Wednesday, October 17, 2018

The economics of artificial intelligence: Implications for the future of work

From a new ILO working paper:

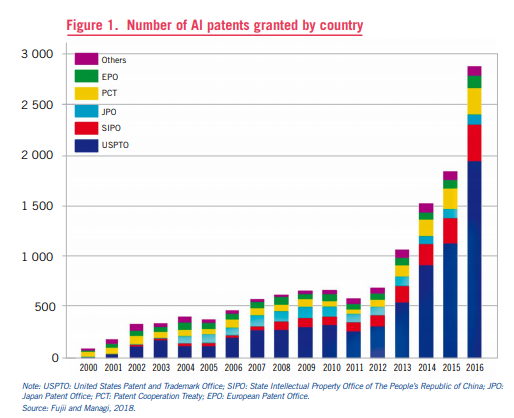

“The current wave of technological change based on advancements in artificial intelligence (AI) has created widespread fear of job losses and further rises in inequality. This paper discusses the rationale for these fears, highlighting the specific nature of AI and comparing previous waves of automation and robotization with the current advancements made possible by a wide-spread adoption of AI. It argues that large opportunities in terms of increases in productivity can ensue, including for developing countries, given the vastly reduced costs of capital that some applications have demonstrated and the potential for productivity increases, especially among the low-skilled. At the same time, risks in the form of further increases in inequality need to be addressed if the benefits from AI-based technological progress are to be broadly shared. For this, skills policy are necessary but not sufficient. In addition, new forms of regulating the digital economy are called for that prevent further rises in market concentration, ensure proper data protection and privacy and help share the benefits of productivity growth through a combination of profit sharing, (digital) capital taxation and a reduction in working time. The paper calls for a moderately optimistic outlook on the opportunities and risks from artificial intelligence, provided policy-makers and social partners take the particular characteristics of these new technologies into account.”

From a new ILO working paper:

“The current wave of technological change based on advancements in artificial intelligence (AI) has created widespread fear of job losses and further rises in inequality. This paper discusses the rationale for these fears, highlighting the specific nature of AI and comparing previous waves of automation and robotization with the current advancements made possible by a wide-spread adoption of AI. It argues that large opportunities in terms of increases in productivity can ensue,

Posted by at 3:21 PM

Labels: Inclusive Growth

The secular decline in US employment over the past two decades

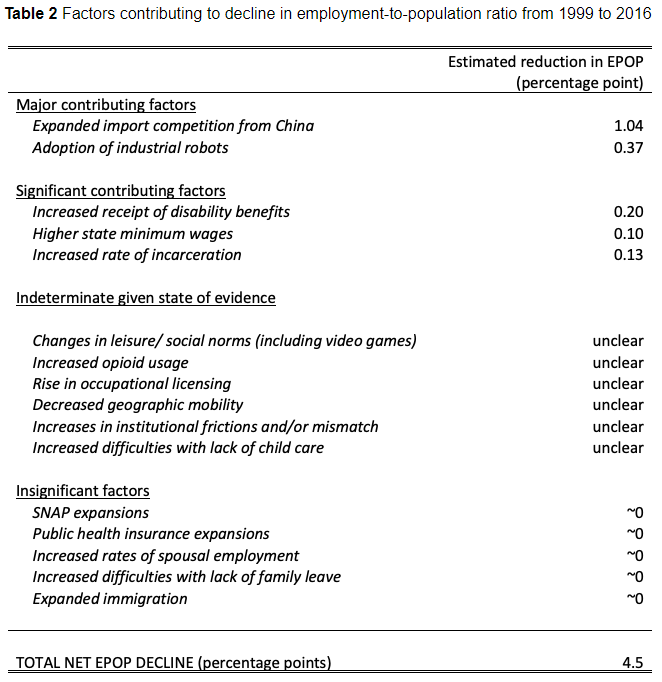

A new VOX post “reviews the evidence on the main causes of the secular decline in employment since the turn of the century. Labour demand factors – notably import competition from China and the rise of industrial robots – emerge as the key drivers. Some labour supply and institutional factors also have contributed to the decline, but to a lesser extent.”

“Among the effects for which we were able to construct an estimate, increased import competition from China is the single largest contributing factor to the decline in employment. A great deal of empirical evidence links import competition from China to the decline in manufacturing employment. These import pressures also had negative employment effects on ‘upstream’ intermediate goods industries, as well as other non-manufacturing industries (Acemoglu et al. 2016, Autor et al. 2015). Estimates from Acemoglu et al. (2016) are the basis for our estimate that the 302% increase in Chinese imports (measured in 2007 US dollars) from 1999 to 2016 led to displacement of approximately 2.65 million workers, a 1.04 percentage point shift in the employment-population ratio.”

“The employment effects from industrial robots are most clearly documented by Acemoglu and Restrepo (2017), who find that each additional robot per thousand workers between 1993 and 2007 reduced employment by 5.6 workers. This estimate implies that the rise in the stock of robots between 2007 and 2016 displaced 0.95 million workers, equivalent to a 0.37 percentage point decline in the employment-to-population ratio.Although improvements in computing technology have been if anything even more ubiquitous, Autor et al. (2015) find that competition from computing technology affects only routine task-intensive occupations, and that any employment losses in those occupations were offset by employment gains in abstract and manual task-intensive occupations.”

Labour supply factors as a group have been considerably less important than labour demand factors in driving the decline in employment.The claim that expanded safety net support through SNAP (food stamps) or Medicaid led to sizable decreases in employment is hard to square with either the institutional features of these programmes or the evidence on causal linkages. Careful work finds little to no labour supply effects of these programmes, and as a practical matter, they offer very little by way of income support to able-bodied childless adults (see, for example, Hoynes and Schanzenbach 2016 on SNAP, and Leung and Mas 2016 on Medicaid.)

That said, the availability of lifelong disability insurance benefits through the Social Security Disability Insurance (SSDI) programme and the Veterans Affairs Disability Compensation (VADC) programme has contributed modestly to falling employment rates. Applying age-group specific causal labour supply estimates from Maestes et al. (2013) to the growth in the SSDI caseload over and above that due to the population becoming older yields an estimated 0.14 percentage point decline in the e/pop ratio over our time period owing to growth in this programme. Applying the labour supply elasticity from a recent study of an exogenous policy change to VADC program eligibility (Autor et al. 2016) to an estimate of the excess VADC caseload implies that programme’s growth led to an e/pop decline of perhaps 0.06 percentage points.

One might expect the tremendous rise in incarceration in the US to have been a significant driver of declining employment, but because so many incarcerated individuals had low levels of labour force attachment even before their prison term, we estimate only a modest aggregate effect. Applying the causal estimates from Mueller-Smith (2015) to rough estimates of the number of former prisoners by length of time served and prior earnings history, our very rough estimate is that perhaps 0.13 percentage points of the decline in e/pop between 1999 and 2016 can be attributed to policy-induced increases in incarceration. Minimum wage increases probably also had a small but non-negligible impact, especially among younger, less-skilled workers. Taking account of the range of estimates produced by credible study designs, we estimate that increases in state and local minimum wages might have contributed 0.10 percentage points to the e/pop decline.

Other plausible factors driving the decline in employment are the sharp rise in occupational licensing (Kleiner and Krueger 2013), the decline in geographic mobility (Molloy et al. 2011), and increased difficulties securing affordable, high-quality child care. We do not attempt to assign a magnitude to these factors because we lack sufficient evidence to establish the causal impact of these factors or, in the case of child care, to assess how much the factor itself has changed. Another open question is to what extent anecdotes about worsening mismatch between the skills workers possess and those that employers need are borne out in the data.

Scholars have noted the connection of both increased leisure time (including time playing video games) (Aguiar et al. 2017) and increased opioid use (Krueger 2017, Currie et al. 2018) with non-employment, but whether one is causing the other or vice versa, or they are all manifestations of other societal changes, is not easy to disentangle.”

A new VOX post “reviews the evidence on the main causes of the secular decline in employment since the turn of the century. Labour demand factors – notably import competition from China and the rise of industrial robots – emerge as the key drivers. Some labour supply and institutional factors also have contributed to the decline, but to a lesser extent.”

“Among the effects for which we were able to construct an estimate,

Posted by at 1:14 PM

Labels: Inclusive Growth

Tuesday, October 16, 2018

Housing and Macroeconomics

Global Housing Watch Newsletter: October 2018

*Below is a summary of a workshop prepared by Benjamin Larin (Leipzig University), Hans Torben Löfflad (Leipzig University), Konstantin Gantert (Leipzig University).

What drives house price fluctuations? How do fluctuations in house prices and credit affect the real economy? What explains the long-run dynamics of house prices? How do house prices and rents affect wealth inequality and individual welfare? These are some of the questions that were discussed at a recent event.

The European Association of Young Economists (EAYE), in collaboration with Leipzig University, organized the first EAYE Workshop on Housing and Macroeconomics. This newly established workshop will take place annually and will focus on a specific topic. The workshop is organized by young economists, and it is meant for young economists. This year’s keynote lectures were Moritz Kuhn (University of Bonn, CEPR, IZA) and Alberto Martín (ECB, CREI, Barcelona GSE). What follows is a summary of this year’s workshop.

Credit cycles, housing, and short-term fluctuations

How credit and the real side of the economy are linked, and how financial shocks translate to changes in GDP—this is one of the questions that was asked frequently at the workshop. One paper analyzed the effects of credit expansion on aggregate demand in Denmark. The authors find that additional demand due to credit expansion is mostly spend in the non-tradable sector. Employment increases, mostly at small firms, yet the average labor separation rate is found to be higher for those jobs. Another paper analyzed the supply side effects of housing on the macroeconomy. The authors found that housing supply elasticities have decreased over the course of the last two US housing boom-bust episodes, implying more volatile house prices.

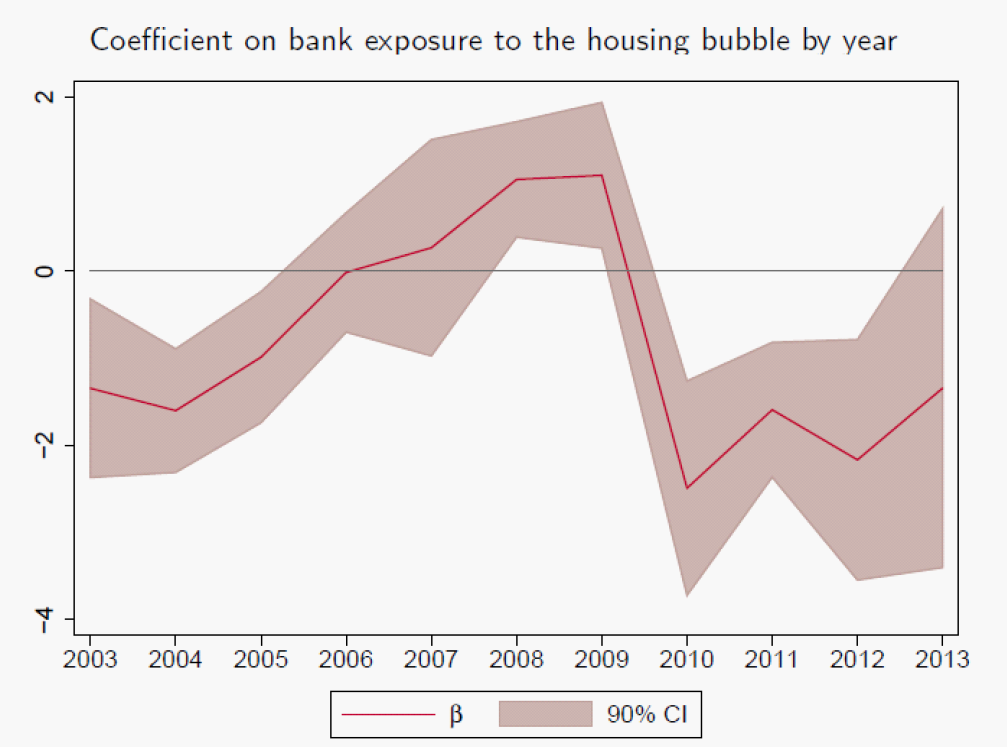

In the first keynote lecture, Alberto Martin presented a theory of macroeconomics of rational bubbles with an application to housing bubbles. He showed that a housing bubble leads to investment into the housing sector, first crowding out investment in non-housing firms (see figure 1). As bank capital increases over time, credit to non-housing firms increases as well. As the housing bubble bursts, this development reverses as credit lines freeze.

Figure 1.

Note: Coefficient of housing credit exposure of banks on credit growth to non-financial firms in the U.S. from 2003 to 2013. A value below 0 indicates a fall in credit to non-housing firms as the exposure to housing credit of a bank increases.

The real effects of housing credit on the macroeconomy are driven by changes in the credit side of the economy. A paper presented preliminary evidence that there is again a housing bubble in the U.S. and in other OECD economies. The housing bubbles in the U.S. seem to be geographically clustered, yet county specific factors cannot explain this. Bubbles do in general induce investment and growth through collateral feedback loops, yet they also create significant costs when they burst. When a bubble bursts feedback loops amplify the effects on the real economy. One channel is the excessively volatile risk premium that has to be paid. Another channel is the fluctuation in housing liquidity due to a change in the average time-to-sell margin. When everybody wants to sell their house, there is a supply side overhang and the liquidity of houses decreases strongly. This leads to a decrease in the value of houses.

Policy applications

As volatility of risk and house prices is high and its economic costs are large, the question arises whether policy can smooth this cycle and increase welfare. Two papers discussed different policy measures.

First, is macroprudential policy useful as an aggregate policy tool or should it take regional heterogeneity into account? A model-based analysis shows that taking the regional heterogeneity of house prices into account has potential benefits over classical monetary policy targeting inflation and one-size-fits-it-all macroprudential policy.

The second paper asked whether monetary policy effectiveness changes depending on the leverage cycle. The authors show that monetary policy is very effective when households deleverage, and credit constraints are binding, while it has only small effects when household leverage is increasing.

A third paper took a completely different angle on housing and studied the effect of the recent refugee inflow on rents in Germany. The authors find, very surprisingly, that local rents decrease as refugees move in. A possible explanation is the crowding out of the original population to different places in response to the inflow of refugees in their neighborhood.

Growth and wealth distribution

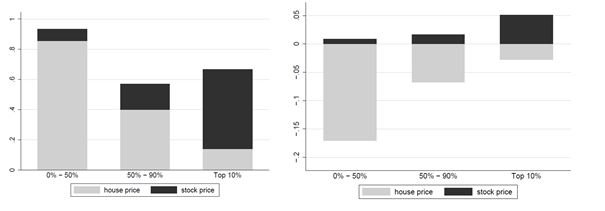

Some presentations at the workshop studied the relevance of the portfolio composition and house prices on the dynamics of wealth inequality. As the bottom 90 percent of the U.S. wealth distribution have a very large housing portfolio share, and hold only a small fraction of equity, it is paramount to wealth distribution how the two assets develop relatively to each other. Moritz Kuhn emphasized that the evolution of wealth inequality is the result of a race between housing and equity performance (see figure 2). When housing does relatively better, wealth inequality decreases. When equity does relatively better, wealth inequality increases.

Figure 2.

Note: The left figure indicates the wealth growth of different groups of the wealth distribution in the U.S. separated for housing and equity between 1998 and 2007. The right figure shows the impact on wealth growth from 2008 to 2016.

The significance of this statement has further been shown by a presentation on wealth inequality in Spain. There, wealth inequality did not increased significantly as rich households held a relatively high share of housing in their portfolio. Moritz Kuhn further emphasized the importance of data on the joint distribution of income and wealth for better understanding the dynamics of income and wealth inequality.

Takeaways from the workshop

Housing and Macroeconomics is an increasingly important topic. And as the many high-quality presentations have showed, young economists are aware of the importance of this topic. Housing has both short and long-run effects on the macroeconomy and the two dimensions might be connected. The financialization of housing drives both the business cycle and long-run wealth inequality. Therefore, housing is an important determinant for welfare and the economy in general.

Note: Photo on the left: Alberto Martin, center photo: participants at the workshop, right photo: Moritz Kuhn.

Global Housing Watch Newsletter: October 2018

*Below is a summary of a workshop prepared by Benjamin Larin (Leipzig University), Hans Torben Löfflad (Leipzig University), Konstantin Gantert (Leipzig University).

What drives house price fluctuations? How do fluctuations in house prices and credit affect the real economy?

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, October 15, 2018

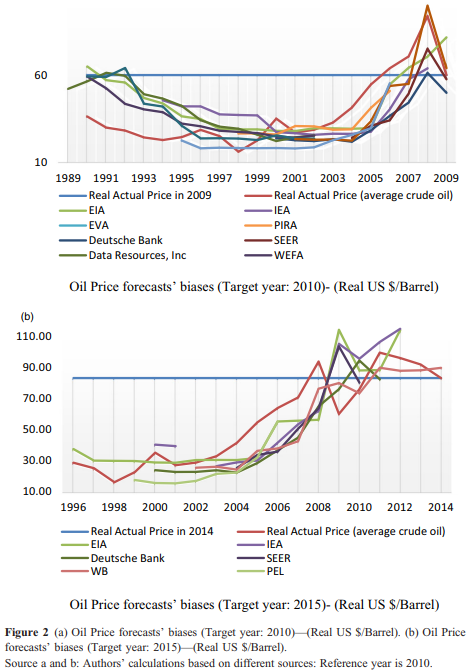

Are published oil price forecasts efficient?

A new paper assesses “the accuracy and efficiency of crude oil price forecasts published by different organisations, think tanks and companies. Since the sequence of published forecasts appears as smooth, the weak efficiency criterion is clearly violated. Even combining forecasts, cannot increase efficiency due to high correlation among various forecasts. This pattern of oil price forecasts can be attributed to combining myopia (use current oil price levels as a basis) with Hotelling-type exponential growth. Another behavioural explanation in source of inefficiencies is that forecasters prefer to harmonise their forecasts with other forecasters in order to be not an outlier.”

A new paper assesses “the accuracy and efficiency of crude oil price forecasts published by different organisations, think tanks and companies. Since the sequence of published forecasts appears as smooth, the weak efficiency criterion is clearly violated. Even combining forecasts, cannot increase efficiency due to high correlation among various forecasts. This pattern of oil price forecasts can be attributed to combining myopia (use current oil price levels as a basis) with Hotelling-type exponential growth.

Posted by at 10:19 AM

Labels: Forecasting Forum

Friday, October 12, 2018

Housing View – October 12, 2018

On cross-country:

- Book: Housing Bubbles – SpringerLink

On the US:

- Mortgage Lending and Housing Markets – NBER

- Dark clouds gather over the US housing market – Financial Times

- 10 years later: How the housing market has changed since the crash – Washington Post

- The Housing Bust Widened the Wealth Gap. Here’s How. – Zillow

- Homeless in US: A deepening crisis on the streets of America – BBC

- Low mortgage rates and securitization: A distinct perspective on the U.S. housing boom – Brunel University of London

- Housing Sentiment Dips Slightly on Interest Rate Concerns – Fannie Mae

- 2018 Cost Burden Report: Despite improvements, affordability issues are immense – Apartment List

On other countries:

- [China] Angry Mobs Show All’s Not Well in China’s Property Sector – Bloomberg

- [Hong Kong] An Early Warning Sign for the World’s Priciest Homes Is Flashing Sell – Bloomberg

- [United Kingdom] What determines UK housing equity withdrawal in later life? – Regional Science and Urban Economics

Photo by Aliis Sinisalu

On cross-country:

- Book: Housing Bubbles – SpringerLink

On the US:

- Mortgage Lending and Housing Markets – NBER

- Dark clouds gather over the US housing market – Financial Times

- 10 years later: How the housing market has changed since the crash – Washington Post

- The Housing Bust Widened the Wealth Gap.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts