Tuesday, August 14, 2018

Inequality in the Middle East

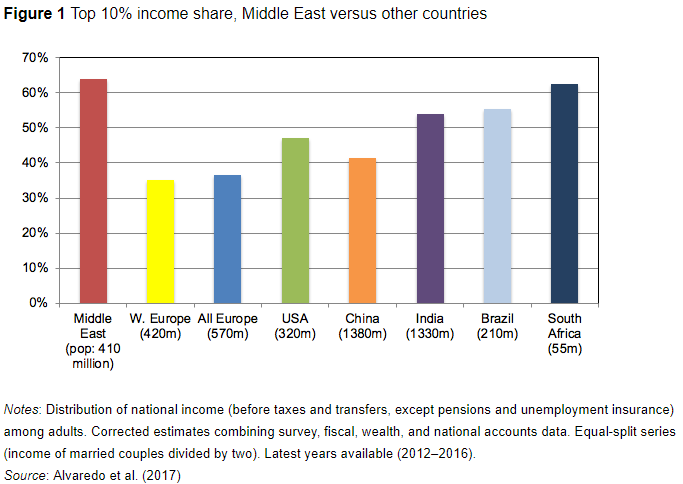

A new VOX post “uses new ‘distributional national accounts’ data to show that the Middle East is in fact the most unequal region in the world, with both enormous inequality between countries and large inequality within countries. The results emphasise the need to develop mechanisms of regional redistribution and to increase transparency on income and wealth data.”

“According to our benchmark estimates, the share of total income accruing to the top 10% of income earners is about 64% in the Middle East, which compares with 37% in Western Europe, 47% in the US, 55% in Brazil, and 62% in South Africa – the two latter countries being often characterised as the most unequal in the world (see Figure 1).”

Continue reading here.

A new VOX post “uses new ‘distributional national accounts’ data to show that the Middle East is in fact the most unequal region in the world, with both enormous inequality between countries and large inequality within countries. The results emphasise the need to develop mechanisms of regional redistribution and to increase transparency on income and wealth data.”

“According to our benchmark estimates, the share of total income accruing to the top 10% of income earners is about 64% in the Middle East,

Posted by at 9:52 AM

Labels: Inclusive Growth

The Global Liveability Index 2018

From the EIU report:

“The results of the Global Liveability Index 2018 reveal that Vienna has displaced Melbourne as the world’s most liveable city. This ends a record seven consecutive years at the head of the survey for the Australian city.

This year’s Index also finds an improvement in the scores of the top-ranked cities, reflecting improvements in safety and stability across most regions. Other key findings include:

- Canadian cities outperform cities in the United States, with three Canadian cities making this year’s top ten

- Manchester, Paris and Copenhagen have seen the biggest ranking improvements among western European cities over the past year

- Osaka and Tokyo have climbed up the ranking to enter to top 10 for the first time”

From the EIU report:

“The results of the Global Liveability Index 2018 reveal that Vienna has displaced Melbourne as the world’s most liveable city. This ends a record seven consecutive years at the head of the survey for the Australian city.

This year’s Index also finds an improvement in the scores of the top-ranked cities, reflecting improvements in safety and stability across most regions. Other key findings include:

- Canadian cities outperform cities in the United States,

Posted by at 9:36 AM

Labels: Global Housing Watch

Friday, August 10, 2018

Per Capita Income, Consumption Patters, and CO2 emission

From a new working paper by Justin Caron and Thibault Fally:

“This paper investigates the role of income-driven differences in consumption patterns in explaining and projecting energy demand and CO2 emissions. We develop and estimate a general-equilibrium model with non-homothetic preferences across a large set of countries and sectors, and trace embodied energy consumption through intermediate use and trade linkages. Consumption of energy goods is less than proportional to income in rich countries, and more income-elastic in low-income countries. While income effects are weaker for embodied energy, we nd a signi cant negative relationship between income elasticity and CO2 intensity across all goods. These income-driven differences in consumption choices can partially explain the observed inverted-U relationship between income and emissions across countries, the so-called environmental Kuznet curve. Relative to standard models with homothetic preferences, simulations suggest that income growth leads to lower emissions in high-income countries and higher emissions in some low-income countries, with only modest reductions in world emissions on aggregate.”

From a new working paper by Justin Caron and Thibault Fally:

“This paper investigates the role of income-driven differences in consumption patterns in explaining and projecting energy demand and CO2 emissions. We develop and estimate a general-equilibrium model with non-homothetic preferences across a large set of countries and sectors, and trace embodied energy consumption through intermediate use and trade linkages. Consumption of energy goods is less than proportional to income in rich countries,

Posted by at 10:49 AM

Labels: Energy & Climate Change

Housing View – August 10, 2018

On cross-country:

- Housing Policy and the Changing Tenure Mix – National Institute of Economic Review

- A Tale of Two Countries: Comparing the US and Chinese Housing Markets – The Journal of Real Estate Finance and Economics

On the US:

- Both renters and homeowners could benefit from better housing policy – Brookings

- Will The Mortgage Market Impact The Midterm Elections? – Forbes

- Pricey Housing Markets in West Are Cooling Off Most Quickly – Wall Street Journal

- America’s Housing Crisis Is Forcing More People To Live In Vehicles – Huffington Post

On other countries:

- [Canada] Housing market dynamics and macroprudential policies – Bank of Canada

- [India] Too slow for the urban march: Litigations and real estate market in Mumbai – Brookings

- [Netherlands] The Big Problem With Investing in Amsterdam’s Hot Housing Market – Bloomberg

- [United Arab Emirates] Dubai Builder Sees Property Slump Lasting for Years – Bloomberg

- [United Kingdom] History dependence in the housing market – Bank of England

Photo by Aliis Sinisalu

On cross-country:

- Housing Policy and the Changing Tenure Mix – National Institute of Economic Review

- A Tale of Two Countries: Comparing the US and Chinese Housing Markets – The Journal of Real Estate Finance and Economics

On the US:

- Both renters and homeowners could benefit from better housing policy – Brookings

- Will The Mortgage Market Impact The Midterm Elections?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, August 9, 2018

Housing Market in Hungary

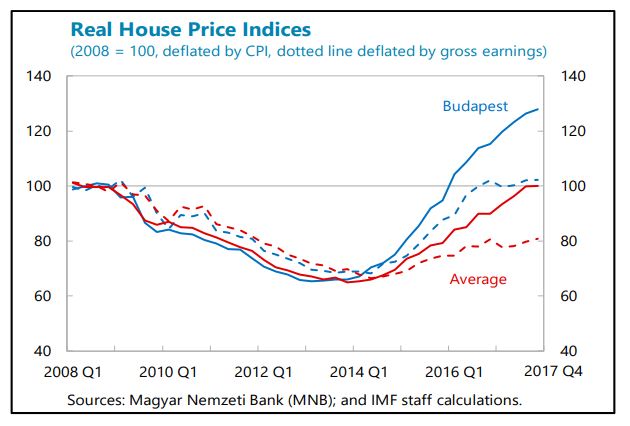

From the IMF’s latest report on Hungary:

“Hungarian housing prices have increased rapidly since 2014, but from a low level. House prices began to increase in the Budapest area, but have spread to other cities and more recently to municipalities. According to the MNB’s and European Systemic Risk Board’s (data for the latter are as of Q3 2017) estimates, average prices are not yet excessively overpriced compared to fundamentals. The number of transactions has begun to stabilize, possibly due to labor shortages and increasing construction costs, which, according to market observers, frequently delay the completion of new dwellings by 6–12 months.

The housing boom has been driven by many factors other than credit. Delayed purchases following the global financial crisis as well as fiscal initiatives have contributed to the boom. For instance, (i) young families committed to have three or more children can receive a grant and a subsidized loan to purchase a home; and (ii) the VAT rate on sales of certain new dwellings has been temporarily reduced from 27 to 5 percent during the 2016–2019 period. Moreover, low interest rates have made real estate investments more attractive. The MNB’s mortgage bond purchase program may have further supported the market. Finally, the MNB-certified consumer friendly housing loans introduced in 2017, has helped level the playing field, lowered borrowing costs, and encouraged fixed-rate lending. The stock of loans for house purchases increased by 6.8 percent (y-o-y) in May 2018. Nevertheless, according to market observers, only about 45 percent of transactions involve borrowings. Moreover, household debt in Hungary remains low compared to peers. It is also almost completely denominated in local currency, but a substantial share remains variable-rate loans.

The MNB has preventatively tightened macroprudential policies, but the booming housing market needs to be closely monitored. The various macroprudential measures seem to be working, as only about 20 percent of new lending have variable-rates or a fixed rate up to one year. Already in 2016, the calculation of the payment-to-income (PTI) ratio was changed to not discourage fixed-rate borrowing. In April 2017, the mortgage funding adequacy ratio (MFAR) was introduced to encourage banks to issue longer mortgage bonds. These ratios will be further refined to discourage interest rate risk for households in October 2018, while there are no plans thus far to change the loan-to-value ratios. However, given the fact that the boom thus far has mostly been driven by strong disposable income and fiscal incentives rather than credit and low interest rates, there is also a need to review these fiscal incentives as well as supply constraints that appear to be contributing to the boom.”

From the IMF’s latest report on Hungary:

“Hungarian housing prices have increased rapidly since 2014, but from a low level. House prices began to increase in the Budapest area, but have spread to other cities and more recently to municipalities. According to the MNB’s and European Systemic Risk Board’s (data for the latter are as of Q3 2017) estimates, average prices are not yet excessively overpriced compared to fundamentals. The number of transactions has begun to stabilize,

Posted by at 10:08 AM

Labels: Global Housing Watch

Subscribe to: Posts