Thursday, June 7, 2018

Snapshots of the Salubrious US Labor Market

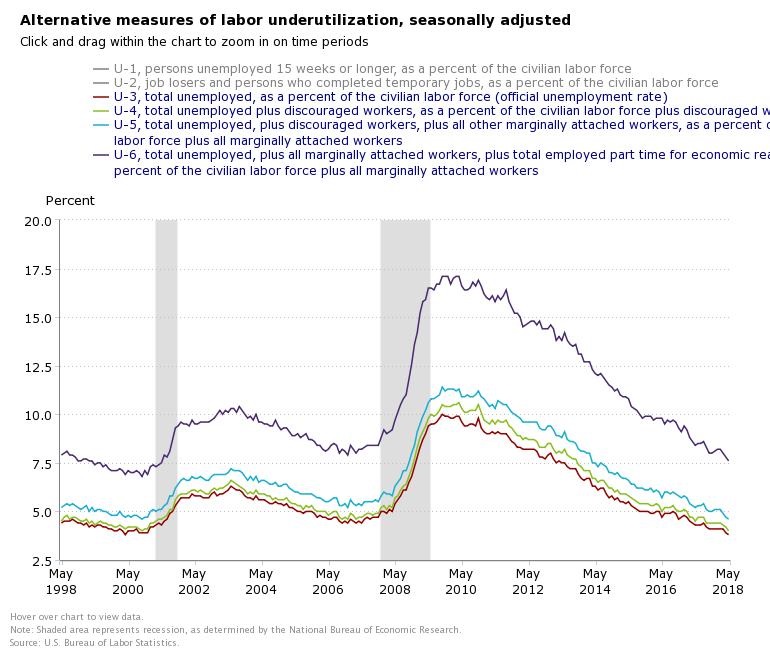

A new post by Timothy Taylor says that “there are a lot of ways to look at unemployment, but whatever measure you choose, the measure is essentially back to what it was before the Great Recession.” “There is no heaven on Earth, and there is no ultimate perfection to be found in real-world labor markets. But the current US labor market situation is really quite good.”

A new post by Timothy Taylor says that “there are a lot of ways to look at unemployment, but whatever measure you choose, the measure is essentially back to what it was before the Great Recession.” “There is no heaven on Earth, and there is no ultimate perfection to be found in real-world labor markets. But the current US labor market situation is really quite good.”

Posted by at 10:18 AM

Labels: Inclusive Growth

Wednesday, June 6, 2018

Housing Market in Romania

The IMF’s latest report on Romania says that:

- “Notwithstanding these improvements, vulnerabilities arise from the high exposure of banks to the real estate sector and sovereign debt. Real estate exposure rose with housing loans increasing from 21 to 54 percent of household loans between 2008 and 2017. These mortgage contracts (mostly at variable rates) expose banks to credit risks in the event of sharp increases in interest rates. The effectiveness of existing macroprudential tools on mortgages is undermined by the Prima Casa program, which allows loan-to-value ratios up to 95 percent. The Romanian banking system has also a large exposure to their own sovereign debt (one of the highest in the EU at around 20 percent of assets in 2017), that could lead to valuation losses in the event of interest rate increases. Finally, despite declining considerably since 2011, about 35 percent of banks’ liabilities and assets remain denominated in foreign exchange (FX), and FX liquidity risks can exist within an environment of ample overall liquidity.”

- “A Debt-Service-to-Income (DSTI) limit on mortgage lending would mitigate risks from the exposure of banks to the real estate sector. An appropriately set DSTI limit can boost borrowers’ resilience and should be imposed on all mortgages, including those made under

the Prima Casa program. In this context, staff welcomed the government’s strategy to gradually scale back the program.”

The IMF’s latest report on Romania says that:

- “Notwithstanding these improvements, vulnerabilities arise from the high exposure of banks to the real estate sector and sovereign debt. Real estate exposure rose with housing loans increasing from 21 to 54 percent of household loans between 2008 and 2017. These mortgage contracts (mostly at variable rates) expose banks to credit risks in the event of sharp increases in interest rates. The effectiveness of existing macroprudential tools on mortgages is undermined by the Prima Casa program,

Posted by at 10:12 PM

Labels: Global Housing Watch

The U.S. Personal Saving Rate

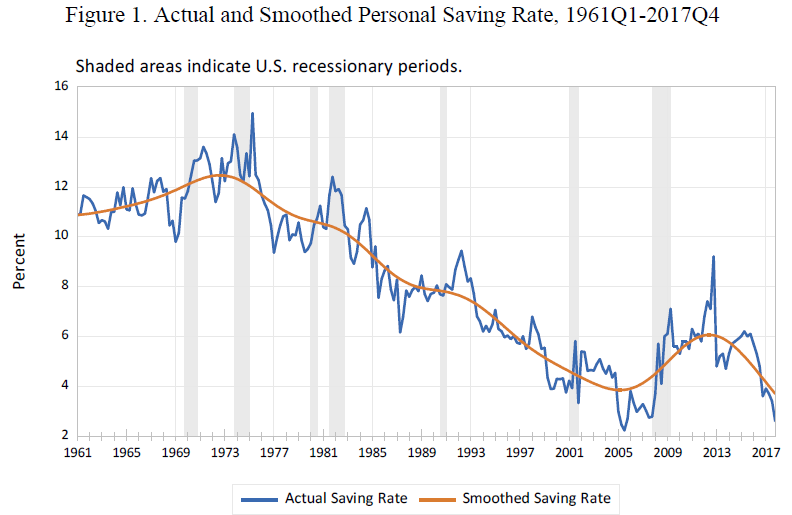

A new IMF paper shows that “Before the crisis, the personal saving rate was trending downwards. However, in 2008 there was a significant rise in the saving rate that continued until the end of 2012, suggesting a permanent change in household behavior. […] the rise in the saving rate during 2008-2012 was caused by the negative shocks to income, employment and wealth. This result explains why the saving rate resumed its decline in 2013, as real disposable income, employment

and net worth recovered. Assuming that the real growth in these determinants remains strong, the estimated model predicts continued negative pressures on the current account deficit and further external imbalances attributable to the U.S. household sector.”

A new IMF paper shows that “Before the crisis, the personal saving rate was trending downwards. However, in 2008 there was a significant rise in the saving rate that continued until the end of 2012, suggesting a permanent change in household behavior. […] the rise in the saving rate during 2008-2012 was caused by the negative shocks to income, employment and wealth. This result explains why the saving rate resumed its decline in 2013, as real disposable income,

Posted by at 1:35 PM

Labels: Inclusive Growth, Macro Demystified

Financial Stability and Inequality: A Challenge for Macroprudential Regulation

From a new post by Pierre Monnin:

“Theoretical analyses and recent empirical evidence support the hypothesis that increasing inequality can pave the way to financial instability. Considering these results, central banks and financial regulators should keep a close watch on income and wealth distributions in their countries. They should be particularly attentive to a simultaneous rise in inequality and aggregate debt. They might also consider including inequality in their sets of early warning indicators for financial crises.”

“Central banks and financial regulators should also carefully consider the potential feedback loops between their macroprudential policy, inequality and financial stability. Some measures aimed at strengthening financial stability might increase inequality, and thus impede their initial goals. In such a case, central banks and financial regulators, perhaps in collaboration with fiscal authorities, could consider accompanying measures to mitigate the impact of macroprudential measures on inequality. When facing the choice between two policies with the same impact on financial stability, they should prefer the option that does not lead to higher inequality (or increases it the least) to avoid or reduce the side effects of higher inequality on financial stability. Finally, in accordance with their mandate regarding financial stability, central banks and financial regulators may have some reasons to support policies, e.g. fiscal policies, that mitigate the impact of inequality on financial stability.”

From a new post by Pierre Monnin:

“Theoretical analyses and recent empirical evidence support the hypothesis that increasing inequality can pave the way to financial instability. Considering these results, central banks and financial regulators should keep a close watch on income and wealth distributions in their countries. They should be particularly attentive to a simultaneous rise in inequality and aggregate debt. They might also consider including inequality in their sets of early warning indicators for financial crises.”

Posted by at 1:32 PM

Labels: Inclusive Growth

Tuesday, June 5, 2018

Inequality in China – Trends, Drivers and Policy Remedies

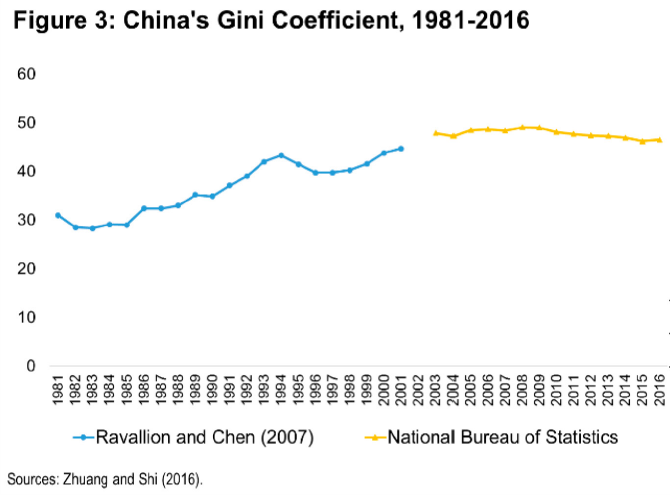

From a new IMF working paper:

“China has experienced rapid economic growth over the past two decades and is on the brink of eradicating poverty. However, income inequality increased sharply from the early 1980s and rendered China among the most unequal countries in the world. This trend has started to reverse as China has experienced a modest decline in inequality since 2008. This paper identifies various drivers behind these trends – including structural changes such as urbanization and aging and, more recently, policy initiatives to combat it. It finds that policies will need to play an important role in curbing inequality in the future, as projected structural trends will put further strain on equity considerations. In particular, fiscal policy reforms have the potential to enhance inclusiveness and equity, both on the tax and expenditure side.”

From a new IMF working paper:

“China has experienced rapid economic growth over the past two decades and is on the brink of eradicating poverty. However, income inequality increased sharply from the early 1980s and rendered China among the most unequal countries in the world. This trend has started to reverse as China has experienced a modest decline in inequality since 2008. This paper identifies various drivers behind these trends – including structural changes such as urbanization and aging and,

Posted by at 5:28 PM

Labels: Inclusive Growth

Subscribe to: Posts