Wednesday, November 14, 2018

Macroprudential Policies and House Prices in Europe: An Overview of Recent Experiences

From the IMF’s latest Regional Economic Outlook report for Europe:

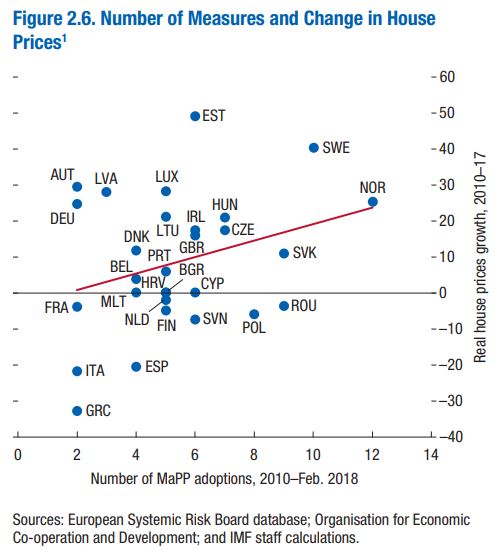

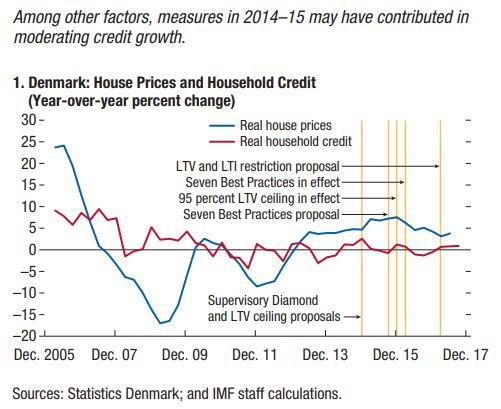

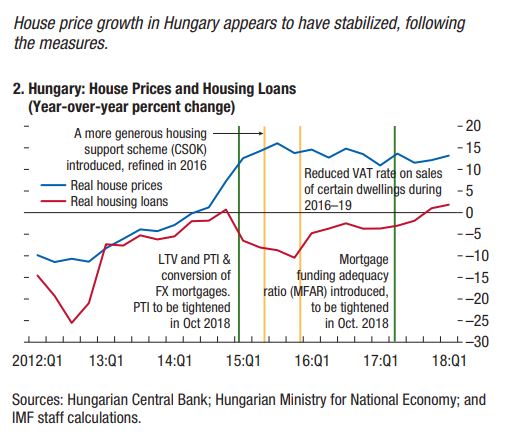

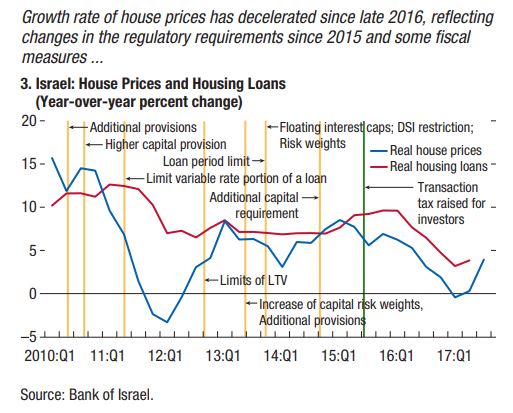

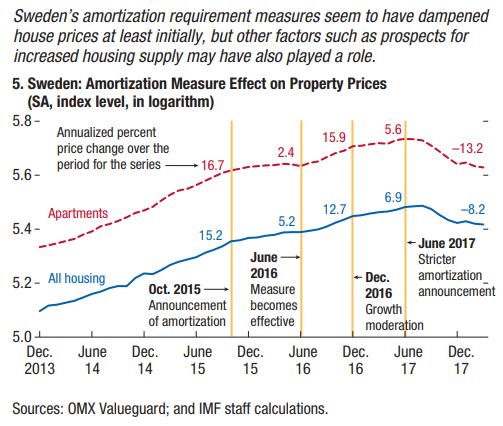

“This chapter documents the increasing use of macroprudential policies (MaPPs) in Europe in recent years to build financial resilience, contain general and sectoral credit growth, and limit house price increases. Considering these objectives and drawing from case studies, the chapter finds evidence that borrower-side measures, supported by lender-side measures, helped limit the share of riskier mortgages, thereby building resilience. Evidence is more mixed as to the ability of MaPPs to contain house price and overall credit growth against the backdrop of a still-accommodative monetary policy and other factors.

Macroprudential Measures in European Countries

The recent reacceleration in house prices has prompted the adoption of MaPPs in several European countries. Though credit and house price concerns are not yet generalized, house prices have increased substantially in several European countries over the past few years (…). In most of these countries, higher house prices have been accompanied by rising household debt (…) and rapid household credit growth (…).

To contain the buildup of systemic risks, especially in the residential housing market, many European countries have strengthened their MaPPs (…). While MaPPs have been

implemented across Europe, countries with larger postcrisis increases in house prices and household debt tended to adopt more MaPPs (…).The main objectives of the recently introduced MaPPs, as stated by country authorities, were improving financial stability, building financial resilience, and containing general and sectoral credit growth. Within these broader objectives, policies were generally focused on protecting borrowers, strengthening banking systems, and slowing down house price increases (…). The latter was an objective in most economies, but particularly in the Czech Republic, Estonia, Norway, and Sweden.

In some countries (Estonia, Norway, Switzerland), the relaxation of lending standards was a major concern. Constraining the rise in the share of loans denominated in foreign currency was a prominent goal in Hungary. The various capital buffers adopted beginning in 2013, in line with the EU Capital Requirements Directive (CRD IV), were aimed at containing not only housing sector imbalances, but also credit cycle swings.”

Continue reading here.

From the IMF’s latest Regional Economic Outlook report for Europe:

“This chapter documents the increasing use of macroprudential policies (MaPPs) in Europe in recent years to build financial resilience, contain general and sectoral credit growth, and limit house price increases. Considering these objectives and drawing from case studies, the chapter finds evidence that borrower-side measures, supported by lender-side measures, helped limit the share of riskier mortgages, thereby building resilience. Evidence is more mixed as to the ability of MaPPs to contain house price and overall credit growth against the backdrop of a still-accommodative monetary policy and other factors.

Posted by at 2:30 PM

Labels: Global Housing Watch

House Prices in Iceland

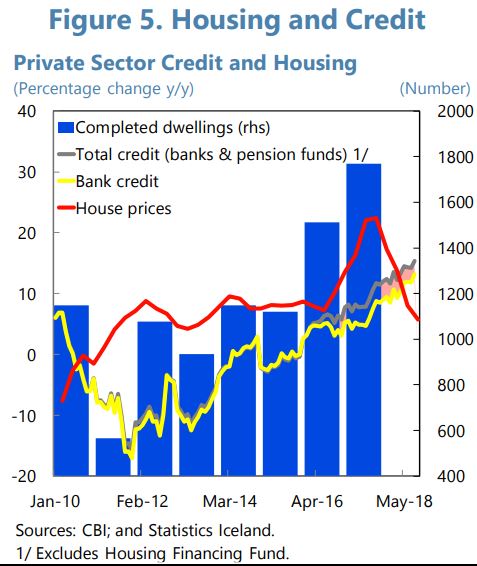

The IMF’s latest report on Iceland says that:

“The real estate markets have cooled. The rate of growth of housing prices fell from a peak of 24 percent y/y in July 2017 to 6 percent 12 months later, while that for commercial real estate slowed from 19 percent y/y to 15 percent. A robust supply response was key, although slowing tourism growth also helped—including by limiting private rental demand via Airbnb (see for instance Eliasson and Ragnarsson, 2018). Residential investment and commercial construction continue to expand briskly.”

Also, see a separate report on Inflation Targeting in Iceland–The Issue of Housing Costs here.

The IMF’s latest report on Iceland says that:

“The real estate markets have cooled. The rate of growth of housing prices fell from a peak of 24 percent y/y in July 2017 to 6 percent 12 months later, while that for commercial real estate slowed from 19 percent y/y to 15 percent. A robust supply response was key, although slowing tourism growth also helped—including by limiting private rental demand via Airbnb (see for instance Eliasson and Ragnarsson,

Posted by at 2:19 PM

Labels: Global Housing Watch

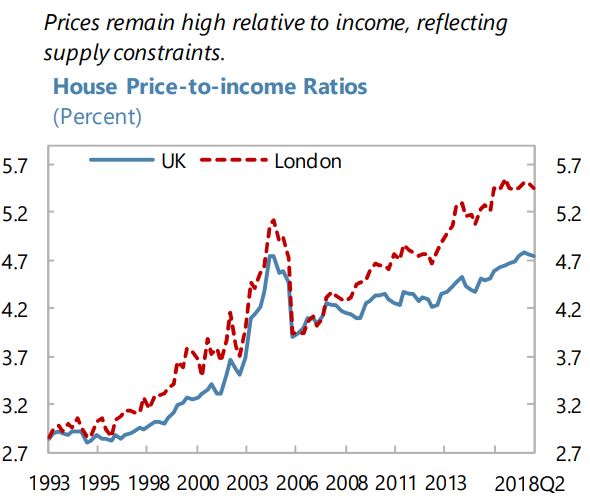

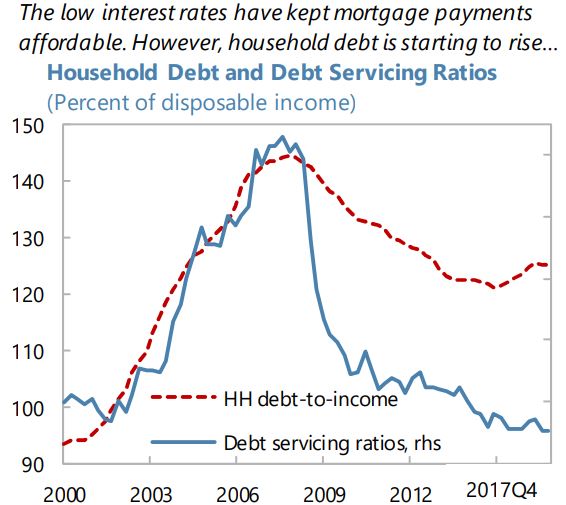

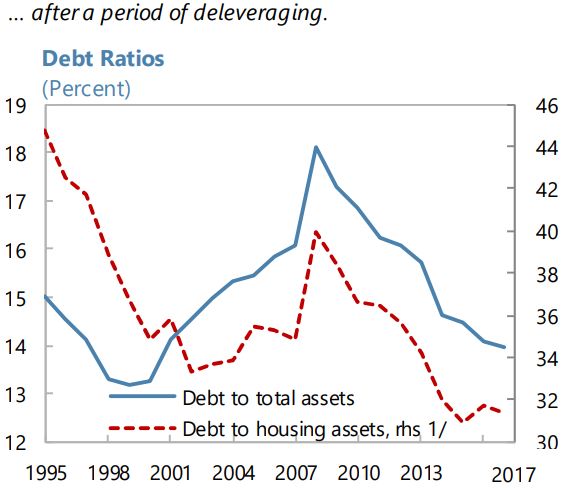

House Prices in United Kingdom

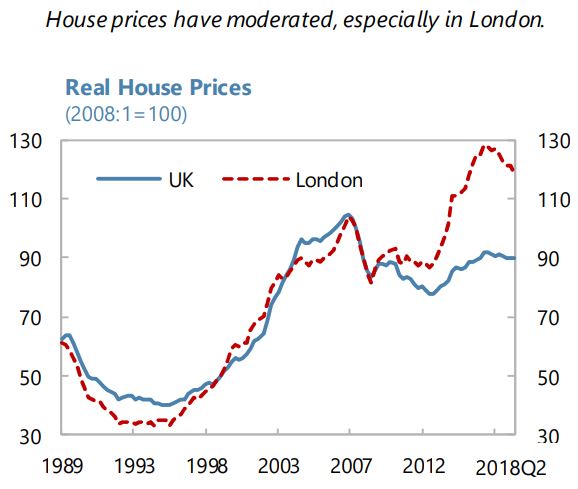

From the IMF’s latest report on the United Kingdom:

“Mortgage lending growth has been moderate, owing in part to subdued demand, as well as macroprudential measures taken in recent years. Despite the recent moderation in residential house price growth (and outright declines in parts of London), house prices remain high relative to incomes (…). The ratio of new mortgage loans at relatively high loan-to-income (LTI) ratios has increased somewhat in the last two years, although the share of highly indebted households remains low. Since 2014, mortgage lenders have been required to test whether borrowers could still afford their mortgages in a stressed rates scenario.”

From the IMF’s latest report on the United Kingdom:

“Mortgage lending growth has been moderate, owing in part to subdued demand, as well as macroprudential measures taken in recent years. Despite the recent moderation in residential house price growth (and outright declines in parts of London), house prices remain high relative to incomes (…). The ratio of new mortgage loans at relatively high loan-to-income (LTI) ratios has increased somewhat in the last two years,

Posted by at 2:13 PM

Labels: Global Housing Watch

Simple Rules for Climate Policy and Integrated Assessment

From a new working paper by Frederick van der Ploeg and Armon Rezai:

“A simple integrated assessment framework that gives rules for the optimal carbon price, transition to the carbon-free era and stranded carbon assets is presented, which highlights the

ethical, economic, geophysical and political drivers of optimal climate policy. For the ethics we discuss the role of intergenerational inequality aversion and the discount rate, where we show the importance of lower discount rates for appraisal of longer run benefit and of policy makers using lower discount rates than private agents. The economics depends on the costs and rates of technical progress in production of fossil fuel, its substitute renewable energies and sequestration. The geophysics depends on the permanent and transient components of

atmospheric carbon and the relatively fast temperature response, and we allow for positive feedbacks. The politics stems from international free-rider problems in absence of a global

climate deal. We show how results change if different assumptions are made about each of the drivers of climate policy. Our main objective is to offer an easy back-on-the-envelope analysis, which can be used for teaching and communication with policy makers.”

From a new working paper by Frederick van der Ploeg and Armon Rezai:

“A simple integrated assessment framework that gives rules for the optimal carbon price, transition to the carbon-free era and stranded carbon assets is presented, which highlights the

ethical, economic, geophysical and political drivers of optimal climate policy. For the ethics we discuss the role of intergenerational inequality aversion and the discount rate, where we show the importance of lower discount rates for appraisal of longer run benefit and of policy makers using lower discount rates than private agents.

Posted by at 2:01 PM

Labels: Energy & Climate Change

Monday, November 12, 2018

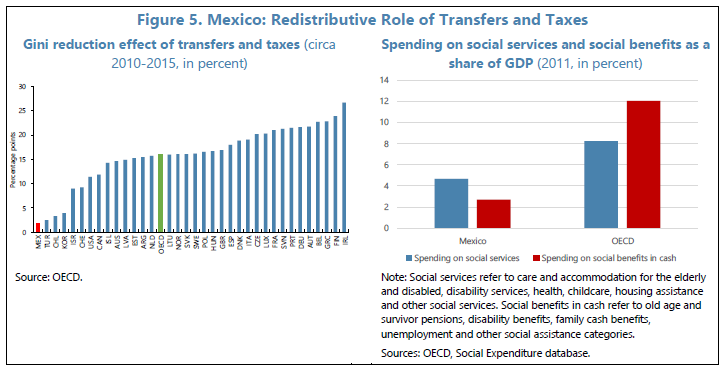

Inequality and Social Policies

An IMF country report analyzes the “income inequalities and government transfers using microdata from Mexico’s survey on household income and expenditures (ENIGH). It highlights the positive role played by government transfers in reducing inequalities over 2004-2016 and suggests that there is scope for better targeting existing social programs.”

“Transfers and taxes play a much more limited role in alleviating inequalities in Mexico than in other OECD countries. The Gini reduction effect of transfers and taxes is lower in Mexico than in all OECD countries. This limited redistributive role of fiscal policies in Mexico may result from a tax system that is insufficiently progressive. It also reflects the low level of public social spending as a share of GDP, in particular on non-contributory cash transfers targeted at the poorest households.”

“Transfers and taxes play a much more limited role in alleviating inequalities in Mexico than in other OECD countries. The Gini reduction effect of transfers and taxes is lower in Mexico than in all OECD countries. This limited redistributive role of fiscal policies in Mexico may result from a tax system that is insufficiently progressive. It also reflects the low level of public social spending as a share of GDP, in particular on non-contributory cash transfers targeted at the poorest households.”

“After a modest increase over 2007-2015, public social spending as a share of GDP has

fallen in the last two years. Public social spending increased by 2.5 percent of GDP from 2007 to

2015, reaching a maximum of 12.1 percent of GDP, before shrinking to 10.4 percent in 2017. Social

assistance and education, the first two components of public social spending, absorb together more

than 60 percent of the total, while health expenditures amount to close to a fourth.”

“Mexico’s social assistance programs cover well households at the bottom of the income distribution. 31 percent of the households in the bottom income quintile benefit from Mexico’s conditional cash transfer program Prospera (formerly known as Oportunidades and initially launched as Progresa), which has served as a model for many countries around the world (Parker and Todd, 2017). Similarly, the share of households benefiting from old-age social assistance is three times higher in the first income quintile than in the fifth one. Prospera and old-age social assistance programs account for about ¾ of the decline in the Gini coefficient coming from government transfers, while they represent about half of the total government transfer amount received by an average household.”

An IMF country report analyzes the “income inequalities and government transfers using microdata from Mexico’s survey on household income and expenditures (ENIGH). It highlights the positive role played by government transfers in reducing inequalities over 2004-2016 and suggests that there is scope for better targeting existing social programs.”

“Transfers and taxes play a much more limited role in alleviating inequalities in Mexico than in other OECD countries. The Gini reduction effect of transfers and taxes is lower in Mexico than in all OECD countries.

Posted by at 9:42 PM

Labels: Inclusive Growth

Subscribe to: Posts