Friday, November 24, 2017

Housing View – November 24, 2017

On cross-country:

- A quarter of household expenditure allocated to housing – Eurostat

- The Problem With Expensive Real Estate – Bloomberg

- Capacity Building & Disseminating best practices in affordable housing – Housing Europe

On the US:

- More reactions to House Tax Reform Bill – Curbed, Foreign Affairs, NAHB, Politico, Seattle Times

- A duopsony built around rent-seeking – American Enterprise Institute

- After a Natural Disaster, Do Landlords Jack Up the Rent? – Priceonomics

- Why Does Land-Use Regulation (Still) Matter in Oregon? – Cato Institute

- House and Senate Tax Plans Cut Affordable Housing, Set Stage for Deeper Cuts Later – Center on Budget and Policy Priorities

- The Mortgage Credit Channel of Macroeconomic Transmission – MIT

- What the Housing Market in America Needs Is More Options – Smithsonian

On other countries:

- [Australia] Speech on Mortgage Insights From Securitisation Data – Reserve Bank of Australia

- [Australia] Regional housing supply and demand in Australia – Australian National University

- [Brazil] Loan-to-value policy and housing finance: effects on constrained borrowers – Bank for International Settlements

- [Canada] Even Real Estate Developers Can’t Afford Toronto’s Housing Market – Bloomberg

- [China] China to step up property market regulation to avoid bubble risk – Reuters

- [Japan] Is Tokyo’s property market reaching its peak? – Financial Times

- [Romania] Housing privatization in Romania – Economics of Transition

- [Sweden] Slowdown in Swedish house prices is ‘positive’ for stability – Riksbank – Financial Times

- [Sweden] Riksbank Governor Tries to Quell Fears of Swedish Housing Slump – Bloomberg

- [Switzerland] Zurich’s Public Housing Problem: The Tenants Are Too Rich – Citylab

- [Switzerland] Lessons from Zurich – Inside Housing

- [United Kingdom] Your regular reminder that stamp duty cuts make nearly no difference to anything – Financial Times

- [United Kingdom] 2017 Autumn Statement Response – Cluttons

On cross-country:

- A quarter of household expenditure allocated to housing – Eurostat

- The Problem With Expensive Real Estate – Bloomberg

- Capacity Building & Disseminating best practices in affordable housing – Housing Europe

On the US:

- More reactions to House Tax Reform Bill – Curbed, Foreign Affairs, NAHB,

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, November 22, 2017

House Prices in Philippines

The IMF’s latest report on Philippines says that “However, credit growth has accelerated from 13.6 percent in 2015 to 19.7 percent in July 2017, led by consumer credit and real estate loans. Although most indicators show no evidence of a credit boom so far, property prices have stabilized, and lending standards have not deteriorated, some indicators suggest that, under current trends, credit gaps could approach early warning levels of credit booms in 2017−18 (…)”.

The IMF’s latest report on Philippines says that “However, credit growth has accelerated from 13.6 percent in 2015 to 19.7 percent in July 2017, led by consumer credit and real estate loans. Although most indicators show no evidence of a credit boom so far, property prices have stabilized, and lending standards have not deteriorated, some indicators suggest that, under current trends, credit gaps could approach early warning levels of credit booms in 2017−18 (…)”.

Posted by at 3:04 PM

Labels: Global Housing Watch

Tuesday, November 21, 2017

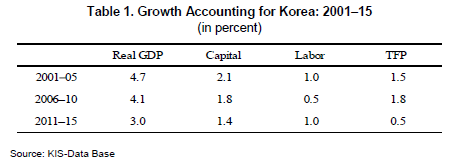

Korea’s Paradigm Shift for Sustainable and Inclusive Growth: A Proposal

From a new IMF working paper:

“Korea is facing mounting economic challenges. Productivity growth has been on a trend decline amid demographic headwinds, while the societal demand for inclusive growth has been on a steep rise. Furthermore, the government-led unbalanced growth model—which served Korea well in the past—has become less effective and politically palatable in recent years. As such, Korea needs a major paradigm shift to embark on a new sustainable and inclusive growth path. But policy response has been modest at best with no major reforms being implemented over the past two decades. We propose a paradigm shift in Korea’s economic framework, involving a simultaneous big push for greater economic freedom and stronger social protection within the parameters set by long-run fiscal sustainability. We also provide a detailed account of structural reforms to boost economic freedom and sustainable funding plans for stronger social protection.”

From a new IMF working paper:

“Korea is facing mounting economic challenges. Productivity growth has been on a trend decline amid demographic headwinds, while the societal demand for inclusive growth has been on a steep rise. Furthermore, the government-led unbalanced growth model—which served Korea well in the past—has become less effective and politically palatable in recent years. As such, Korea needs a major paradigm shift to embark on a new sustainable and inclusive growth path.

Posted by at 4:50 PM

Labels: Inclusive Growth

Mexico’s Structural Reform Agenda”: Early Signs of Success”

A new IMF country report finds:

“The implementation of the Pacto por México has already led to important transformations in the Mexican economy. While initial estimates of potential growth payoffs may have been optimistic, external headwinds have masked important signals that the reforms are working. From a macroeconomic perspective, the reforms have already contributed to increasing investment, falling prices and more widespread access to services.

The reforms will take more time to fully feed through to the broader macro economy and lift growth. The delayed impact of the reforms owes to their complexity as well as some important short-term costs. At the same time, weaknesses in the rule of law will have weakened their impacts. Nevertheless, the transformations have highlighted the positive synergies associated with a broad approach to structural reform that exploits complementarities between different sectors.

Building on existing reforms will be key, and priority should be given to reforms targeting the rule of law. Continued weaknesses related to informality, corruption and crime would stifle private investment and would likely impede the broader reform effort from exerting its full impact on the economy. Improving the efficiency and quality of law enforcement and judicial institutions would be critical in this regard.”

A new IMF country report finds:

“The implementation of the Pacto por México has already led to important transformations in the Mexican economy. While initial estimates of potential growth payoffs may have been optimistic, external headwinds have masked important signals that the reforms are working. From a macroeconomic perspective, the reforms have already contributed to increasing investment, falling prices and more widespread access to services.

The reforms will take more time to fully feed through to the broader macro economy and lift growth.

Posted by at 3:17 PM

Labels: Inclusive Growth

Monday, November 20, 2017

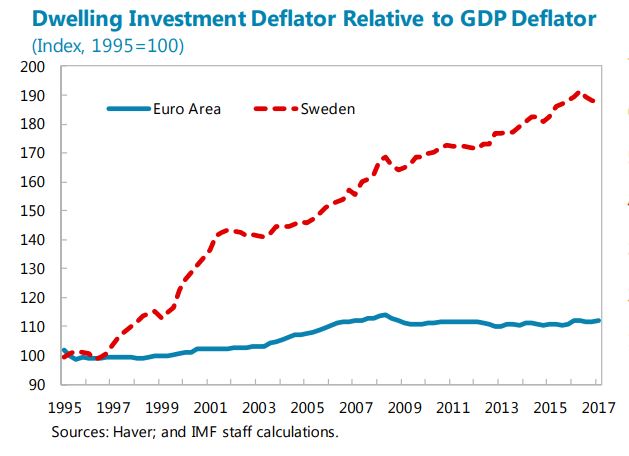

Housing in Sweden

From IMF’s latest report on Sweden:

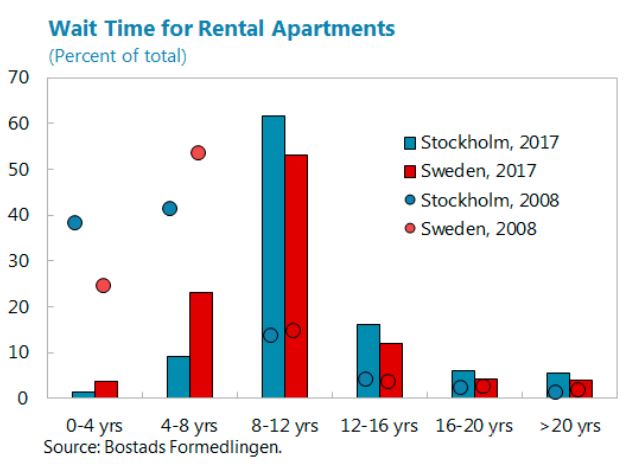

“The Swedish housing market has deep structural problems. Large house price increases were necessary to overcome the hurdle of high construction costs before construction began rising. These costs reflect a combination of complex building regulations and limited competition in the sector owing to cumbersome municipal land sale and planning and approval procedures. The resulting supply shortfalls are present in 255 out of 290 municipalities, but are mostly in the three major metropolitan areas (Stockholm, Gothenburg, and Malmo) owing to ongoing urbanization. Moreover, strict rent controls have resulted in a declining supply of rental apartments as they are converted into tenant-owned condominiums and as existing renters are “locked-in”. The resulting long waiting times for rental apartments leave many households with no option but to purchase housing, which is incentivized by the tax deductibility of mortgage interest payments.”

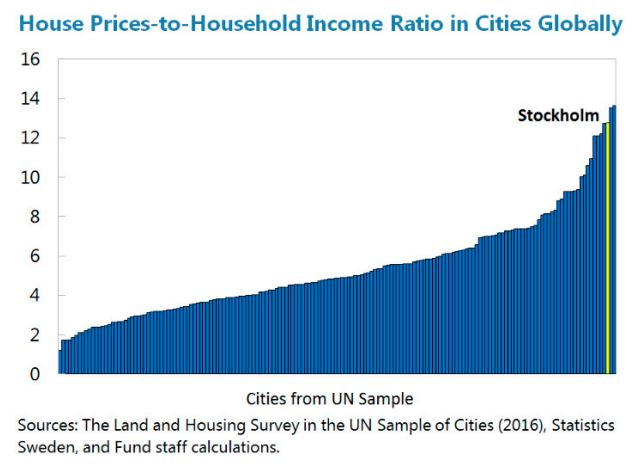

“Low housing affordability undermines financial stability, growth, and equality. Home costs relative to median household income have more than doubled since the mid-1990s (…). In Stockholm, the price-to-income ratio is nearly twice the national average and is among the highest worldwide. These factors reduce labor mobility, especially for those from outside the main centers, hindering inclusive growth. Equity is further undermined by overcrowding among low-income groups and the need to rely on parental savings for housing purchases. Households must borrow more at higher house prices, lifting household debt to 182 percent of disposable income (…), with new purchasers taking on debts averaging 402 percent of their disposable income.”

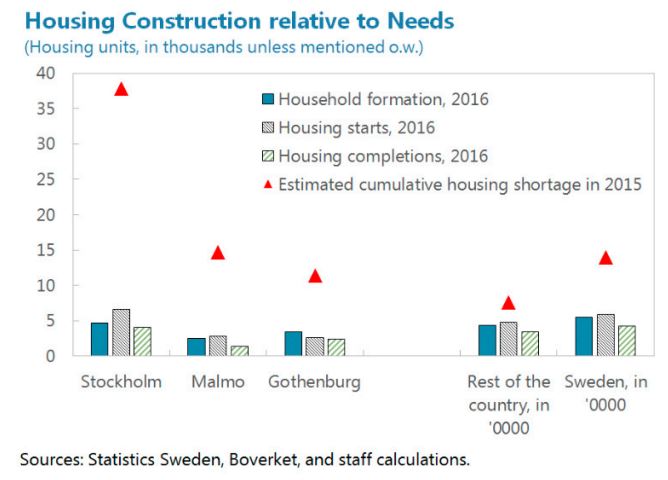

“Policies to bolster construction are welcome yet are unlikely to be sufficient to rebalance the housing market. The government targets building 250,000 dwellings during 2015– 20, including by subsidizing (0.1 percent of GDP) construction of affordable rental housing—which meets energy efficiency and rent limit requirements—and through state financing to municipalities for infrastructure related to housing development. Although construction has risen (…), housing starts only modestly exceed estimated household formation in most of the country, indicating that shortages will persist. Moreover, due to high land prices and construction costs, new development has been focused on the high-end of the market or located in more remote areas.”

“Improving housing affordability should be a central priority, supported by deep structural reforms to promote more efficient use of existing property:

- Sustaining housing supply. High construction costs in Sweden need to be addressed by streamlining building regulations and promoting competition in the sector, including by harmonizing fragmented planning and approval processes. Improving public transportation within regions would help relieve demand pressures in major centers. Budgetary support for construction of rental housing that meets affordability tests should be expanded.

- Phasing out rent control. Providing incentives to better match housing to household needs will effectively increase supply in areas with high demand. All new construction of rental apartments should be fully exempt from controls. Rents on apartments under control should be steadily aligned with market rates, with low-income households protected by the housing allowance.

- Addressing tax incentives. To promote efficient use of space, the composition of property taxes should be shifted by cutting capital gains taxes that deter sales while raising the recurrent property tax, which in 2008 was capped at a level among the lowest in OECD. If the property tax cannot be raised, it becomes more critical to reduce mortgage interest deductibility to ease demand and discourage high leverage. The macroeconomic impact would be modest while interest rates are low and such reforms could be part of a package that benefits households.”

“Authorities’ Views. The authorities recognize the structural challenges in the Swedish housing market, as reflected in the appointment of committees to review the planning and building regulations as well as the model for setting rents on newly produced rental housing. The authorities also recognize the need for further measures to reduce incentives for over-indebtedness. Political opposition to property tax is strong as it is considered to be unfair, and while a lower capital gains tax could improve property turnover, it could have distributional effects favoring older households that had often accumulated significant wealth. The government’s view is that a reduction in mortgage interest deductibility is more feasible if broad political consensus can be reached. With rents on newly-produced rental properties being very high, the government is concerned that a transition to market-based rents would bring high rents, and it also has doubts that the supply of rental housing within the reach of lower income households would increase significantly. The Riksbank, on the other hand, stresses that a more market-based rent system would increase supply, benefitting young people.”

From IMF’s latest report on Sweden:

“The Swedish housing market has deep structural problems. Large house price increases were necessary to overcome the hurdle of high construction costs before construction began rising. These costs reflect a combination of complex building regulations and limited competition in the sector owing to cumbersome municipal land sale and planning and approval procedures. The resulting supply shortfalls are present in 255 out of 290 municipalities, but are mostly in the three major metropolitan areas (Stockholm,

Posted by at 1:29 PM

Labels: Global Housing Watch

Subscribe to: Posts