Wednesday, February 22, 2017

Housing Market in Malta

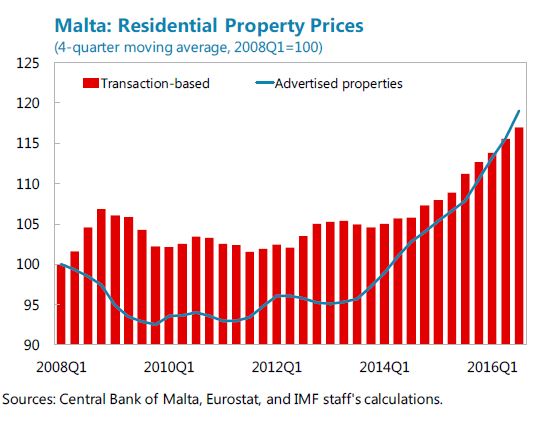

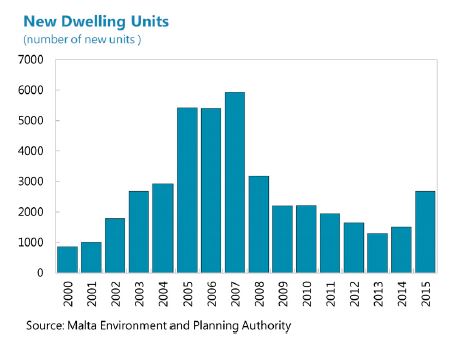

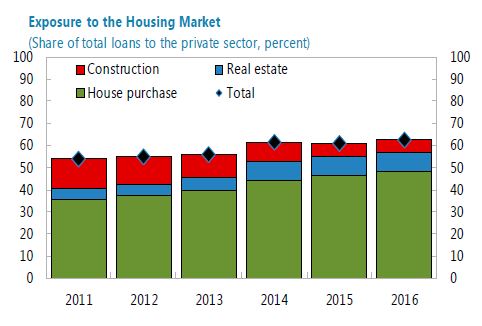

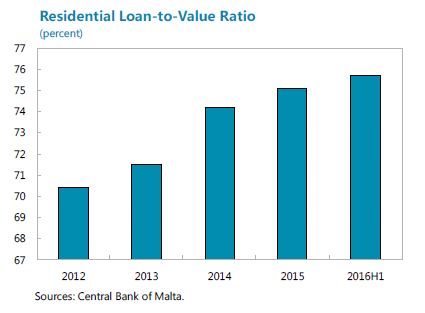

A new IMF paper “(…) assesses vulnerabilities and risks associated with the property market in Malta. The data do not appear to point to a house price misalignment at present, yet a combination of demand and supply factors are likely to exert sustained pressures on house prices going forward. Moreover, elevated households’ indebtedness, combined with high and increasing bank exposure to property market, pose vulnerabilities to a potential negative house price shock. This calls for: (i) deploying targeted macro prudential tools as precautionary measures and maintaining prudent lending standards; (ii) closing data gaps to calibrate such tools and ensure continued in-depth monitoring of risks, (iii) carefully reviewing fiscal incentives related to property market; and (iv) alleviating financing constraints in construction sector to enhance supply response to price signals.”

A new IMF paper “(…) assesses vulnerabilities and risks associated with the property market in Malta. The data do not appear to point to a house price misalignment at present, yet a combination of demand and supply factors are likely to exert sustained pressures on house prices going forward. Moreover, elevated households’ indebtedness, combined with high and increasing bank exposure to property market, pose vulnerabilities to a potential negative house price shock. This calls for: (i) deploying targeted macro prudential tools as precautionary measures and maintaining prudent lending standards;

Posted by at 10:39 AM

Labels: Global Housing Watch

Wednesday, February 15, 2017

House Prices in Macao (SAR)

The IMF’s new report on Macao SAR says that:

“Risks in the housing market appear broadly contained. Housing in Macao SAR experienced a remarkable boom: between end 2008 and mid-2014, prices rose by over 500 percent (nearly 400 percent in real terms). To some degree, this asset appreciation can be explained by fundamentals including rising real wages, financial deepening, and population growth amid a relatively fixed supply of land. In the period since mid-2014, prices have partially corrected, falling by over 30 percent, and are back at 2013 levels. However, only 0.1 percent of residential mortgage loans have negative equity (and nonperforming loans are roughly the same magnitude).2 This strength in asset quality likely owes to three factors. First, for most homeowners, prices are still above the purchase price given the size of the initial boom and the short period of the recent correction. Second, the average loan to value remains well below regulatory maxima. And third, average debt service to income has been consistently low at 25 percent. According to the most recent data, real estate prices and transactions have started to increase again, suggesting that the correction may have bottomed.

In light of these dynamics, the current macroprudential stance appears appropriate. An easing of macro prudential standards would be an appropriate response in the event of a rapid and self-reinforcing decline in housing prices that posed risks to financial stability and the broader economy.3 Current indications suggest, however, that existing standards remain appropriate, including the loan-to-value ratio and debt service-to-income ratio applied in Macao SAR. While house prices have fallen, the adjustment has been orderly and the market appears to be stabilizing without any significant stress on balance sheets or financial stability.

Current public concerns about housing affordability are best addressed through other means. To the degree there are social goals of improving the accessibility of housing, fueling demand via loosening macroprudential regulations amid tight supply may increase the price more than improve affordability. Instead, it would be more effective to provide targeted (means-tested) transfers and ensure that regulatory policy is adequate to support further private sector supply at market (rather than subsidized) prices. In this regard, efficient execution of housing plans for reclaimed land and welltargeted public housing supply will be important. Nonetheless, if the impact of speculative demand on real estate prices is a material concern, the authorities could consider more targeted macroprudential measures such as tighter loan-to-value ratios on second-home purchases.“

The IMF’s new report on Macao SAR says that:

“Risks in the housing market appear broadly contained. Housing in Macao SAR experienced a remarkable boom: between end 2008 and mid-2014, prices rose by over 500 percent (nearly 400 percent in real terms). To some degree, this asset appreciation can be explained by fundamentals including rising real wages, financial deepening, and population growth amid a relatively fixed supply of land. In the period since mid-2014,

Posted by at 10:44 AM

Labels: Global Housing Watch

Friday, February 10, 2017

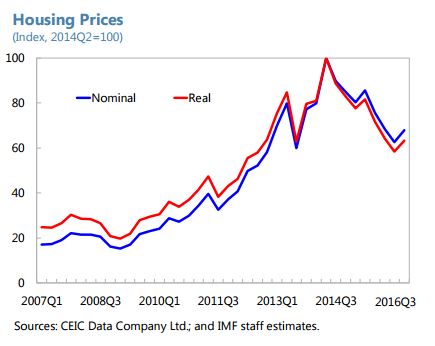

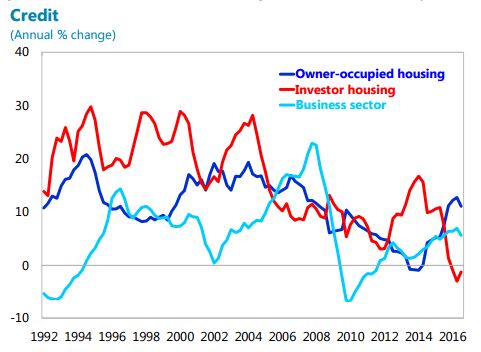

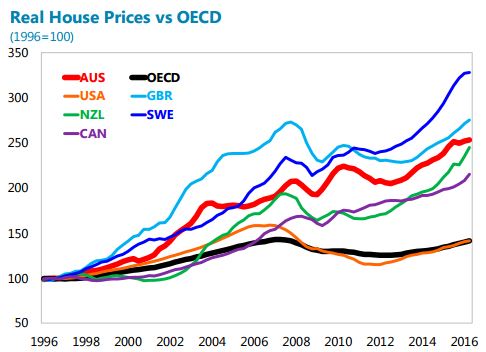

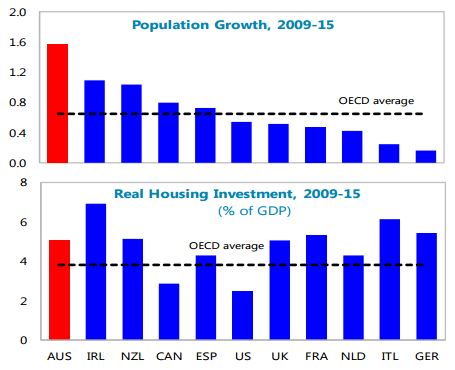

House Prices in Australia

The IMF’s annual report on Australia points out that:

“By some metrics, housing market conditions have cooled and credit growth to households has slowed, but risks related to house price and debt levels have not yet decreased.

Real house price gains have moderated. Indicators of current conditions such as sales volumes and the rate of turnover in the housing stock have moderated. The extent of cooling has varied considerably across capital cities. The strongest price increases continue to be recorded in Sydney and Melbourne, where underlying demand for housing remains strong. With house prices still rising ahead of income, standard valuation metrics suggest somewhat higher house price overvaluation relative to the assessment in 2015 Article IV consultation.

The flipside has been slowing growth in bank lending to households. APRA prudential guidance requiring tighter lending standards by banks, which was introduced in late 2014, has curtailed growth in riskier mortgage loans in particular and credit growth to household more broadly. At the same time, there has been some upward pressures on mortgage rates, as banks have increased capital ratios and prepared for a higher risk weight on mortgage lending. That said, household credit gaps have not yet reversed.

On the supply side, residential investment has risen to some 0.5 percent of GDP above its long term average (the ratio remains comparatively low given population and labor force growth). An above-average number of new apartments is expected to come on stream in the next year or so, mostly in the downtown areas of Brisbane, Melbourne, and, to a lesser extent, Sydney. Concerns about temporary oversupply have thus risen. But leading indicators, such as approvals of new houses and other dwellings or new residential construction starts, have started to level off after brisk increases in 2014-15. In commercial real estate, property price valuations have increased but are still within the usual range of variation over the cycle (..).“

The IMF’s annual report on Australia points out that:

“By some metrics, housing market conditions have cooled and credit growth to households has slowed, but risks related to house price and debt levels have not yet decreased.

Real house price gains have moderated. Indicators of current conditions such as sales volumes and the rate of turnover in the housing stock have moderated. The extent of cooling has varied considerably across capital cities.

Posted by at 12:46 PM

Labels: Global Housing Watch

Tuesday, February 7, 2017

Okun’s Law: Fit at 50?–Revised Paper and Dataset

Here is a revised version of my paper with Larry Ball and Daniel Leigh and the dataset and programs needed to reproduce the results.

Here is a revised version of my paper with Larry Ball and Daniel Leigh and the dataset and programs needed to reproduce the results.

Posted by at 10:03 AM

Labels: Inclusive Growth

Monday, February 6, 2017

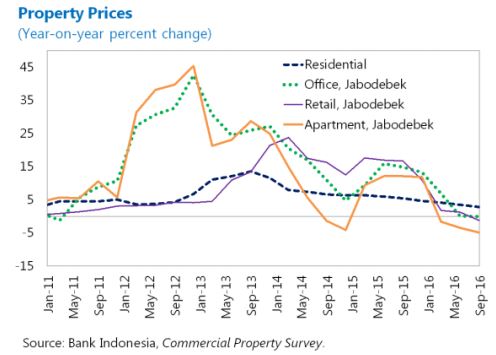

House Prices in Indonesia

“Property prices have been subdued, in tandem with slowing economic growth”, notes IMF’s report on Indonesia.

“Property prices have been subdued, in tandem with slowing economic growth”, notes IMF’s report on Indonesia.

Posted by at 4:10 PM

Labels: Global Housing Watch

Subscribe to: Posts