Thursday, July 5, 2018

New Zealand: Managing Housing Market Imbalances

The IMF’s latest report on New Zealand says that:

“Context

The new government’s housing policy agenda focuses on direct supply initiatives, tax

policy changes, and restrictions on home ownership by nonresidents. Addressing declining

housing affordability has become a policy priority (…).

- Supply initiatives. Under the KiwiBuild program, the government plans to build 100,000 affordable houses over 10 years (about one third of average annual residential building authorizations) for first-time homebuyers. After initial financing of NZ$2 billion, the program would be sustained through the sales of completed houses.

- Addressing other supply constraints. Besides the KiwiBuild program, the Urban Growth

Agenda aims to increase the availability of developable land and the supply response to higher house prices by addressing regulatory, planning and other policy constraints, including the underfunding of locally-provided infrastructure.

- Tax policy changes. To dampen property speculation, more residential property sales will be subject to capital gains taxes, as the related bright-line test has been extended from a two-year to a five-year holding period. Residential properties other than main home acquired after March 29, 2018 will be subject to capital gain taxes if disposed of within five years of acquisition. The government also proposed to limit negative gearing from rental properties, such that the deductibility of net losses from property investment (and interest costs) from other taxable income would be eliminated. A Tax Working Group is considering possible additional reform, including a broader capital gains tax on real estate investment and land tax reform.

- Restrictions on nonresidents’ real estate purchases. A proposed ban in a draft amendment to the Overseas Investment Act is scheduled for a parliamentary vote as early as late June 2018. Under the amendment, all residential land would be re-classified as “sensitive land,” which would require approval for foreign buyers under tighter qualifying criteria.

Staff’s Views

The housing policy agenda appropriately focuses on closing key gaps on the supply

side and in the tax system. While demand-side drivers have stabilized, they remain robust, and improved housing affordability ultimately requires a stronger housing supply response. These measures are complementary, and the success of the housing policy agenda will depend on well coordinated progress on all fronts. While the large scale of the KiwiBuild program can provide the certainty needed to redirect builders’ incentives toward lower-price housing and adopt new, more cost-effective building technology, the direct market intervention by the government also comes with risks to the budget and risks of crowding out private housing supply and market distortions more broadly. The Tax Working Group should also consider raising land taxes, which are efficient and would increase the recurrent cost of holding land, thereby encouraging its (re)development.A ban of residential real estate purchases by nonresidents is unlikely to improve housing affordability significantly. The proposed draft amendment to the Overseas Investment Act would be a capital flow management measure (CFM) under the IMF’s Institutional View (IV) on capital flows, as it would introduce discrimination based on residency and thus limit capital flows by its design. Its use would not be in line with the IV. While macroeconomic and macroprudential policy settings are broadly appropriate, available data suggest that foreign buyers appear to have played a minor role in New Zealand’s residential real estate markets recently. And in its current design, the CFM is unlikely to be temporary or targeted. The broad housing policy agenda above, if fully implemented, would address most of the potential problems associated with foreign buyers on a non-discriminatory basis.

Authorities’ Views

The authorities concurred that restoring housing affordability required a focus on

strengthening supply and lowering tax distortions. They noted that measures to intensify

competition in land markets via the Urban Growth Agenda would not be sufficient. Direct

intervention, through the KiwiBuild program, was also required. On tax policy, while the extension of the bright-line test to five years for capital gains taxation on non-primary residences is now in place, a wider set of reforms are being considered to the tax treatment of residential real estate investment. This includes ring-fencing negative gearing on investment properties. The Tax Working Group has been directed to consider whether a system of taxing capital gains or land (not applying to the family home or the land under it), or other housing tax measures, would improve the tax system.The authorities disagreed with the assessment that a ban on residential real estate

purchases by nonresidents, if implemented, would be a CFM under the IV. They emphasized

that the ban must be assessed holistically, taking into account the broader social, economic and political context. Declining housing affordability and greater inequality have become a major concern, which has lowered approval of globalization and immigration in New Zealand. Given the central role that home ownership plays in New Zealanders’ sense of well being, the government has taken steps to ensure that housing prices will be shaped by domestic market forces. If the government had not committed to extend its domestic screening regime for sensitive New Zealand assets to residential land, it would not have been able to secure the public’s support for additional international trade agreements. The authorities noted that the proposed screening regime will allow nonresidents to obtain consent to acquire residential land where they are committed to reside and become tax residents, in New Zealand; where their investment will increase housing supply; or where they will develop the land for other purposes (such as commercial premises). They also think that the new regime will help ensure that foreign direct investment flows into the productive economy rather than unproductive speculation. Finally, the authorities do not consider this measure to be a CFM; it will only have a limited effect on aggregate capital flows or the balance of payments, and it will have no material impact on the broader direction of or the openness of New Zealand’s economy.”

The IMF’s latest report on New Zealand says that:

“Context

The new government’s housing policy agenda focuses on direct supply initiatives, tax

policy changes, and restrictions on home ownership by nonresidents. Addressing declining

housing affordability has become a policy priority (…).

- Supply initiatives. Under the KiwiBuild program, the government plans to build 100,000 affordable houses over 10 years (about one third of average annual residential building authorizations) for first-time homebuyers.

Posted by at 10:48 AM

Labels: Global Housing Watch

Wednesday, July 4, 2018

Housing in the United States

The IMF’s latest report on the United States says that:

“Housing finance and the U.S. housing market have not been reformed comprehensively. To date, no legislative or executive action has been taken to reduce substantially the footprint of Fannie Mae and Freddie Mac (“Enterprises”). However, as conservator, the Federal Housing Finance Agency (FHFA) has required market-based credit risk transfers from the Enterprises to the private sector at an increasing level since 2013. The Enterprises have also jointly developed a common securitization platform and have announced that they will issue a new uniform mortgage backed security starting June 2019. These Enterprise reforms have been accomplished administratively and have not reformed the entire housing finance system, which would require legislative action.

Since 2015, the FHFA has directed the Enterprises to fund the Housing Trust Fund and Capital Magnet Funds (as required by the 2008 Housing and Economic Recovery Act) by transferring a portion of total new acquisitions to these funds, which are administered by the Department of Housing and Urban Development and Treasury Department, respectively.

FHFA has the discretion to suspend the Enterprise allocations to the affordable housing funds, including the Housing Trust Fund, if the allocations are contributing to the Enterprise’s financial instability. Moreover, the Senior Preferred Stock Purchase Agreements (PSPA’s) are sources of strength for the Enterprises. Indeed, the PSPA’s between the Treasury and each Enterprise both ensure the ability of each Enterprise to meet its financial obligations and to ensure that they will have minimal net worth as all profits above the capital reserve amount are transferred to Treasury each quarter. The capital reserve amount had been declining by $600 million per year and was scheduled to decline to $0 on January 1, 2018. However, on December 21, 2017, FHFA and the Department of the Treasury agreed to reinstate a $3 billion capital reserve amount for each Enterprise to prevent draws on the PSPA due to fluctuations in the Enterprises’ income due to the normal course of business. Despite the new capital reserve, the December 2017 tax cuts caused the Enterprises to draw a combined total of $4 billion at the end of that quarter. Policymakers have been evaluating and developing a potential comprehensive overhaul of the mortgage finance system over ten years after the federal government took control of Fannie Mae and Freddie Mac that could shrink or eventually close the two entities and create a system with more private capital. The Congressional Budget Office (CBO) has provided analyses on these issues. One such analysis prepared at the request of the Chairman of the House Committee on Financial Services, analyzed alternatives for attracting more private capital to the secondary mortgage market and alternative structures for that market, including a fully federal agency, a hybrid, public-private market, a market with a government guarantor of last resort, and a largely private secondary market.In 2018, the U.S. Senate passed The Economic Grown, Regulatory Relief and Consumer Protection Act (S. 2155), which has emphasized providing regulatory relief for small banks and credit unions and amending the Dodd-Frank Act. Moreover, on June 12, 2017, the Department of the Treasury published a comprehensive report containing recommendations for the financial regulation of banks and credit unions (“A Financial System that Creates Economic Opportunities: Banks and Credit Unions”).”

The IMF’s latest report on the United States says that:

“Housing finance and the U.S. housing market have not been reformed comprehensively. To date, no legislative or executive action has been taken to reduce substantially the footprint of Fannie Mae and Freddie Mac (“Enterprises”). However, as conservator, the Federal Housing Finance Agency (FHFA) has required market-based credit risk transfers from the Enterprises to the private sector at an increasing level since 2013.

Posted by at 2:11 PM

Labels: Global Housing Watch

Housing Affordability in New Zealand and Policy Response

The IMF’s latest report on New Zealand says that:

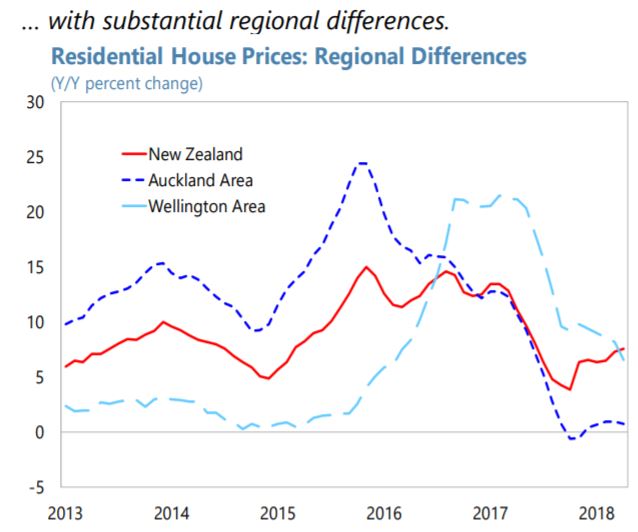

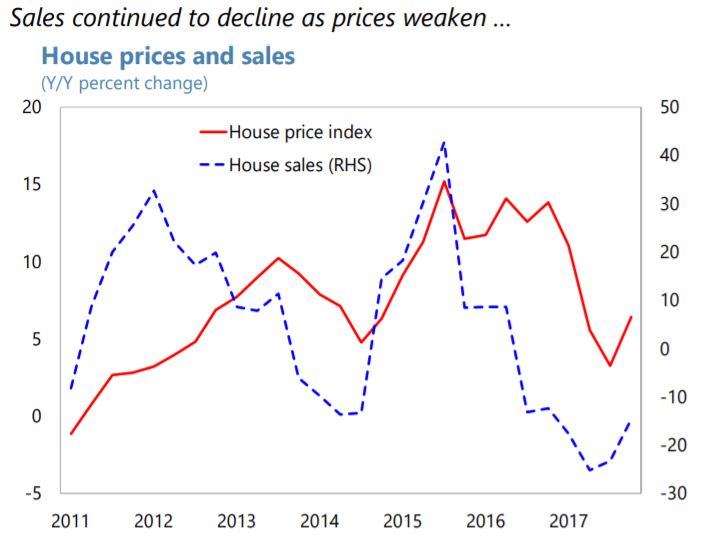

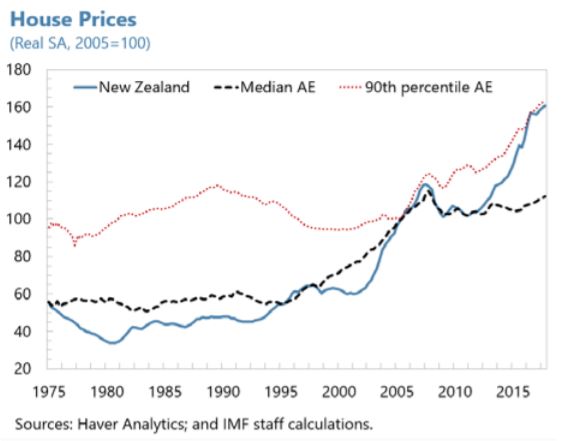

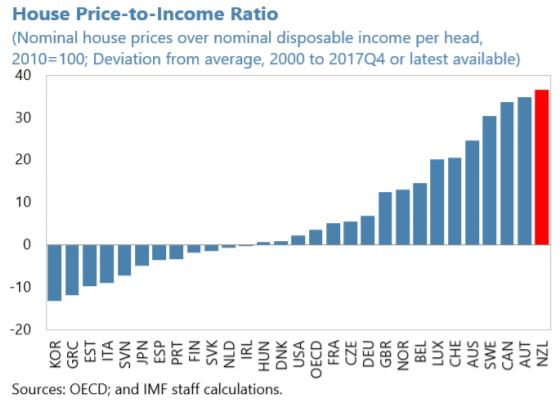

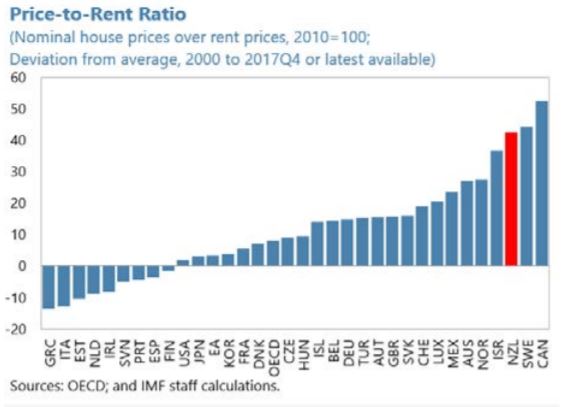

“The housing market is cooling but managing housing-related risks remain challenging.

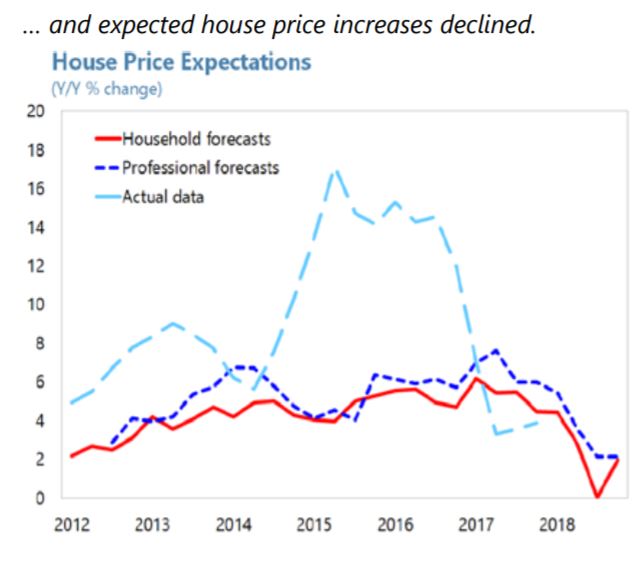

Rising house prices were associated with rapid household credit growth through 2016. Given the slower rise in income, house price-to-income ratios reached unprecedented levels, especially in Auckland where the surge in house prices has been stronger. Household credit growth has moderated in 2017 while household debt continued to rise from already high levels. Given the underlying shortages in housing supply, the moderation in house prices is expected to be slow.Affordability concerns have also become more pressing, especially for first-time home

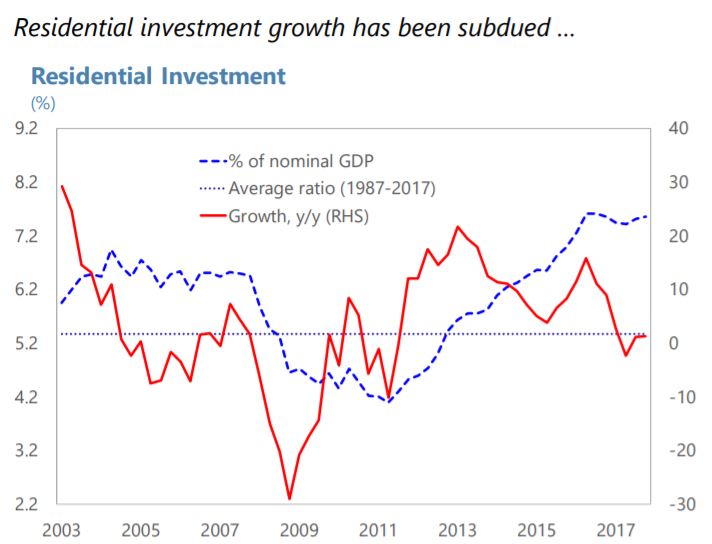

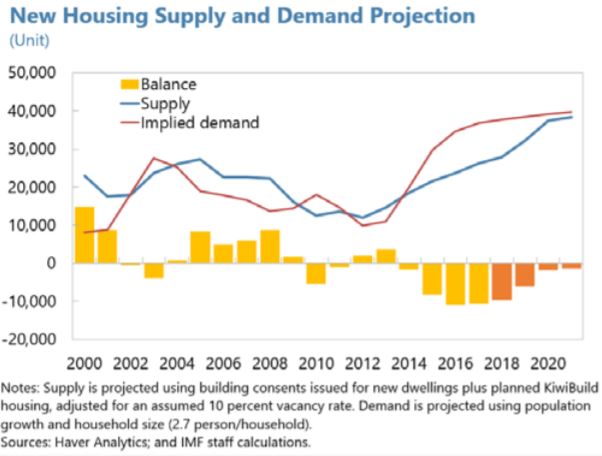

buyers. The deterioration in housing affordability because of high house prices as measured by housing cost to income has been partially offset by lower interest rates. Lower income groups remain more adversely affected by declining housing affordability. Rising house prices pose increasing difficulties for first-time home buyers entering the home market as it increases the length of time needed to save for a mortgage down payment regardless of the level of interest rates, and lead to higher debt servicing requirements as they need to have a larger mortgage than in the past.The housing policy agenda is ambitious and appropriately focuses on closing key gaps

on the supply side and in the tax system. Housing supply shortfalls have contributed to the runup in house prices, reflecting supply constraints amid strong demand fundamentals, including rising net migration, lower interest rates, and stronger income growth. While demand-side drivers have stabilized, they remain robust, and improved housing affordability requires eliminating supply bottlenecks. Supply and demand sides reforms are complementary, and the success of the housing policy agenda will depend on well-coordinated progress on all fronts.Lastly, improving the availability of housing affordability and other related statistical data is important. Further effort to compile and regularly release key housing related indicators such as house prices, housing costs, housing ownership and affordability measures would help to

enhance analysis and inform policy decisions.”

The IMF’s latest report on New Zealand says that:

“The housing market is cooling but managing housing-related risks remain challenging.

Rising house prices were associated with rapid household credit growth through 2016. Given the slower rise in income, house price-to-income ratios reached unprecedented levels, especially in Auckland where the surge in house prices has been stronger. Household credit growth has moderated in 2017 while household debt continued to rise from already high levels.

Posted by at 1:33 PM

Labels: Global Housing Watch

Worries about the yield curve

From a new Econbrowser post by James Hamilton:

“Why does a low or negative spread predict future economic weakness? One factor may be the Fed’s tightening cycle. Historically the inflation rate would at times start climbing above where the Fed wanted it. The Fed responded by raising the short-term rate, the traditional instrument of monetary policy. The market response of long-term rates to the higher short rates was significantly more muted. The result is that the yield spread narrowed as the tightening cycle continued. The Fed often found itself behind the curve, and the last short-term rate hikes were likely a contributing factor to some historical economic recessions.

But we’re still very early in the current tightening cycle. The 3-month Treasury bill has not gone up so far by nearly as much as it did in previous complete cycles, and inflation is still very moderate. So I don’t think it’s time to run for cover just yet. However, if the Fed were to raise the short rate by another 100 basis points without any move up in long rates, we would be into inverted territory, and I would be very concerned. Not a danger sign yet, but definitely an indicator to keep watching.”

From a new Econbrowser post by James Hamilton:

“Why does a low or negative spread predict future economic weakness? One factor may be the Fed’s tightening cycle. Historically the inflation rate would at times start climbing above where the Fed wanted it. The Fed responded by raising the short-term rate, the traditional instrument of monetary policy. The market response of long-term rates to the higher short rates was significantly more muted.

Posted by at 10:37 AM

Labels: Forecasting Forum

Tuesday, July 3, 2018

Revamping inflation targeting in New Zealand 30 years after its inception

A new IMF country report reviews the backdrop to the revamping of the inflation targeting framework in New Zealand. It says that “The Phase One of the Review of the Reserve Bank Act can be regarded as a next step in the gradual evolution of inflation targeting in New Zealand. The new PTA, with its qualitative description of the employment objective, can be regarded as a refinement in the current practice of inflation targeting. The flexible inflation targeting regime was successful in terms of stabilizing output and inflation while maintaining price stability. Recent episodes of inflation undershooting the target serve as an example of uncertainty on the real-time assessment of slack in the economy. The explicit dual mandate will require some changes in the communication of the central bank, including on maximum sustainable employment.”

A new IMF country report reviews the backdrop to the revamping of the inflation targeting framework in New Zealand. It says that “The Phase One of the Review of the Reserve Bank Act can be regarded as a next step in the gradual evolution of inflation targeting in New Zealand. The new PTA, with its qualitative description of the employment objective, can be regarded as a refinement in the current practice of inflation targeting.

Posted by at 7:38 PM

Labels: Inclusive Growth

Subscribe to: Posts