Tuesday, July 17, 2018

Balancing Financial Stability and Housing Affordability: The Case of Canada

From the IMF’s latest report on Canada:

“Housing market imbalances are prominent in Canada and are a key source of systemic

risk. Rapidly-rising house prices are usually coupled with rising household indebtedness (figure 1). High household debt raises the vulnerability of financial institutions to sharp corrections in house prices, and the interconnectedness of financial institutions make this risk systemic, not merely idiosyncratic. As such, agencies in charge of macroprudential policy/systemic risk oversight typically use macroprudential measures aimed at mitigating these risks to contain the build-up of vulnerabilities over time and enhance the resilience of the financial sector.

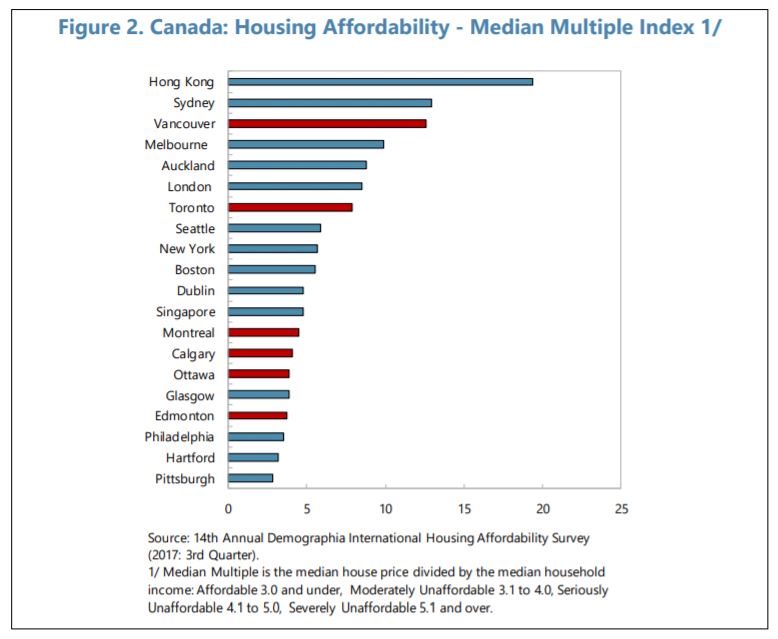

In addition to financial stability concerns, the rapid rise in housing prices has led to worsening housing affordability, posing a major problem to some of Canada’s most dynamic

metropolitan regions. Although Canada’s overall affordability indices are not yet among the worst globally, the Toronto and Vancouver regions are becoming severely unaffordable (figure 2). This raises important social and economic concerns.

The federal government has introduced a raft of macroprudential measures over the

past ten years to tackle growing housing market imbalances and associated risks to financial

stability. Initially, the measures were aimed at the high LTV ratio, government-backed insured mortgage market, helping to reduce the government’s exposure to the housing sector. In early 2018, the Office of the Superintendent of Financial Institutions (OSFI) tightened underwriting requirements for low-ratio mortgages to stem rising risk in the uninsured mortgage market. Low ratio mortgages are now subject to: (i) a stress test for mortgage interest rates; (ii) Loan-to-Value (LTV) measures and limits that reflect housing market risks, to be updated as housing markets and the economic environment evolve; and (iii) restrictions on combining mortgages with other lending products (e.g. co-lending arrangements) that could circumvent LTV limits (…).The governments of British Columbia and Ontario have also recently deployed property-tax measures to stem speculative activity and improve housing affordability in their major cities. A 15 percent nonresident property-transfer tax was introduced for the Toronto and Vancouver areas between 2016–17. More recently, the British Columbia government increased the property-transfer tax on nonresident homebuyers to 20 percent and expanded its geographic coverage.

The question remains: Which policy—macroprudential policy or property-tax policy—

best satisfies the overall objectives of policymakers? This chapter develops a simple Dynamic Stochastic-General-Equilibrium (DSGE) framework to assess the effectiveness of a specific

macroprudential policy—an LTV limit—against property-tax measures. The model is estimated using Bayesian methods and Canadian data. Operational objectives are specified for the central bank, the macroprudential authority, and the property-tax authority (assumed to be provincial governments). Optimal policy experiments are conducted to assess the overall performance of each policy given the specified objectives.”

From the IMF’s latest report on Canada:

“Housing market imbalances are prominent in Canada and are a key source of systemic

risk. Rapidly-rising house prices are usually coupled with rising household indebtedness (figure 1). High household debt raises the vulnerability of financial institutions to sharp corrections in house prices, and the interconnectedness of financial institutions make this risk systemic, not merely idiosyncratic. As such, agencies in charge of macroprudential policy/systemic risk oversight typically use macroprudential measures aimed at mitigating these risks to contain the build-up of vulnerabilities over time and enhance the resilience of the financial sector.

Posted by at 6:48 AM

Labels: Global Housing Watch

Monday, July 16, 2018

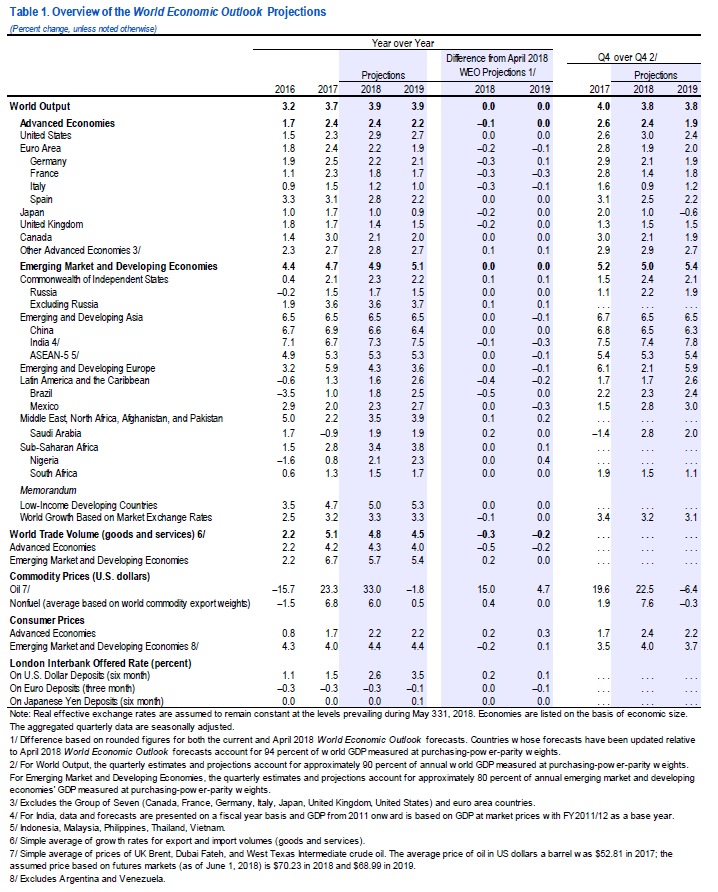

WEO July 2018: Less Even Expansion, Rising Trade Tensions

From the World Economic Outlook Update, July 2018:

“Global growth is projected to reach 3.9 percent in 2018 and 2019, in line with the forecast of the April 2018 World Economic Outlook (WEO), but the expansion is becoming less even, and risks to the outlook are mounting. The rate of expansion appears to have peaked in some major economies and growth has become less synchronized. In the United States, near-term momentum is strengthening in line with the April WEO forecast, and the US dollar has appreciated by around 5 percent in recent weeks. Growth projections have been revised down for the euro area, Japan, and the United Kingdom, reflecting negative surprises to activity in early 2018. Among emerging market and developing economies, growth prospects are also becoming more uneven, amid rising oil prices, higher yields in the United States, escalating trade tensions, and market pressures on the currencies of some economies with weaker fundamentals. Growth projections have been revised down for Argentina, Brazil, and India, while the outlook for some oil exporters has strengthened.

The balance of risks has shifted further to the downside, including in the short term. The recently announced and anticipated tariff increases by the United States and retaliatory measures by trading partners have increased the likelihood of escalating and sustained trade actions. These could derail the recovery and depress medium-term growth prospects, both through their direct impact on resource allocation and productivity and by raising uncertainty and taking a toll on investment. Financial market conditions remain accommodative for advanced economies—with compressed spreads, stretched valuations in some markets, and low volatility—but this could change rapidly. Possible triggers include rising trade tensions and conflicts, geopolitical concerns, and mounting political uncertainty. Higher inflation readings in the United States,where unemployment is below 4 percent but markets are pricing in a much shallower path of interest rate increases than the one in the projections of the Federal Open Market Committee,could also lead to a sudden reassessment of fundamentals and risks by investors. Tighter financial conditions could potentially cause disruptive portfolio adjustments, sharp exchange rate movements, and further reductions in capital inflows to emerging markets, particularly those with weaker fundamentals or higher political risks.

Avoiding protectionist measures and finding a cooperative solution that promotes continued growth in goods and services trade remain essential to preserve the global expansion. Policies and reforms should aim at sustaining activity, raising medium-term growth, and enhancing its inclusiveness. But with reduced slack and downside risks mounting, many countries need to rebuild fiscal buffers to create policy space for the next downturn and strengthen financial resilience to an environment of possibly higher market volatility.”

From the World Economic Outlook Update, July 2018:

“Global growth is projected to reach 3.9 percent in 2018 and 2019, in line with the forecast of the April 2018 World Economic Outlook (WEO), but the expansion is becoming less even, and risks to the outlook are mounting. The rate of expansion appears to have peaked in some major economies and growth has become less synchronized. In the United States, near-term momentum is strengthening in line with the April WEO forecast,

Posted by at 11:13 PM

Labels: Forecasting Forum, Inclusive Growth

Sunday, July 15, 2018

The Surge in Second Home Investments: Causes, Consequences, and Cures

Global Housing Watch Newsletter: July 2018

In this interview, Christian Hilber explores a recent global phenomenon: the surge of investment in second homes and the subsequent political backlash against wealthy investors. Building on his research, he discusses the causes of the surge, the consequences, and possible cures. Hilber is Professor of Economic Geography at the London School of Economics.

On the causes…

Hites Ahir: As you know, there has been a surge in second home investments across several countries. This refers to investment in property that is not used as primary residence, a house bought for leisure or investment purposes or a mix of the two. Could you give us some numbers that show how big is the investment boom in second homes?

Christian Hilber: The data are patchy but it appears the surge emerged in the mid-1990s. It has been more moderate in some countries, rather dramatic in others. The US or Canada belong to the former category: Between 1995 and 2005, the number of second homes increased by 20% and 22%, respectively. The UK or China belong to the latter category. The number of second homes in the UK has more than doubled between 1995 and 2013. In China, the number of investors surged from 6.6% of urban households in 2002 to 15% in 2007.

Hites Ahir: What explains this surge in second home investments?

Christian Hilber: A staggering amount of wealth accumulation among a growing cohort of ‘top earners’ certainly contributed. As housing is a normal good, a rise in income and wealth implies greater housing demand. And one way this manifests itself at the top end of the income and wealth distribution is growing consumption of second homes. But housing is also an investment good: A growing cohort of wealthy implies more investment in second homes. A lack of attractive alternative investment opportunities further reinforces the surge.

On the consequences…

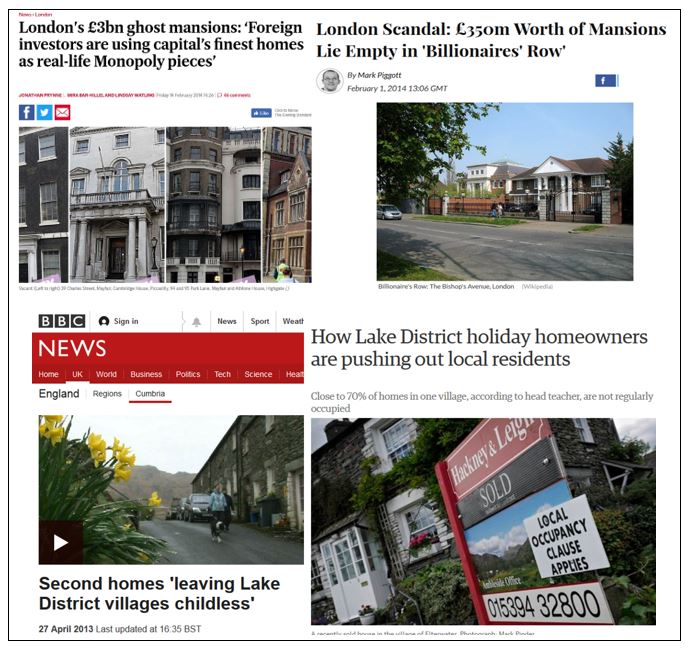

Hites Ahir: What have been the consequences of this development?

Christian Hilber: The surge in second home investments has triggered a serious political backlash in many countries. Some countries such as the UK and cities such as Vancouver introduced substantive transaction taxes on the purchase of second homes, others, such as touristic places in Switzerland or St. Ives in Cornwall, banned new second home investments altogether.

Figure 1: Newspaper coverage of sentiments against second home investors

Sources: Evening Standard, International Business Times, BBC News, Guardian

Hites Ahir: As you know, there is a growing recent literature that focuses on the role played by residential real estate investors in housing markets. Could you give us a brief summary of this literature?

Christian Hilber: The emerging literature can be divided into two strands. The first explores the role of speculative real estate investors during the last US housing boom and bust. Haughwout et al. (2011) find that investors were overrepresented in booming states, were prone to misreport their intentions to occupy their property, bid more aggressively during the boom, and defaulted at a much higher rate than owner-occupiers during the bust. Chinco and Mayer (2016) provide evidence that it was out-of-town second-house buyers rather than locals who behaved like misinformed speculators. Bayer et al. (2015) establish a causal link between speculative investor behavior and housing price booms.

The second strand focuses on international second home investments in superstar cities such as Paris (Cvijanovic and Spaenjers, 2015), London (Badarinza and Ramadorai, 2016; Sá, 2016), or NYC (Suher, 2016; Favilukis and Van Nieuwerburgh, 2017). In a nutshell, what these studies find is that investors, who possess a ‘home bias abroad’, concentrate in specific (desirable) areas, thereby increasing local house prices and transaction volumes very locally. Favilukis and Van Nieuwerburgh (2017) investigate the welfare effects. They find that higher levels of out-of-town buyers are associated with higher house prices and lower welfare. However, taxing purchases made by foreign investors can lead to welfare gains to the extent fiscal revenues are used to finance local public goods.

Hites Ahir: You have a working paper on The Housing Market Impacts of Constraining Second Home Investments with Olivier Schöni (University of Bern). What gaps your paper fills within the existing literature?

Christian Hilber: We provide a theoretical framework that illustrates the various theoretical mechanisms at play and reveals under what conditions we should expect constraints on second home investments to have positive or negative effects on local housing and labor markets. The main contribution however is empirical in nature. Exploiting a unique quasi-natural experiment in Switzerland, we are able to identify the causal economic impacts of constraining second home investments.

Hites Ahir: In your paper, you discuss the Second Home Initiative? What is it?

Christian Hilber: Initiatives are an instrument of direct democracy that allow Swiss citizens to modify the country’s constitution. Initiatives must be approved by the majority of voters and cantons.

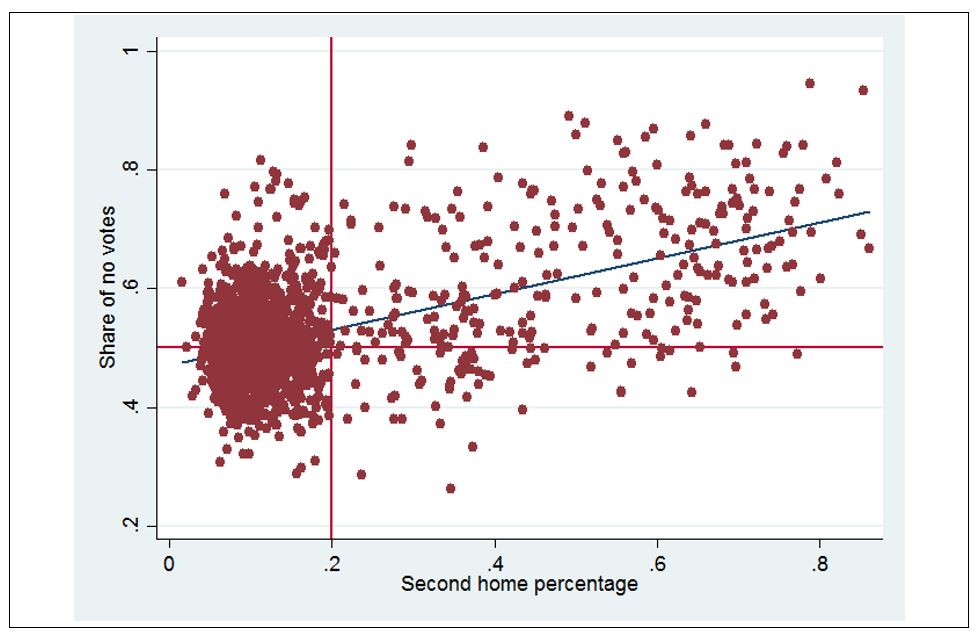

The Second Home Initiative (SHI) requested that construction of new second homes is banned in municipalities where such homes represent more than 20% of the total housing stock. The SHI was approved by the narrowest of margins—50.6% of votes and 13.5 of 26 cantons—in March 2012. It came into force in January of 2013. Voters in touristic municipalities with very high shares of second homes were heavily opposed (see Figure 3), presumably due to fears about adverse effects on the local economy. This is in contrast to voters in the larger cities who favored the initiative.

Figure 2: Second Home Initiative: The Yes and No Campaigns

Sources: www.zweitwohnungsinitiative.ch and INFOsperber. Yes-Campaign: We must stop setting our landscape in concrete vs. No-Campaign: Approving initiative would destroy your dream of second home.

Figure 3: Second Home Share and Opposition Against Initiative

Hites Ahir: Intuitively, can you walk us through the mechanisms of how a constraint on second home investment affects the price of primary and second home?

Christian Hilber: Various mechanisms are at play simultaneously. A constraint on new second home investments may help preserve the landscape and ‘character’ of a locality. This ‘amenity effect’—and its anticipation—should be positively capitalized into property values. Of course, a constraint (ban) on new second homes also makes the supply of second homes very (perfectly) price-inelastic. This should raise the price of second homes, all else equal. But then there is also what we call a ‘local economy effect’: A constraint may adversely affect local construction and other local economic activity—importantly tourism. This will lower prospective earnings and may increase unemployment. This in turn will adversely affect local demand for and the price of primary homes.

In a setting where primary and second homes are perfect substitutes, it is theoretically ambiguous whether the positive or the negative effect dominates. It depends on their relative importance. If primary and second homes are poor substitutes, then the price effects can go in opposite directions: positive for second homes and negative for primary homes.

On the cures…

Hites Ahir: What are the main findings from your paper?

Christian Hilber: We find that banning second home investments in desirable Swiss tourist locations lowered the price of primary homes (adversely affecting local homeowners), increased the price of second homes (further raising the wealth of existing second home investors), and increased unemployment rates (harming immobile local workers), compared to those locations that were not affected by the ban. These findings suggest that the negative effect on local economies dominated the positive amenity-preservation effect. It also suggests that constraining second home investments may reinforce rather than reduce wealth inequality.

Hites Ahir: How should policymakers deal with the surge in second home investments?

Christian Hilber: The political backlash against second home investors is partly driven by legitimate concerns such as ever more unaffordable housing, destruction of beautiful landscape or creation of ghost towns during large parts of the year. But banning second home investments or even transaction taxes are the wrong answer. If the primary goals are to make housing more affordable, prevent vacant homes and ghost towns, generate more local tax revenue, and reduce local wealth inequality, then an annual local tax on the value of second homes (or better even: the value of their land) would be a much superior policy response. It wouldn’t be a ‘free lunch’ though, as the local tourism and construction sectors and their workers are still bound to suffer.

More generally, second home investors—especially foreign ones—are often really just a popular scapegoat. In England, for example, the housing affordability crisis is predominately driven by an extremely inflexible and dysfunctional land use planning system and a tax system that provides virtually no incentives to local authorities to permit residential development. Banning second home investments or imposing transaction taxes on second home purchases may be politically popular policies in the short-run. But they don’t do anything to cure the underlying problems.

Hites Ahir: What kind of questions you would like future research to address on this topic?

Christian Hilber: Data limitations prevented us from exploring the impact of constraints on housing rents, homeownership attainment, or particular industries. Future research will hopefully be able to shed some light on these open questions. Moreover, less-recent quasi-natural experiments could tell us something about long-run sorting effects.

More generally, while our research focused on highly touristic areas, the backlash against second home investors is also prevalent in superstar cities, where the local economy effect may be comparably less important. Exploiting a quasi-natural experiment in a superstar city (such as the massive transaction tax imposed in Vancouver) could provide valuable insights in a different setting. Exploring the political economy of the backlash against second home investors might be another fruitful avenue for future research.

References:

Badarinza, C., Ramadorai, T. (2016). Home Away From Home? Foreign Demand and London House Prices. Working Paper.

Bayer, P., Geissler, C., Mangum, K., & Roberts, J.W. (2015). Speculators and Middlemen: The Role of Intermediaries in the Housing Market. Economic Research Initiatives at Duke (ERID) Working Paper No. 93.

Chinco, A., Mayer, C. (2016). Misinformed Speculators and Mispricing in the Housing Market, Review of Financial Studies 29(2): 486-522.

Cvijanovic, D., Spaenjers, C. (2015). Real Estate as a Luxury Good: Non-Resident Demand and Property Prices in Paris. HEC Paris Research Paper No. FIN-2015-1073.

Favilukis, J.Y. and Van Nieuwerburgh, S. 2017. Out-of-Town Home Buyers and City Welfare. CEPR Discussion Paper, No. 12283.

Haughwout, A., Lee, D., Tracy, J., van der Klaauw, W. (2011). Real Estate Investors, the Leverage Cycle, and the Housing Market Crisis. Federal Reserve Bank of New York Staff Reports, 514.

Hilber, C.A.L. and O. Schöni. 2018. The Economic Impacts of Constraining Second Home Investments. CEP Discussion Paper No. 1556. (http://cep.lse.ac.uk/pubs/download/dp1556.pdf)

Sá, F. (2016). The Effect of Foreign Investors on Local Housing Markets: Evidence from the UK. Centre for Macroeconomics Discussion Paper, No. 1639.

Suher, M. (2016). Is Anybody Home? The Impact of Taxation of Non-Resident Buyers. NYU Furman Center, mimeo, February.

Global Housing Watch Newsletter: July 2018

In this interview, Christian Hilber explores a recent global phenomenon: the surge of investment in second homes and the subsequent political backlash against wealthy investors. Building on his research, he discusses the causes of the surge, the consequences, and possible cures. Hilber is Professor of Economic Geography at the London School of Economics.

On the causes…

Hites Ahir: As you know,

Posted by at 11:25 PM

Labels: Global Housing Watch

Football’s minnows demonstrate how poor countries can catch up

From a new post by Tim Harford:

“Prof Rodrik has found evidence that unconditional convergence does happen, not for economies as a whole but for specific manufacturing sectors in those economies, such as “macaroni and noodles” or “knitted or crocheted apparel” or “plastic sacks and bags”.

If such a sector is well behind the global cutting edge, it can expect labour productivity to grow by 4-8 per cent a year, enough to double every decade or two. This tendency holds regardless of what else might be happening in the economy. Why?

The likely answer is that such manufacturing sectors get drawn into global supply chains. They can learn quickly, and must do so to respond to the incessant threat of competition. They will be doing business with suppliers and customers who can provide swift feedback and instruction. In the modern global economy, certain kinds of know-how travel fast, small tasks are unbundled, and part-finished goods and components shuttle back and forth across borders. Any enterprise plugged into this process will improve quickly. It may be more closely integrated into global supply chains than its own local economy, which might not keep up.

All of which brings us back to football. Two economists, Melanie Krause and Stefan Szymanski, decided to examine whether the unconditional convergence hypothesis holds for international men’s football, as it does for manufacturing sectors. (Prof Szymanski is the co-author, with the Financial Times’s Simon Kuper, of Soccernomics. (UK) (US)) Football, after all, offers a long data set and some clear measures of performance. International football’s governing body, Fifa, has more members than the UN.

Sure enough, Profs Krause and Szymanski found that the strength of international football teams is converging. The minnows are acquiring bite, and the old cliché, “there are no easy games in international football”, is far truer today than it was in 1950.

Perhaps we should not be surprised. As with manufacturing, the standard of competition is fierce, performance metrics unforgiving, and the very best ideas will be copied. As an additional spur to progress, elite football offers a global labour market: a strong player from a weak national team will spend most of his time at a top club side in the company of world-class dietitians, trainers, and teammates. His home nation will enjoy the benefits.

It is tempting to draw grand conclusions from all this, about the increasing importance of knowledge in globalisation; about the bracing effects of robust international competition; about the benefits of being open to international migrants. But perhaps it is better to just watch the football. In an age of distressing reality-TV politics, here, at least, is a competitive spectacle we can all enjoy.”

Continue reading here.

From a new post by Tim Harford:

“Prof Rodrik has found evidence that unconditional convergence does happen, not for economies as a whole but for specific manufacturing sectors in those economies, such as “macaroni and noodles” or “knitted or crocheted apparel” or “plastic sacks and bags”.

If such a sector is well behind the global cutting edge, it can expect labour productivity to grow by 4-8 per cent a year,

Posted by at 11:00 AM

Labels: Inclusive Growth, Macro Demystified

Friday, July 13, 2018

House Prices in Vietnam

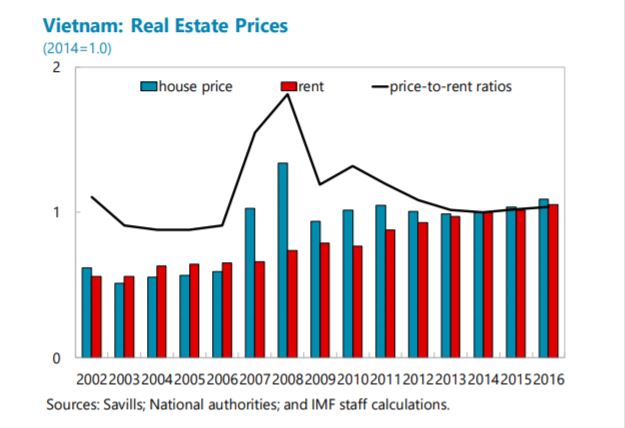

From the IMF’s latest report on Vietnam:

“Real estate prices have rebounded from the lows seen in the GFC but remain well below the

highs of 2008. Price-to-rent ratios suggest that the increase in property prices is in line with growing demand for housing from a rapidly growing urban middle class with rising incomes (…). The availability of affordable housing is also increasing, supported in part by low-interest mortgage lending by SOCBs.”

From the IMF’s latest report on Vietnam:

“Real estate prices have rebounded from the lows seen in the GFC but remain well below the

highs of 2008. Price-to-rent ratios suggest that the increase in property prices is in line with growing demand for housing from a rapidly growing urban middle class with rising incomes (…). The availability of affordable housing is also increasing, supported in part by low-interest mortgage lending by SOCBs.”

Posted by at 8:27 AM

Labels: Global Housing Watch

Subscribe to: Posts