Thursday, July 26, 2018

House Prices in Peru

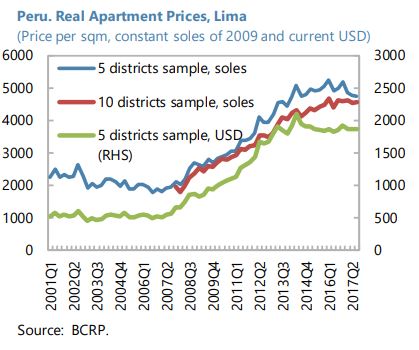

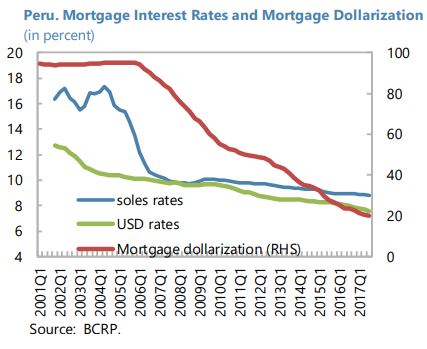

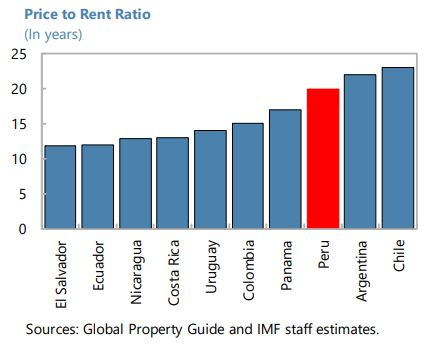

The IMF’s latest report on Peru says that:

“Housing prices have stabilized and cross-country indicators on balance do not suggest a misalignment, although careful monitoring is warranted. Regional comparators show that Peru’s property market is still in line with the rest of the region. Although indicators of the price-to rent ratio show Peru relatively high in the distribution of Latin American countries, the absolute value of this indicator does not appear excessive. In addition, cross-country indicators of housing prices place Peru in the bottom-half of the price distribution of a broader sample of countries. Nevertheless, property price indices in Peru only reflect the capital, Lima.”

The IMF’s latest report on Peru says that:

“Housing prices have stabilized and cross-country indicators on balance do not suggest a misalignment, although careful monitoring is warranted. Regional comparators show that Peru’s property market is still in line with the rest of the region. Although indicators of the price-to rent ratio show Peru relatively high in the distribution of Latin American countries, the absolute value of this indicator does not appear excessive.

Posted by at 5:16 PM

Labels: Global Housing Watch

Fundamental Drivers of House Prices in Advanced Economies

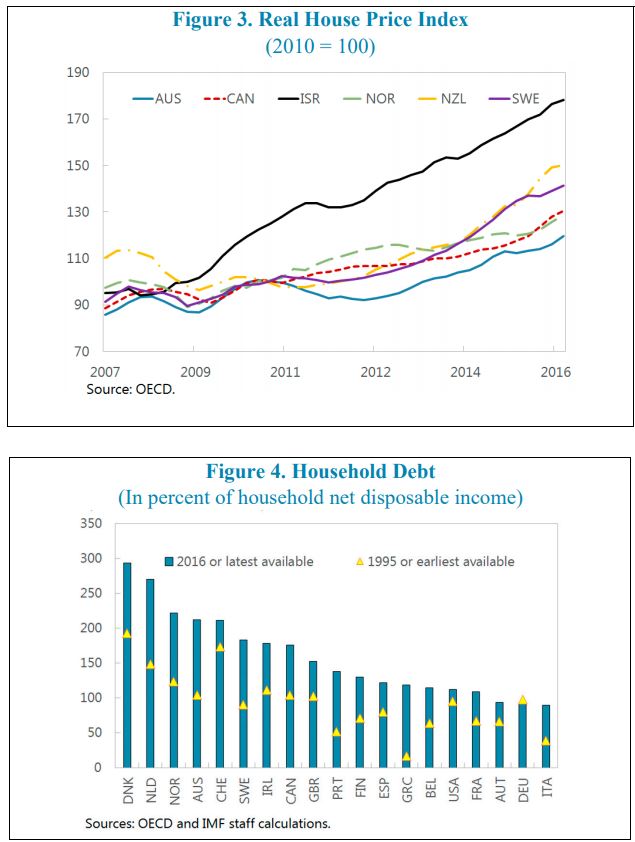

An IMF working paper by Nan Geng says that:

“Assessing the sustainability of house price developments has become an integral part of macro-financial surveillance. Many AEs have experienced a remarkable run-up in their national housing markets in the past two decades and in some cases house prices have remained strong in recent years. Understanding housing price developments and monitoring the extent to which house prices deviate from levels supported by long-run fundamental factors are important for assessing risks to financial and macroeconomic stability.

This paper models house prices on a cross-country basis seeking insights on deviations from sustainable valuations. Based on standard theory, it selects a small set of supply and demand fundamental drivers of house prices to model long-run equilibrium house prices in 20 AEs in the OECD. The novel feature of the model is the incorporation of policy, institutional, and structural factors—i.e. tax incentives for home ownership, rent controls, and the long-run supply responsiveness of housing construction. The estimated long-run relationship broadly captures trends in housing prices since the early 1990s. Hence, the uptrend in real housing prices largely reflects fundamentals, especially rising real disposable incomes. On average, the overvaluation of housing prices on current fundamentals is modest, but there are significant variations in the estimated valuation gaps across our sample.

Policy, institutional, and structural factors are found to be important determinants of long-run equilibrium house prices. The impact of shocks to the traditional demand and supply factors on long-run house prices varies significantly across countries depending on policies and structural factors. In particular, more generous tax relief, stricter rent control, and below-average long-run supply responsiveness are found to drive up house prices.

In this regard, structural reforms in the housing market should be considered alongside macroprudential instruments. Structural reforms can over time improve housing affordability, thereby reducing debt accumulation and enhancing financial stability. These structural reforms include, but are not limited to, reforms to raise the long-run elasticity of housing supply, phasing out rent control, and reducing tax incentives for home ownership and debt financing. Such instruments may complement and support the more commonly used macroprudential tools such as limits on loan-to-value ratios, as the impact of reforms on supply and demand fundamentals may shape longer-term expectations in the housing market.”

An IMF working paper by Nan Geng says that:

“Assessing the sustainability of house price developments has become an integral part of macro-financial surveillance. Many AEs have experienced a remarkable run-up in their national housing markets in the past two decades and in some cases house prices have remained strong in recent years. Understanding housing price developments and monitoring the extent to which house prices deviate from levels supported by long-run fundamental factors are important for assessing risks to financial and macroeconomic stability.

Posted by at 5:09 PM

Labels: Global Housing Watch

Housing in Romania

The latest IMF’s report on Romania says that:

“Real estate exposure rose with housing loans increasing from 21 to 54 percent of household loans between 2008 and 2017. These mortgage contracts (mostly at variable rates) expose banks to credit risks in the event of sharp increases in interest rates. The effectiveness of existing macroprudential tools on mortgages is undermined by the Prima Casa program, which allows loan-to-value ratios up to 95 percent. The Romanian banking system has also a large exposure to their own sovereign debt (one of the highest in the EU at around 20 percent of assets in 2017), that could lead to valuation losses in the event of interest rate increases. Finally, despite declining considerably since 2011, about 35 percent of banks’ liabilities and assets remain denominated in foreign exchange (FX), and FX liquidity risks can exist within an environment of ample overall liquidity.”

The latest IMF’s report on Romania says that:

“Real estate exposure rose with housing loans increasing from 21 to 54 percent of household loans between 2008 and 2017. These mortgage contracts (mostly at variable rates) expose banks to credit risks in the event of sharp increases in interest rates. The effectiveness of existing macroprudential tools on mortgages is undermined by the Prima Casa program, which allows loan-to-value ratios up to 95 percent.

Posted by at 5:03 PM

Labels: Global Housing Watch

Saturday, July 21, 2018

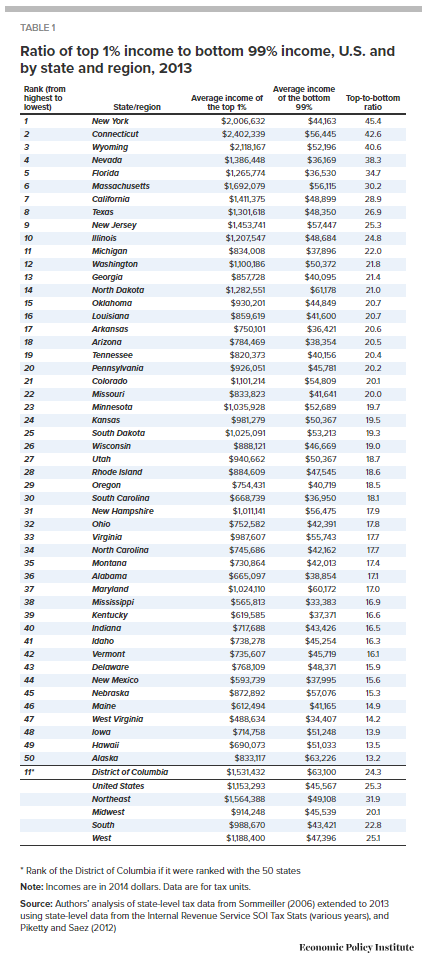

Income inequality in the U.S. by state, metropolitan area, and county

An EIU report finds that “Income inequality has risen in every state since the 1970s and in many states is up in the post–Great Recession era. In 24 states, the top 1 percent captured at least half of all income growth between 2009 and 2013, and in 15 of those states, the top 1 percent captured all income growth. In another 10 states, top 1 percent incomes grew in the double digits, while bottom 99 percent incomes fell. For the United States overall, the top 1 percent captured 85.1 percent of total income growth between 2009 and 2013. In 2013 the top 1 percent of families nationally made 25.3 times as much as the bottom 99 percent.”

An EIU report finds that “Income inequality has risen in every state since the 1970s and in many states is up in the post–Great Recession era. In 24 states, the top 1 percent captured at least half of all income growth between 2009 and 2013, and in 15 of those states, the top 1 percent captured all income growth. In another 10 states, top 1 percent incomes grew in the double digits, while bottom 99 percent incomes fell.

Posted by at 4:40 PM

Labels: Inclusive Growth

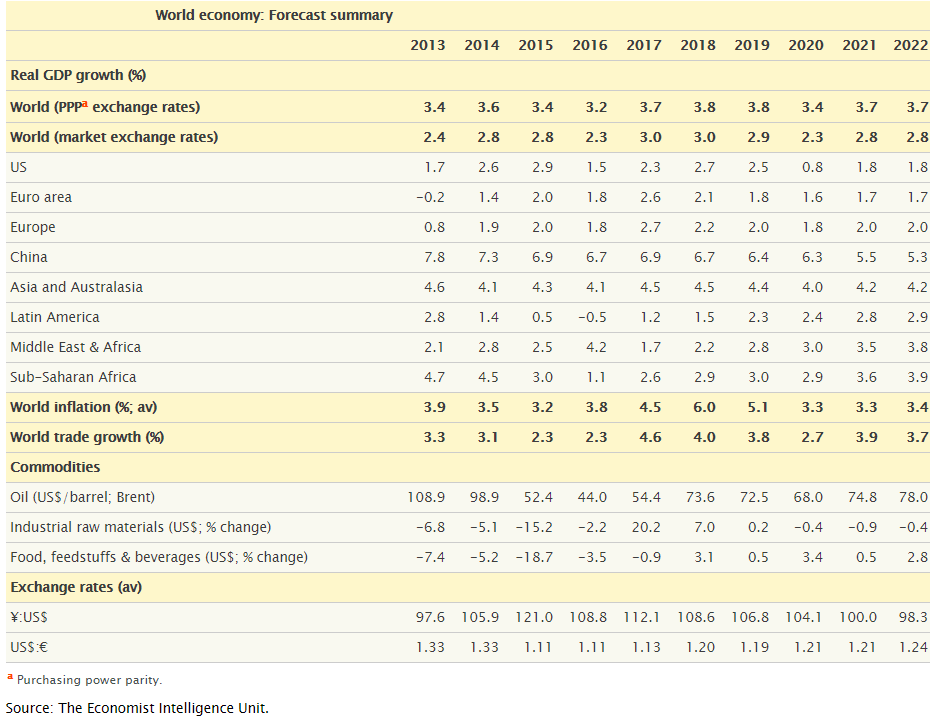

EIU global forecast – Growth will slow in 2019

From the most recent EIU global forecast:

Posted by at 4:36 PM

Labels: Forecasting Forum

Subscribe to: Posts