Thursday, August 9, 2018

The Impact of Higher Temperatures on Economic Growth

From Federal Reserve Bank of Richmond:

“June 2018 was the third-warmest on average across the contiguous forty-eight states since record keeping began in 1895, according to the National Oceanic and Atmospheric Administration (NOAA). Only 1933 and 2016 saw hotter starts to the summer.

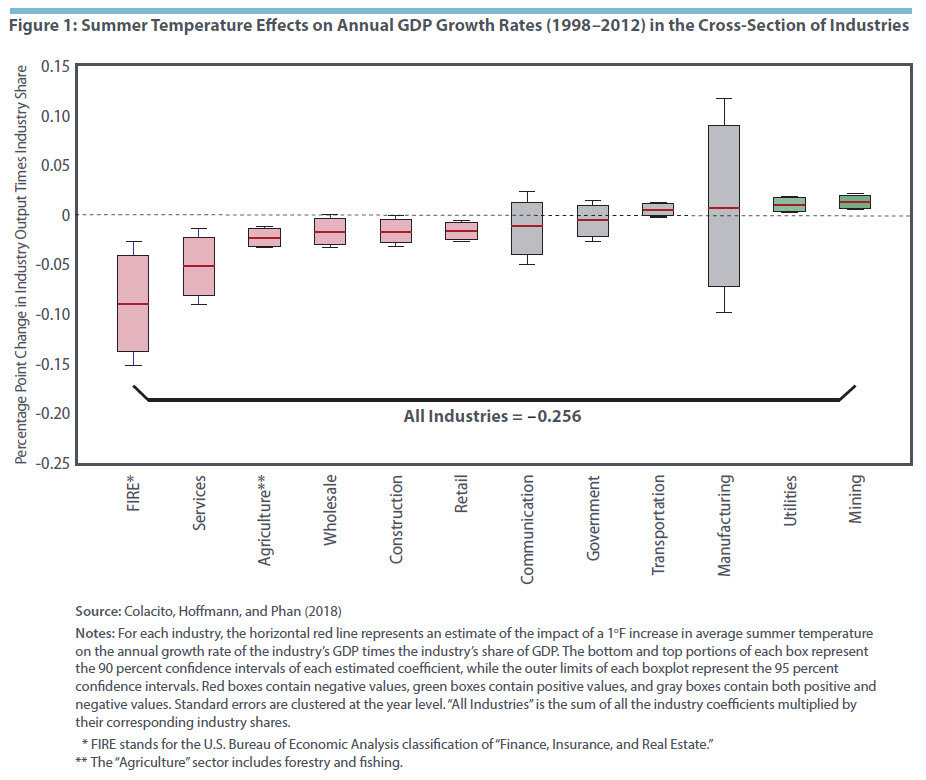

Climate scientists project that average global temperatures will rise over the coming decades, which could have a variety of environmental impacts. But what impact would higher temperatures have on the economy? To date, studies of this question have largely focused on developing countries, under the assumption that those countries are more exposed to the effects of higher temperatures. The economy in developing countries is often more reliant on agriculture or other outdoor activities, and those countries have fewer resources to devote to mitigating the effects of heat through technologies such as air conditioning. Indeed, researchers have found that higher temperatures have significant negative effects on the economic growth of developing nations.1

In the case of developed countries, such as the United States, researchers have focused largely on measuring the impact of warming on outdoor economic activities, such as agriculture.2 Since these sectors make up a relatively small share of the U.S. economy, it has generally been assumed that the economic effects of global warming for the United States would be relatively small. As Nobel prize winning economist Thomas Schelling observed in a 1992 article, “Today very little of our gross domestic product is produced outdoors, susceptible to climate.”3

However, research by three authors of this Economic Brief (Colacito, Hoffmann, and Phan) finds that the consequences of higher temperatures on the U.S. economy may be more widespread than previously thought. By examining changes in temperature by season and across states, they find evidence that rising temperatures could reduce overall growth of U.S. economic output by as much as one-third by 2100.”4

Continue reading here.

From Federal Reserve Bank of Richmond:

“June 2018 was the third-warmest on average across the contiguous forty-eight states since record keeping began in 1895, according to the National Oceanic and Atmospheric Administration (NOAA). Only 1933 and 2016 saw hotter starts to the summer.

Climate scientists project that average global temperatures will rise over the coming decades, which could have a variety of environmental impacts. But what impact would higher temperatures have on the economy?

Posted by at 9:55 AM

Labels: Energy & Climate Change

Saturday, August 4, 2018

Twin Deficits in Developing Economies

A new IMF working paper by Davide Furceri and Aleksandra Zdzienicka provides “new evidence on the existence and magnitude of the “twin deficits” in developing economies. It finds that a one percent of GDP unanticipated increase in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP. This effect is substantially larger than that obtained using standard measures of fiscal impulse, such as the cyclically-adjusted budget balance. The results point to heterogeneity across countries and over time. The effect tends to be larger: (i) during recessions; in countries (ii) that are more open to trade; (iii) that have less flexible exchange rate regimes; and (iv) with lower initial public debt-to-GDP ratios.”

A new IMF working paper by Davide Furceri and Aleksandra Zdzienicka provides “new evidence on the existence and magnitude of the “twin deficits” in developing economies. It finds that a one percent of GDP unanticipated increase in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP. This effect is substantially larger than that obtained using standard measures of fiscal impulse, such as the cyclically-adjusted budget balance.

Posted by at 5:47 PM

Labels: Macro Demystified

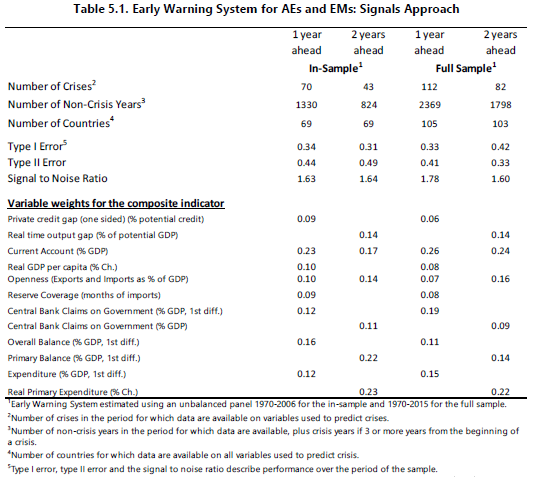

Predicting Fiscal Crises

A new IMF working paper finds that “both nonfiscal (external and internal imbalances) and fiscal variables help predict crises among advanced and emerging economies.”

“Our analysis identifies robust indicators of vulnerabilities that can help signal a high probability of the onset of a crisis in the near future. Building early warning indicators that help predict future fiscal crises is inherently difficult, including because countries may take mitigating action as they see the growing vulnerabilities. However, we find that some types of vulnerabilities are consistently relevant to explain fiscal crises. This raises the question why governments do not act as they see signals. In large measure they do, as crises among advanced economies are rare. Still, the occurrence of crises may reflect overly optimistic projections about the future (e.g., economic growth, cost of debt), and as such governments underestimate the risks and fail to take mitigating measures. Another possibility could be that other shocks or crisis (e.g., banking) could lead to fiscal pressures”

A new IMF working paper finds that “both nonfiscal (external and internal imbalances) and fiscal variables help predict crises among advanced and emerging economies.”

“Our analysis identifies robust indicators of vulnerabilities that can help signal a high probability of the onset of a crisis in the near future. Building early warning indicators that help predict future fiscal crises is inherently difficult, including because countries may take mitigating action as they see the growing vulnerabilities.

Posted by at 5:35 PM

Labels: Forecasting Forum

Friday, August 3, 2018

Housing View – August 3, 2018

On cross-country:

- Housing, Debt and the Economy: a Tale of Two Countries – University of Oxford

- The End of the Global Housing Boom – Bloomberg

- Housing Costs and Regional Income Inequality in China and the U.S. – Federal Reserve Bank of St. Louis

- Charlemagne: the backlash against Airbnb – Economist

- ¿Es posible alquilar en la ciudad sin dejarse el sueldo en ello? – GQ

- Prime price growth drift lower across global cities – Knight Frank

On the US:

- The Scar From Which The Construction Workforce Has Yet To Recover – BuildZoom, Wall Street Journal

- Eyes Wide Shut? The Moral Hazard of Mortgage Insurers during the Housing Boom – NBER

- What is driving America’s housing crisis? A long-read Q&A with Lynn Fisher – American Enterprise Institute

- Fixing Public Housing: A Day Inside a $32 Billion Problem – New York Times

- Blackstone Makes First Bet on Manufactured Housing – Blackstone

- The Urbanist Case for Trailer Parks – CityLab

- The U.S. Housing Market Looks Headed for Its Worst Slowdown in Years – Bloomberg

- A Greater Share of Rentals Are Out of Reach for Blacks, Hispanics – Zillow

- Buying a Home Is Less Affordable Than It’s Been in Almost a Decade – Zillow

- Homeownership Aspirations: The Enduring & Evolving American Dream – Zillow

- Non-Resident Foreigners Sell for Twice Median U.S. Home Value – Zillow

- When Rent Growth Signals Stability, Not Stress – Zillow

- The Real Reasons Millennials Are Struggling to Become Homeowners – Zillow

- Housing’s Headwinds Are Getting Stiffer – Bloomberg

- Nation’s housing market may be headed for biggest slowdown in years – Seattle Times

- As Affordable Housing Crisis Grows, HUD Sits on the Sidelines – New York Times

- MLS Information Sharing Intensity and Housing Market Outcomes – The Journal of Real Estate Finance and Economics

- New York City Sues Airbnb to Force Compliance With Subpoena – Bloomberg

- Best Neighborhoods for Real Estate Buying and Investing – ATTOM

On other countries:

- [Australia] Australia House Prices Fall the Most in 7 Years – Bloomberg

- [Canada] Canada Risks Creating ‘A Permanent Generation Of Middle-Class Renters’: Industry Group – Huffington Post

- [China] China Toughens Housing Policy as Shenzhen Imposes More Curbs – Bloomberg

- [Poland] Disequilibrium in the real estate market: Evidence from Poland – Land Use Policy

Photo by Aliis Sinisalu

On cross-country:

- Housing, Debt and the Economy: a Tale of Two Countries – University of Oxford

- The End of the Global Housing Boom – Bloomberg

- Housing Costs and Regional Income Inequality in China and the U.S. – Federal Reserve Bank of St. Louis

- Charlemagne: the backlash against Airbnb – Economist

- ¿Es posible alquilar en la ciudad sin dejarse el sueldo en ello?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, August 2, 2018

What Are Economists Getting Wrong Today?

A new BloombergQuint post by Simon Kennedy notes my research on forecasting recessions that “Indeed, a 2014 study by Prakash Loungani of the International Monetary Fund found that not one of the 49 recessions suffered around the world in 2009 had been predicted by a consensus of economists a year earlier. Further back, he discovered only two of the 60 recessions of the 1990s were anticipated a year in advance.”

It also summarizes the views of many economists:

“Given our past record in predicting the economic impact of technology, economists will probably get this wrong again. Today, weak productivity growth seems puzzling at a time of great new technological innovations. But in the past, it took decades for electricity or cars or computers to be fully integrated into our production processes and business practices and to boost productivity growth. Likewise, the internet of things or artificial intelligence will take time to be similarly integrated and to be visible in our measures of productivity. While being well aware that, in the 1930s, [John Maynard] Keynes famously predicted that automation would lead to a three-hour working day, my sense is that this process is likely to speed up and surprise on the positive side.”—Peter Praet, Chief Economist at the European Central Bank

A new BloombergQuint post by Simon Kennedy notes my research on forecasting recessions that “Indeed, a 2014 study by Prakash Loungani of the International Monetary Fund found that not one of the 49 recessions suffered around the world in 2009 had been predicted by a consensus of economists a year earlier. Further back, he discovered only two of the 60 recessions of the 1990s were anticipated a year in advance.”

It also summarizes the views of many economists:

“Given our past record in predicting the economic impact of technology,

Posted by at 9:46 PM

Labels: Forecasting Forum

Subscribe to: Posts