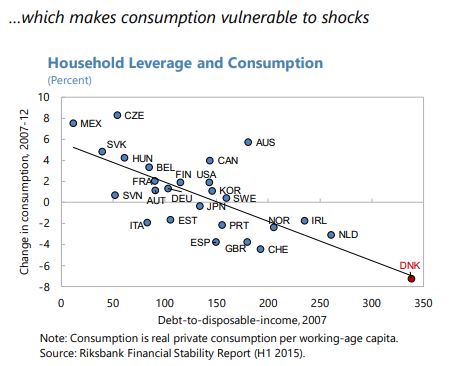

“The adverse feedback loops between housing and the real economy in Denmark are important. The centrality of housing in the Danish economy reflects at least three aspects. First, housing is a major asset of Danish households, together with pensions. Second, MCIs issue covered bonds to fund the mortgages provided to households, transferring part of mortgage risks to investors, mainly financial institutions, including pension funds and insurance companies (Figure 4). Third, because of the high real estate valuations and low interest rates, house purchases typically need to be funded via large mortgage multiples relative to disposable income. These factors help to explain why Danish households’ debt to income ratios are among the highest among advanced economies, and why consumption is sensitive to house price developments.

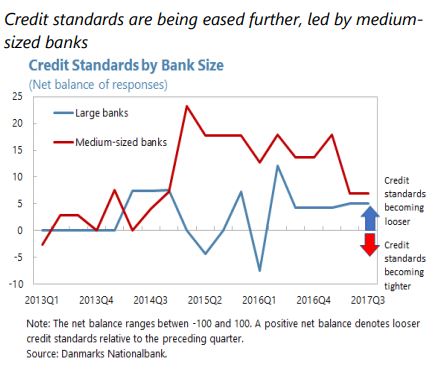

High household leverage combined with high and rising house prices could raise macrofinancial vulnerabilities. There is a risk that high and still rising house prices (particularly in urban areas), the relaxation of credit standards (Figure 4), and mortgage rates near all time-lows, may increase the perception of affordability across a broad spectrum of income levels. In this environment, two types of Danish households are particularly vulnerable to shocks. First, low-income households who spend more than 40 percent of their disposable income on housing (Figure 4). Second, households who have purchased in highly appreciating and potentially overvalued urban areas such as Copenhagen (Selected Issues), where LTI ratios and credit growth are noticeably higher than in the rest of the country. These vulnerabilities are compounded by the large proportion of variable-rate and interest-only mortgages in the system.

In recent years, authorities have implemented an extensive package of policies to address rising vulnerabilities. These include diverse macroprudential policies, 10 various supervisory guidance for MCIs and banks, and a reform of property taxation (Denmark 2017 Article IV report). The authorities continued building their macroprudential toolbox. Following the March 2017 Systemic Risk Council’s recommendation to limit lending via interest-only and floating-rate mortgages to high DTI households in areas with rapid housing prices growth, authorities introduced LTV restrictions. Effective from 2018, changes to consumer protection rules limit lending via interest-only and floating-rate mortgages to highly indebted households. Specifically, there are lending restrictions for households with DTI greater than 4 times and LTV greater than 60 percent: (i) the interest-rate fixation of floating-rate mortgages needs to be at least 5 years, and (ii) deferred amortization is only applicable on 30-year fixed-rate loans.

Coordinated policies are needed to tackle macro-financial vulnerabilities, including those stemming from excessive household leverage combined with rising house prices and affordability. Staff recognized authorities’ efforts and advocated continuing with the deployment of policies as follows.

Macroprudential instruments. The existing macroprudential measures should be tightened further. Staff analysis suggests that the LTV limit should be lowered from 95 to 90 percent to better protect households from house price declines. This decrease would lower aggregate consumption by about 1.5 percentage points one year after introduction, but increase it by 0.2 percentage points in a new steady-state because of lower debt-servicing costs (Denmark 2016 Article IV, Selected Issues). Thus, tightening the LTV limit would have a positive spillover by alleviating demand pressures in the near-term. DTI restrictions should be strengthened for all loans irrespective of LTV considerations. Tighter DTI limits for interest-only and adjustable-rate mortgages should also be considered to contain leverage, increase resilience, and limit the drag on consumption. Highly leveraged households—with debt-to-income above 400 percent—should be subject to mandatory amortization.11 To encourage further reduction of interest-rate sensitivity, the DTI limit could be calibrated to account for lower risk if financing is via fixed–rate mortgages.

Tax policy. Mortgage interest deductibility (MID) should be reduced further than currently planned, as MID distorts investment incentives and incentivizes leverage (Gruber, 2017). During the transition period to a lower mortgage deductibility regime, the current low rate environment would mitigate the adverse impact on homeowners. Also, fiscal savings from this measure could be used to reduce labor tax burden.

Housing supply. Restrictions on the size of new apartments should be relaxed in urban areas where demand-supply imbalances appear to have been a factor pushing valuations higher.

Simpler and more streamlined zoning and planning processes would allow housing supply to respond to increases in demand without steep price increases. Rent controls are among the highest in the EU and should be reduced to incentivize the rental market and alleviate demand for housing. Below-market rents limit the incentive to supply rental units, and incentivize the purchase of housing, adding upward pressure to property prices. Upgrading public and transport infrastructure—especially around inner-city areas experiencing strong house price growth—would help mitigate house prices pressures.The interaction between high household leverage and rising house prices poses macrofinancial risks. Authorities indicated that household resilience to interest rate increases likely improved as more homeowners had shifted towards fixed rate mortgages and longer fixing periods. But if risks continue to build up, the DN sees scope for tighter LTV limit, higher countercyclical capital buffer, amortization requirements and reduction of variable-rate loans. The government argued that additional measures would require further analysis of the effects on the housing market and the overall economy. The government considers unlikely that mortgage interest deductibility will be reduced beyond the planned gradual decline ending next year, and noted that mortgage interest deductibility should take into account balances towards other capital taxation rates.”

The IMF’s latest report on Denmark says that:

“The adverse feedback loops between housing and the real economy in Denmark are important. The centrality of housing in the Danish economy reflects at least three aspects. First, housing is a major asset of Danish households, together with pensions. Second, MCIs issue covered bonds to fund the mortgages provided to households, transferring part of mortgage risks to investors, mainly financial institutions, including pension funds and insurance companies (Figure 4).

Posted by at 11:23 AM

Labels: Global Housing Watch

Subscribe to: Posts