Sunday, November 25, 2018

How does monetary policy affect income and wealth inequality?

From a new paper by Yannis Dafermos and Christos Papatheodorou:

“The recent empirical literature on the distributional effects of monetary policy on inequality has focused on the various channels through which a change in the policy interest rate or the central bank asset purchases affect income and wealth inequality. Although most studies show that expansionary (contractionary) conventional policy tends to reduce (increase) income inequality (see Coibion et al., 2017; Mumtaz and Theophilopoulou, 2017; Furceri et al., 2018; Guerello, 2018; Ampudia et al., 2018), there is no consensus on whether these effects are economically significant. In addition, there is no consensus about (i) the size and the direction of the effects of conventional monetary policy on wealth inequality and (ii) the distributional impact of quantitative easing (see e.g. Saiki and Frost, 2014; Domaski et al., 2016; Montecino and Epstein, 2017; Mumtaz and Thephilopoulou, 2017; O’Farrell and Rawdanowicz, 2016; Ampudia et al., 2018; Casiraghi et al., 2018; Guerello, 2018; Koedijk, 2018). This comes as no surprise: the magnitude of the distribution channels of monetary policy depends on a number of factors which influence the impact of these channels across countries and time periods. For example, it has been shown that the effect of monetary policy on inequality depends on the initial wealth distribution and the composition of household financial assets (O’Farrell and Rawdanowicz, 2017; Guerello, 2018), the initial wage share (Furceri et al., 2018) and the marginal propensity to consume (Ampudia et al., 2018).

Despite these recent developments in the empirical literature, there is currently no theoretical model that incorporates the key distribution channels of monetary policy simultaneously and is capable of analysing in a systematic way the exact conditions under which monetary policy has economically significant effects on inequality. This paper develops such a model by combining the agent-based (AB) and the stock-flow consistent (SFC) approaches to macroeconomic modelling. The SFC approach is characterised by the explicit incorporation of accounting principles into dynamic macro modelling and the emphasis that it places on the dynamic interplay between monetary stocks and flows (see Godley and Lavoie, 2007a). The AB approach is suitable for exploring how macroeconomic phenomena emerge out of the interactions between heterogeneous agents. It has been recently argued that the combination of agent-based and stockflow consistent approaches is a fruitful avenue for the reconstruction of macroeconomics, moving beyond the conventional representative agents framework (see e.g. van der Hoog and Dawid, 2015; Caiani et al., 2016).”

From a new paper by Yannis Dafermos and Christos Papatheodorou:

“The recent empirical literature on the distributional effects of monetary policy on inequality has focused on the various channels through which a change in the policy interest rate or the central bank asset purchases affect income and wealth inequality. Although most studies show that expansionary (contractionary) conventional policy tends to reduce (increase) income inequality (see Coibion et al., 2017; Mumtaz and Theophilopoulou,

Posted by at 1:04 PM

Labels: Inclusive Growth

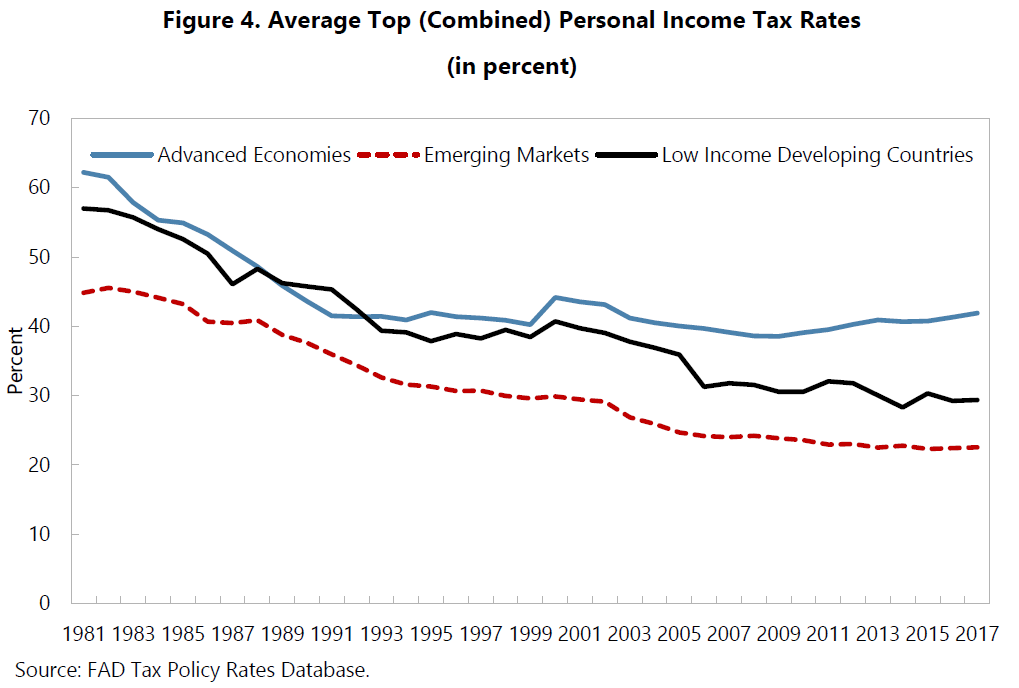

Personal Income Tax Progressivity: Trends and Implications

From a new IMF working paper:

“This paper has approached progressivity from different angles. Bringing together our findings, we can conclude strongly that progressivity has decreased over the last few decades, a finding that is robust to the choice of measure. We also conclude, but with less certainty, that the reduction in progressivity appears not to have given growth a boost.

While this paper focused on personal income taxes, developments in capital income taxation are also likely to have contributed to reducing overall progressivity: Capital income is distributed more unequally than labor income, has risen over the past few decades as a share of total income (IMF, 2017b), and is often taxed at a lower rate than labor income. The corporate income tax, in particular, plays an important role in determining progressivity. First, there can be a direct effect to the extent that it is partly borne by owners of corporations. Second, it indirectly supports the enforcement of the taxation of labor income: Corporate taxation mitigates arbitrage in response to taxation of entrepreneurial income, because distinguishing labor income from capital income can be difficult (or impossible) when individuals can freely choose the form through which they declare their income (IMF, 2014). When the personal income tax base can be shifted to some alternative tax base that is taxed at a lower rate (such as corporate income), optimal tax theory implies that the optimal tax rate on personal income rises with the tax rate on the alternative base. In recent decades, international tax competition—resulting from capital mobility—has led to a steady downward trend in corporate income tax rates (Table 2). This trend reduces overall tax progressivity and may also put downward pressure on personal income tax rates—even though labor itself is less mobile and could be taxed more easily in a globalized world.

There are many unresolved questions and areas for further research. For example, progressivity measures taking the entire tax and benefit system, and ideally even public spending, into account would enhance the understanding of overall progressivity tremendously. The challenges in finding such a measure, especially one that is still independent of pre-tax and spending distributions are enormous.

Despite the absence of a fully comprehensive measure of progressivity, and some reasonable doubts about the impact of progressivity on growth, it appears safe to say that progressivity-enhancing measures could be taken without major risks to growth. This would be especially relevant in countries that are marked by great inequality.”

From a new IMF working paper:

“This paper has approached progressivity from different angles. Bringing together our findings, we can conclude strongly that progressivity has decreased over the last few decades, a finding that is robust to the choice of measure. We also conclude, but with less certainty, that the reduction in progressivity appears not to have given growth a boost.

While this paper focused on personal income taxes,

Posted by at 12:57 PM

Labels: Inclusive Growth

Saturday, November 24, 2018

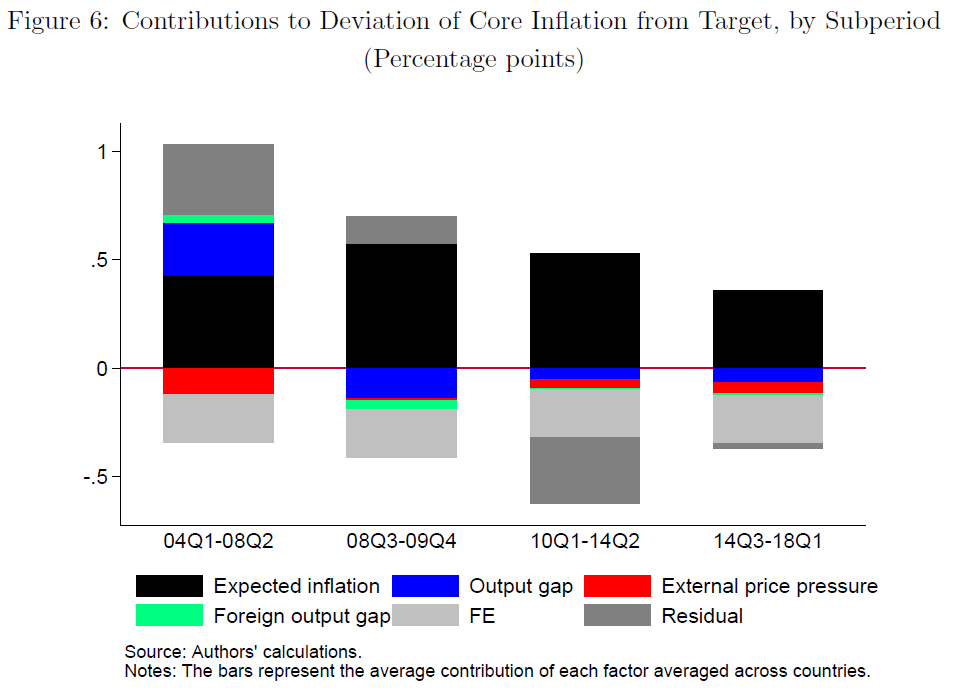

Is Inflation Domestic or Global? Evidence from Emerging Markets

From a new IMF working paper:

“Following a period of disinflation during the 1990s and early 2000s, inflation in emerging markets has remained remarkably low. The volatility and persistence of inflation also fell considerably and remained low despite large swings in commodity prices, the global financial crisis, and periods of strong and sustained US dollar appreciation. A key question is whether this improved inflation performance is sustainable or rather reflects global disinflationary forces that could prove temporary. In this paper, we use a New-Keynesian Phillips curve framework and data for 19 large emerging market economies over 2004-18 to assess the contribution of domestic and global factors to domestic inflation dynamics. Our results suggest that longer-term inflation expectations, linked to domestic factors, were the main determinant of inflation. External factors played a considerably smaller role. The results underscore that although emerging markets are increasingly integrated into the global economy, policymakers remain largely in control of domestic inflation developments.”

From a new IMF working paper:

“Following a period of disinflation during the 1990s and early 2000s, inflation in emerging markets has remained remarkably low. The volatility and persistence of inflation also fell considerably and remained low despite large swings in commodity prices, the global financial crisis, and periods of strong and sustained US dollar appreciation. A key question is whether this improved inflation performance is sustainable or rather reflects global disinflationary forces that could prove temporary.

Posted by at 7:44 PM

Labels: Inclusive Growth

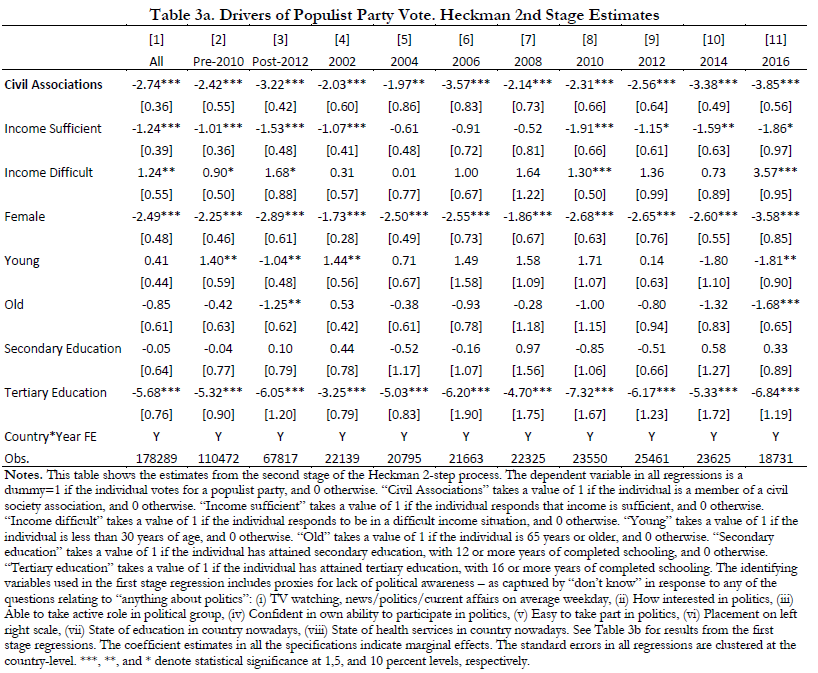

Populism and Civil Society

From a new IMF working paper:

“Populists claim to be the only legitimate representative of the people. Does it mean that there is no space for civil society? The issue is important because since Tocqueville (1835), associations and civil society have been recognized as a key factor in a healthy liberal democracy. We ask two questions: 1) do individuals who are members of civil associations vote less for populist parties? 2) does membership in associations decrease when populist parties are in power? We answer these questions looking at the experiences of Europe, which has a rich civil society tradition, as well as of Latin America, which already has a long history of populists in power. The main findings are that individuals belonging to associations are less likely by 2.4 to 4.2 percent to vote for populist parties, which is large considering that the average vote share for populist parties is from 10 to 15 percent. The effect is strong particularly after the global financial crisis, with the important caveat that membership in trade unions has unclear effects.”

From a new IMF working paper:

“Populists claim to be the only legitimate representative of the people. Does it mean that there is no space for civil society? The issue is important because since Tocqueville (1835), associations and civil society have been recognized as a key factor in a healthy liberal democracy. We ask two questions: 1) do individuals who are members of civil associations vote less for populist parties?

Posted by at 7:34 PM

Labels: Inclusive Growth

Solow on Friedman’s 1968 Presidential Address and the Medium Run

From a new post by Timothy Taylor:

“Robert Solow is a notable player in these disputes: in particular, in his 1960 paper with Paul Samuelson, “Analytical Aspects of Anti-Inflation Policy” (American Economic Review, 50:2, pp. 177-194). In an essay in the Winter 2000 issue of the Journal of Economic Perspectives, “Toward a Macroeconomics of the Medium Run,” Solow addressed this question of thinking about macroeconomic policy in the short- and the long-run. He wrote:

I can easily imagine that there is a “true” macrodynamics, valid at every time scale. But it is fearfully complicated, and nobody has a very good grip on it. At short time scales, I think, something sort of “Keynesian” is a good approximation, and surely better than anything straight “neoclassical.” At very long time scales, the interesting questions are best studied in a neoclassical framework, and attention to the Keynesian side of things would be a minor distraction. At the five-to-ten-year time scale, we have to piece things together as best we can, and look for a hybrid model that will do the job.

In this most recent essay, “A Theory is a Sometime Thing,” Solow pushes this idea of medium-run thinking harder. He acknowledges that if a central bank can only cause the interest rate and unemployment rate to shift for a year or two, in the short-run before a rebound to what is determined in the long run, then when problems of lags in timing are included, macroeconomic policy might be dysfunctional. But if a central bank can affect the interest rate and the unemployment rate for a medium-run period of, say 5-7 years, then even with some uncertainty and lags, macroeocnomic policy may be quite relevant and possible. At one point, Solow writes: “The medium run is where we live.””

From a new post by Timothy Taylor:

“Robert Solow is a notable player in these disputes: in particular, in his 1960 paper with Paul Samuelson, “Analytical Aspects of Anti-Inflation Policy” (American Economic Review, 50:2, pp. 177-194). In an essay in the Winter 2000 issue of the Journal of Economic Perspectives, “Toward a Macroeconomics of the Medium Run,” Solow addressed this question of thinking about macroeconomic policy in the short- and the long-run.

Posted by at 7:30 PM

Labels: Macro Demystified

Subscribe to: Posts