Tuesday, March 6, 2018

IMF Paper Looks at How Inflation Anchoring Affects Growth

My new paper with Sangyup Choi and Davide Furceri has been featured the Central Banking:

“A working paper published by the International Monetary Fund has concluded anchoring inflation expectations – rather than the level of inflation – is what has a statistical effect on growth.

In their paper, Sangyup Choi, Davide Furceri, and Prakash Loungani explore whether low inflation and the anchoring of inflation expectations are positive for economic growth, as central bankers often assert.

While they find inflation anchoring fosters growth in industries that are more credit-constrained, the authors also attempt to “disentangle” the effect of inflation anchoring from the effect of the level of inflation.

Using data on sectoral growth for 36 advanced and emerging market economies from 1990–2014, the authors “explicitly” control for interactions between “the level of inflation and industry-specific measures of credit constraints”.

“While these two channels tend to be correlated, since low inflation is often achieved by better inflation anchoring … the results of the analysis suggest that it is inflation anchoring and not the level of inflation per se that has a statistical effect on growth,” they say.”

My new paper with Sangyup Choi and Davide Furceri has been featured the Central Banking:

“A working paper published by the International Monetary Fund has concluded anchoring inflation expectations – rather than the level of inflation – is what has a statistical effect on growth.

In their paper, Sangyup Choi, Davide Furceri, and Prakash Loungani explore whether low inflation and the anchoring of inflation expectations are positive for economic growth,

Posted by at 8:57 AM

Labels: Inclusive Growth

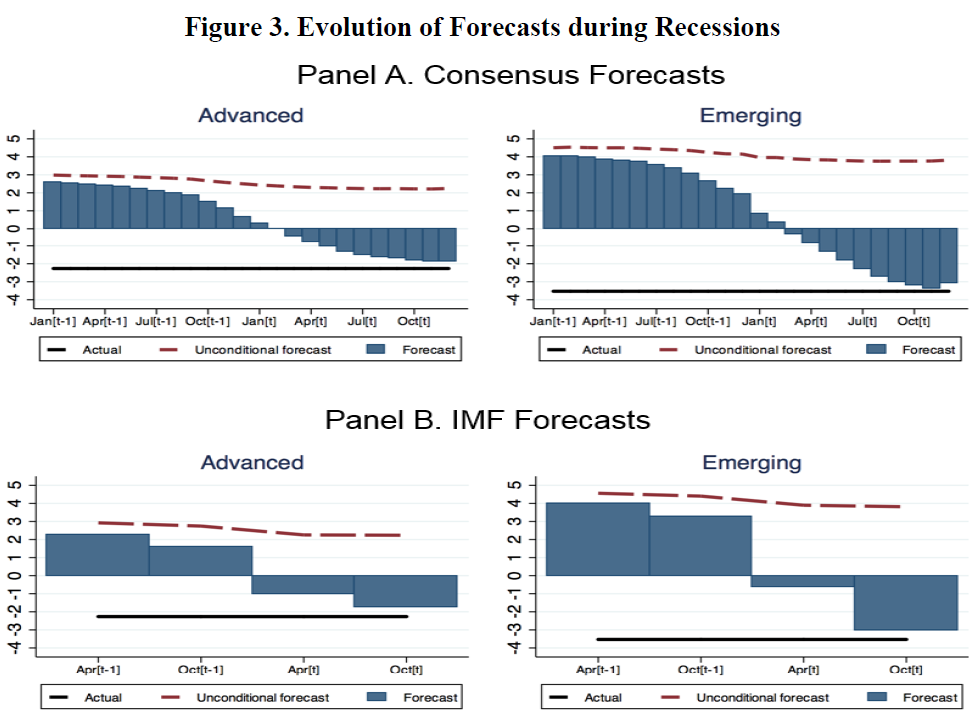

How Well Do Economists Forecast Recessions?

In my latest IMF working paper with Zidong An and Joao Jalles, “We describe the evolution of forecasts in the run-up to recessions. The GDP forecasts cover 63 countries for the years 1992 to 2014. The main finding is that, while forecasters are generally aware that recession years will be different from other years, they miss the magnitude of the recession by a wide margin until the year is almost over. Forecasts during non-recession years are revised slowly; in recession years, the pace of revision picks up but not sufficiently to avoid large forecast errors. Our second finding is that forecasts of the private sector and the official sector are virtually identical; thus, both are equally good at missing recessions. Strong booms are also missed, providing suggestive evidence for Nordhaus’ (1987) view that behavioral factors—the reluctance to absorb either good or bad news—play a role in the evolution of forecasts.”

In my latest IMF working paper with Zidong An and Joao Jalles, “We describe the evolution of forecasts in the run-up to recessions. The GDP forecasts cover 63 countries for the years 1992 to 2014. The main finding is that, while forecasters are generally aware that recession years will be different from other years, they miss the magnitude of the recession by a wide margin until the year is almost over.

Posted by at 8:38 AM

Labels: Forecasting Forum

Monday, March 5, 2018

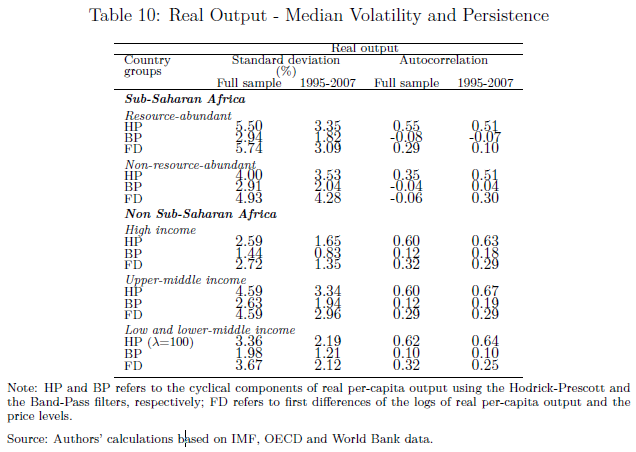

Economic Fluctuations in Sub-Saharan Africa

From a new IMF Working Paper:

“We compare business cycle fluctuations in Sub-Saharan African (SSA) countries vis-à-vis the rest of the world. Our main results are as follows: (i) African economies stand out by their macroeconomic volatility, which is is reflected in the volatility of output and other macro variables; (ii) inflation and output tend to be negatively correlated; (iii) unlike advanced economies and emerging markets (EMs), trade balances and current accounts are acyclical in SSA; (iv) the volatility of consumption and investment relative to GDP is larger than in other countries; (v) the cyclicality of consumption and investment is smaller than in advanced economies and EMs; (vi) there is little comovement between consumption and investment; (vii) consumption and investment are strongly positively correlated with imports.”

Continue reading here.

From a new IMF Working Paper:

“We compare business cycle fluctuations in Sub-Saharan African (SSA) countries vis-à-vis the rest of the world. Our main results are as follows: (i) African economies stand out by their macroeconomic volatility, which is is reflected in the volatility of output and other macro variables; (ii) inflation and output tend to be negatively correlated; (iii) unlike advanced economies and emerging markets (EMs), trade balances and current accounts are acyclical in SSA;

Posted by at 5:30 PM

Labels: Inclusive Growth

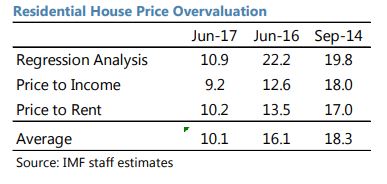

House Prices in Namibia

The IMF’s latest report on Namibia says that:

“Recently decelerating house prices and banks’ and households’ large exposure to mortgage loans raise concerns about risks from sudden corrections in the housing market. Staff estimate that, with the economy decelerating, house prices remain on average overvalued by about 10 percent, down from about 18 percent three years ago. FSAP sensitivity analysis suggests that all banks are resilient to a full correction in house price overvaluation. However, in the case of an over-correction (e.g., 20 percent price decline), some banks would be unable to comply with capital requirements. Under these scenarios, banks would deleverage with negative effects on credit and growth.”

The IMF’s latest report on Namibia says that:

“Recently decelerating house prices and banks’ and households’ large exposure to mortgage loans raise concerns about risks from sudden corrections in the housing market. Staff estimate that, with the economy decelerating, house prices remain on average overvalued by about 10 percent, down from about 18 percent three years ago. FSAP sensitivity analysis suggests that all banks are resilient to a full correction in house price overvaluation.

Posted by at 10:53 AM

Labels: Global Housing Watch

Saturday, March 3, 2018

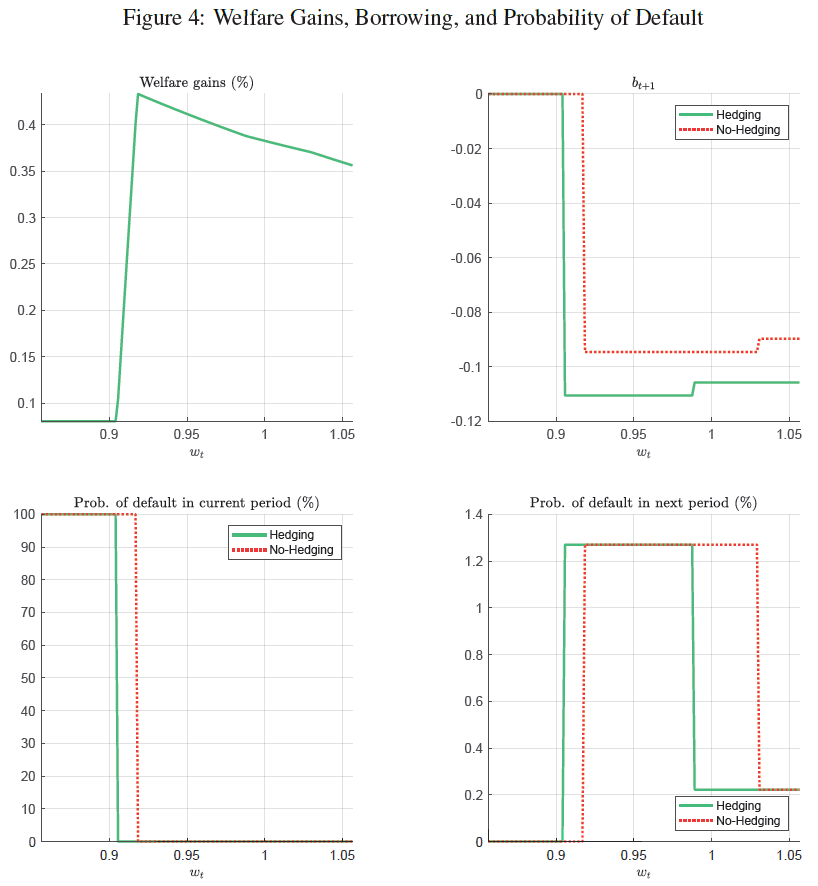

Welfare Gains from Market Insurance: The Case of Mexican Oil Price Risk

From a new IMF working paper:

“Over the past two decades, Mexico has hedged oil price risk through the purchase of put options. We examine the resulting welfare gains using a standard sovereign default model calibrated to Mexican data. We show that hedging increases welfare by reducing income volatility and reducing risk spreads on sovereign debt. We find welfare gains equivalent to a permanent increase in consumption of 0.44 percent with 90 percent of these gains stemming from lower risk spreads.”

From a new IMF working paper:

“Over the past two decades, Mexico has hedged oil price risk through the purchase of put options. We examine the resulting welfare gains using a standard sovereign default model calibrated to Mexican data. We show that hedging increases welfare by reducing income volatility and reducing risk spreads on sovereign debt. We find welfare gains equivalent to a permanent increase in consumption of 0.44 percent with 90 percent of these gains stemming from lower risk spreads.”

Posted by at 9:13 AM

Labels: Energy & Climate Change, Inclusive Growth

Subscribe to: Posts