Wednesday, August 22, 2018

Credit Supply and Housing Speculation

From Atif Mian and Amir Sufi at VoxEU:

“Charles P. Kindleberger wrote that “asset price bubbles depend on the growth in credit”. This column looks at the acceleration of the US private label mortgage securitisation market in the US in the late summer of 2003, which disproportionately reduced the cost of financing by lenders that did not traditionally rely on deposit financing for mortgage lending. The sharp rise in lending in zip codes with greater exposure to such lenders generated a boom and bust in house prices. Easier credit also appears to have been a crucial ingredient in explaining bubble cities that experienced both house price and construction booms.

Charles P. Kindleberger, who was the world’s leading expert on financial crises, wrote that “asset price bubbles depend on the growth in credit” (Kindleberger and Aliber 2005). Nobel prize winner Vernon Smith described evidence from experimental settings showing that that the size of a bubble increased when individuals were allowed to borrow (Porter and Smith 1994). Economic theorists have taken this lesson to heart, writing down models in which easier credit helps fuel asset prices through an increase in speculative buying (Allen and Gorton 1993, Allen and Gale 2000).

A core idea in the theory of credit and bubbles is that easier credit allows optimists with high asset valuations to aggressively buy assets, and therefore boost the price (Geanakoplos 2010, Simsek 2013). Even if optimists form a small part of the overall population, easier credit can allow this small group to have a large effect on the market. Further, if the optimists suddenly lose access to credit, the price of the asset will collapse before more pessimistic individuals can be induced to buy the asset. As a result, fluctuations in credit availability increase the amplitude of fluctuations in asset prices.

Our recent study tests this idea, focusing on the boom and bust in house prices from 2000 to 2010 in the US (Mian and Sufi 2018). The study focuses on a natural experiment: the sudden acceleration of the private label mortgage securitisation (PLS) market in the late summer of 2003. The sudden rise in the PLS market, which was part of the broader global rise in shadow banking during this period, disproportionately reduced the cost of financing by lenders that did not traditionally rely on deposit financing for mortgage lending. The study shows that lenders who traditionally relied on non-deposit financing, such as CountryWide and Ameriquest Mortgage Company, suddenly boosted mortgage lending in the late summer of 2003, just as the PLS market accelerated.

To test the effect of this sudden increase in credit availability on the housing market, we exploit variation across geographic areas in the US in the location of these lenders as of 2002. Zip codes where lenders traditionally relied on non-deposit financing witnessed a sudden and large relative increase in mortgage lending just as the PLS market accelerated in 2003. Our study shows several results that suggest this is a clean experiment – the sudden and large expansion of mortgage lending in these zip codes was due to the acceleration of the PLS market, as opposed to some other factor such as a change in income prospects or beliefs about house prices among those living in these zip codes.”

Continue reading here.

From Atif Mian and Amir Sufi at VoxEU:

“Charles P. Kindleberger wrote that “asset price bubbles depend on the growth in credit”. This column looks at the acceleration of the US private label mortgage securitisation market in the US in the late summer of 2003, which disproportionately reduced the cost of financing by lenders that did not traditionally rely on deposit financing for mortgage lending. The sharp rise in lending in zip codes with greater exposure to such lenders generated a boom and bust in house prices.

Posted by at 9:12 AM

Labels: Global Housing Watch

Tuesday, August 21, 2018

Victories Against Air Pollution

From a new post by Timothy Taylor:

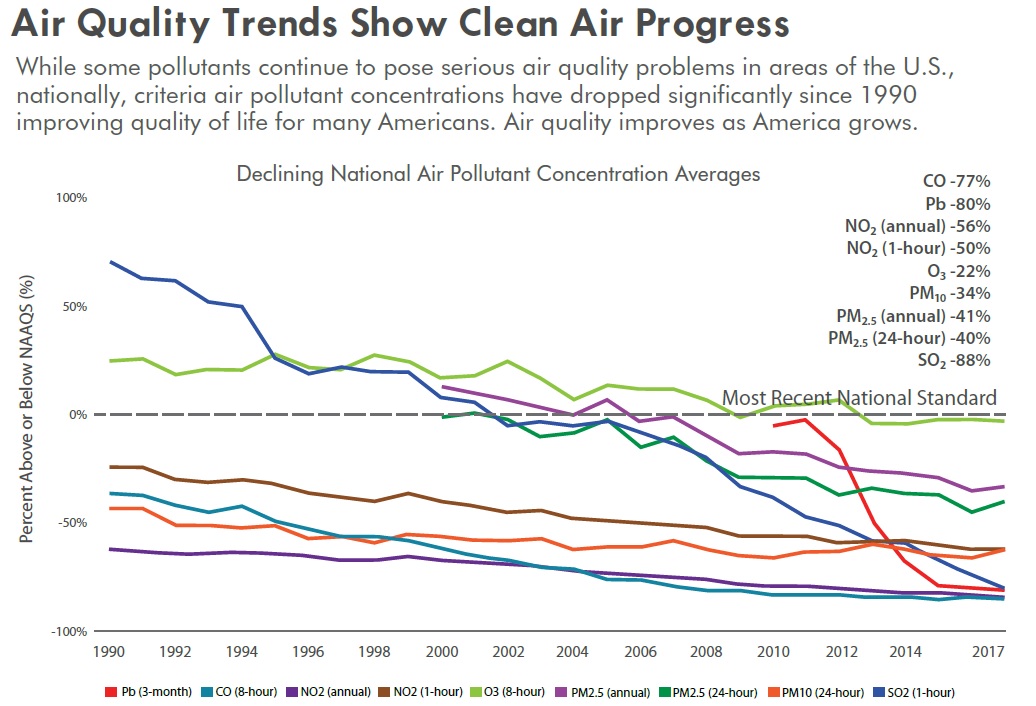

“There is a certain kind of environmentalist who seems unable to acknowledge any good news about the environment, because it might create complacency about remaining issues. I’m not a fan of this approach. When successes are denied, credibility diminishes. And if there’s never been an environmental success to celebrate, I’m more likely to be discouraged about the future than energized. In that spirit, here are some figures from an Environment Protection Agency annual report, Our Nation’s Air.”

“This figure shows the decline in what are often called the “criteria” air pollutants. The horizontal line shows the U.S. National Ambient Air Quality Standards. At a national level, all of the pollutants are below the dashed line. The percentages in the upper right corner of the figure show the decline in the concentration of each category of air pollution since 1990s.”

From a new post by Timothy Taylor:

“There is a certain kind of environmentalist who seems unable to acknowledge any good news about the environment, because it might create complacency about remaining issues. I’m not a fan of this approach. When successes are denied, credibility diminishes. And if there’s never been an environmental success to celebrate, I’m more likely to be discouraged about the future than energized. In that spirit,

Posted by at 5:58 PM

Labels: Energy & Climate Change

Friday, August 17, 2018

Forecasting Failures and the Need for Automatic Stabilizers

From a new post by Chris Dillow:

“Simon has a good discussion on whether fiscal or monetary policy is better at stabilizing output. I’d suggest, though, that neither is in practice particularly good and that what we need instead are stronger automatic stabilizers.

I say so for a simple reason: recessions are unpredictable. Back in 2000 Prakash Loungani studied the record of private sector consensus forecasts for GDP and concluded that “the record of failure to predict recessions is virtually unblemished” – a fact which remained true thereafter.

The ECB, for example, raised rates in 2007 and 2008, oblivious to the impending disaster. The Bank of England did little better. In February 2008, its “fan chart” attached only a slight probability to GDP failing in year-on-year terms at any time in 2008 or 2009 when in fact it fell 6.1% in the following 12 months. Because of this, it didn’t cut Bank Rate to 0.5% until March 2009.

Given that it takes around two years for changes in interest rates to have its maximum effect upon output, this means that monetary policy does a better job of repairing the economy after a recession than it does of preventing recession in the first place. And of course, as there’s no evidence that governments can predict recessions any better than the private sector or central banks, the same is true for fiscal policy.

All this suggests to me that if we want to stabilize in the face of unpredictable recessions, we need not just discretionary monetary or fiscal policy but rather better automatic stabilizers.”

From a new post by Chris Dillow:

“Simon has a good discussion on whether fiscal or monetary policy is better at stabilizing output. I’d suggest, though, that neither is in practice particularly good and that what we need instead are stronger automatic stabilizers.

I say so for a simple reason: recessions are unpredictable. Back in 2000 Prakash Loungani studied the record of private sector consensus forecasts for GDP and concluded that “the record of failure to predict recessions is virtually unblemished”

Posted by at 10:10 AM

Labels: Forecasting Forum

Employment Protection Deregulation and Labor Shares in Advanced Economies

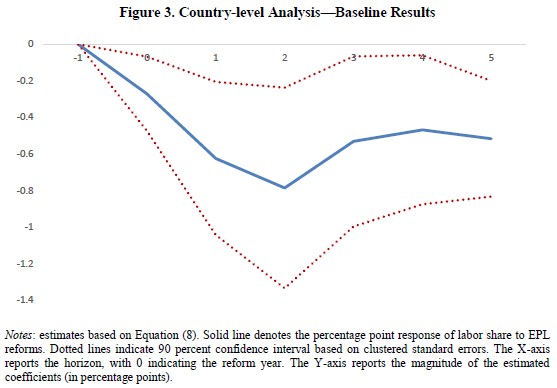

A new IMF working paper by Gabriele Ciminelli, Romain Duval, and Davide Furceri investigates “the impact of job protection deregulation in a sample of 26 advanced economies over the period 1970-2015, using a newly constructed dataset of major reforms to employment protection legislation for regular contracts” and finds “a statistically significant, economically large and robust negative effect of deregulation on the labor share. In particular, illustrative back-of-the-envelope calculations suggest that job protection deregulation may have contributed about 15 percent to the average labor share decline in advanced economies. Together with existing evidence regarding the macroeconomic gains from job protection and other labor market reforms, [these] results also point to the need for policymakers to address efficiency-equity trade-offs when designing such reforms.”

A new IMF working paper by Gabriele Ciminelli, Romain Duval, and Davide Furceri investigates “the impact of job protection deregulation in a sample of 26 advanced economies over the period 1970-2015, using a newly constructed dataset of major reforms to employment protection legislation for regular contracts” and finds “a statistically significant, economically large and robust negative effect of deregulation on the labor share. In particular, illustrative back-of-the-envelope calculations suggest that job protection deregulation may have contributed about 15 percent to the average labor share decline in advanced economies.

Posted by at 10:02 AM

Labels: Inclusive Growth

Housing View – August 17, 2018

On cross-country:

- Our cities house-price index suggests the property market is slowing – Economist

- Global House Price Index – Economist

- Planning rules are driving the global housing crisis – Financial Times

- Opinion today: Demented by the housing crisis: Simply comparing the number of households to dwellings gives a foolishly misleading idea – Financial Times

On the US:

- Our Shrinking Supply of Low-Cost Rental Units – Joint Center for Housing Studies

- Who Owns a Home in America, in 12 Charts – Citylab

- Does Homeownership Influence Political Behavior? Evidence from Administrative Data – Stanford University

- The effects of housing supply restrictions on partisan geography – Political Geography

- Redfin doubling down on direct home buying, plans expansion of Redfin Now – HousingWire

- Housing market has hit a ‘significant slowdown’ in recent weeks, Redfin CEO says – MarketWatch

- New housing construction doesn’t fuel SF evictions, claims report – Curbed

- Hosing Homebuyers: Why Cities Should Not Pay For Water and Wastewater Infrastructure with Development Charges – D. Howe Institute

- Seattle’s Socialist City Council Member Thinks Housing Is a Human Right—Unless it Comes at the Expense of Music Venues – Reason

- Highest Share of Homeowners Likely to Move in Q3 2018 in Chicago, DC, Orlando, Tampa, Atlanta – ATTOM

On other countries:

- [China] China’s new home price growth hits two-year high as small cities boom – Reuters

- [Germany] Creating Permanent Housing Affordability: Lessons From German Cooperative Housing Models – Urban Institute

- [New Zealand] New Zealand bans sales of homes to foreigners – BBC

- [Singapore] Singapore Home Prices Won’t Pop Without More Migrants – Bloomberg

Photo by Aliis Sinisalu

On cross-country:

- Our cities house-price index suggests the property market is slowing – Economist

- Global House Price Index – Economist

- Planning rules are driving the global housing crisis – Financial Times

- Opinion today: Demented by the housing crisis: Simply comparing the number of households to dwellings gives a foolishly misleading idea – Financial Times

On the US:

- Our Shrinking Supply of Low-Cost Rental Units – Joint Center for Housing Studies

- Who Owns a Home in America,

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts