Monday, March 6, 2017

Global House Prices: An Update

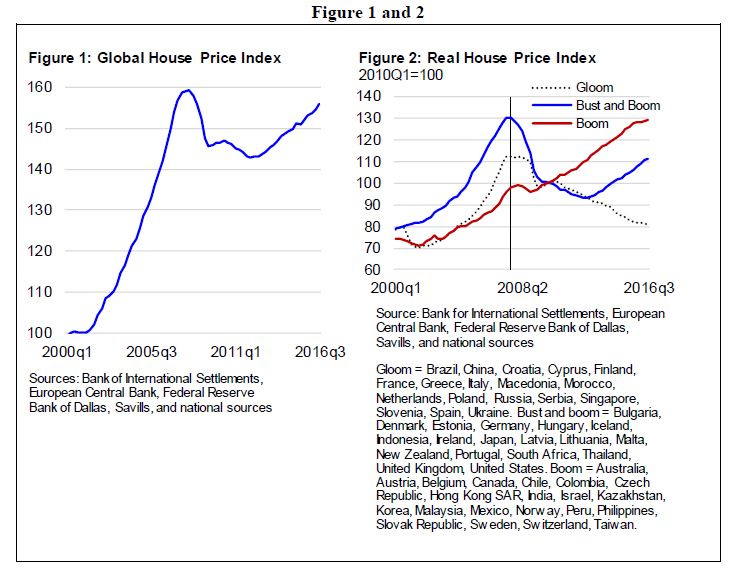

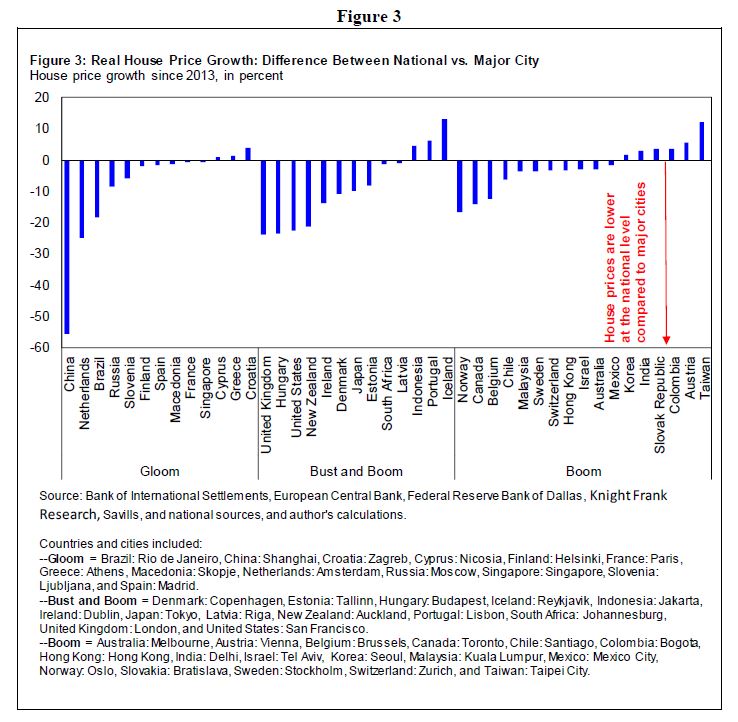

The IMF’s Global House Price Index—an average of real house prices across countries—continued to climb up in the third quarter of 2016 (Figure 1). This is the sixteenth consecutive quarter of positive year-on-year growth in the index. However, house prices are not rising everywhere around the world. As noted in our Q4 2016 Quarterly Update (and as covered in the Wall Street Journal), house price developments in the countries that make up the index fall into three clusters: gloom, bust and boom, and boom (Figure 2).

The Q1 2017 Quarterly Update digs a little deeper and shows that house prices are also not climbing up everywhere within countries. Figure 3 shows that in many countries, house prices are subdued at the national level compared to the city level.

Recent IMF assessments provide a more nuanced view of the within country house price developments.

- On Australia, IMF assessment points out that house price gains have moderated. However, the extent of cooling has varied considerably across cities. The strongest price increases continue to be recorded in Sydney and Melbourne, where underlying demand for housing remains strong. With house prices still rising ahead of income, standard valuation metrics suggest somewhat higher house price overvaluation relative to the previous IMF assessment.

- On Austria, IMF assessment notes that the cumulative increase in the house price index over 2007–2015 was nearly 40 percent. To a large extent, this increase was driven by price dynamics in Vienna. The OeNB residential price index indicator, which assesses whether prices move in line with fundamental factors, points to an overvaluation of property prices of about 22 percent for Vienna, while prices in the rest of the country appear broadly in line with fundamentals.

- On Turkey, IMF assessment points out that the housing market exhibits significant variations across cities. Regional variations have been further accentuated by the presence of more than 2.7 million Syrian refugees since March 2011. Cities near the Syrian border, which have absorbed larger masses of Syrian refugees have seen significant rises in local housing prices since 2011, though they have moderated in recent years.

The IMF’s Global House Price Index—an average of real house prices across countries—continued to climb up in the third quarter of 2016 (Figure 1). This is the sixteenth consecutive quarter of positive year-on-year growth in the index. However, house prices are not rising everywhere around the world. As noted in our Q4 2016 Quarterly Update (and as covered in the Wall Street Journal), house price developments in the countries that make up the index fall into three clusters: gloom,

Posted by at 9:20 PM

Labels: Global Housing Watch

Thursday, March 2, 2017

Creative Financing for Affordable Housing

From Shaping the Future of Construction: Insights to redesign the industry

by Richard Koss

“Overview

Attracting private capital into programmes for affordable housing has been a long-run challenge in both developed and developing countries. In general, the problem is that purely private capital is incentivized to devote its resources towards the development of high-end properties for upper-income households.

Purely public forms of capital can be brought to bear to support affordable housing construction, but cost control can be a problem without the profit incentive. In addition, public resources are limited, in particular in emerging markets, and can fall far short of the public need. What we see then is the development of many forms of public regulation and partnerships with the private sector in order to meet the affordable housing challenge. While still in early changes, a great deal of institutional and technological innovation is just now being brought to bear on this issue that offers considerable promise in this area, particularly in emerging markets.

Regulation and government-sponsored enterprises

Traditionally, higher-income countries have dealt with the issue of affordable housing via a variety of regulations on financial institutions and public support of income targeted at housing. In terms of regulation, the idea is that financial institutions, notably banks, receive public support through features such as cheap funding through taxpayer-insured deposits. In exchange they should be directed to allocate capital towards affordable housing projects that are expected to be profitable, but not so much as the development of costlier units. In the United States, one such mechanism is the Community Reinvestment Act.

Another approach is the formation of government agencies or government-sponsored enterprises (GSE’s) which support liquidity and affordability to loans directed at lower income homeowners and to developers who build high-quality rental units aimed at lower-income communities. They do so in part by designating balance sheet directly towards these mortgages. In addition, they also set standards and share risk with the private sector through the issuance of mortgage-related securities (MRS). In the US these entities include agencies such as the Federal Housing Agency and the Veterans Administration as well as the housing GSEs Fannie Mae and Freddie Mac. GSEs are tasked to support lower-income housing through sweeping regulation known as the Affordable Housing Goals and the Duties to Serve. Other nations have housing agencies, notably Japan and Canada.

The UK has an innovative programme called Help-to-Buy that allows lower income households to purchase a share of a home (usually 25% – 75%) and pay rent on the rest.

Another affordability policy is income support for lowerincome housing. In the US there is the Low Income Housing Tax Credit Programme (LIHTC).

Another approach which is more local in nature is the requirement that developers who are given rights to build on a piece of land set aside a certain number of units designated as affordable housing. Such programmes are very popular in California where affordability is particularly problematic.

Financing vehicles

Another set of responses to the affordable housing financing challenge can be characterized as “financing vehicles”. These are generally partnerships between private, philanthropic and public entities that bring the efficiency of private capital to bear with credit enhancements provided by government and charities. In general, the returns to private capital are somewhat less than for purely private projects, but the experience is that many private developers are willing to participate in these programmes out of a sense of civic duty and reputation enhancement. There are many classes of such investments that are targeted at different segments of the market. These include below-market debt funds, private equity vehicles and real estate investment trusts (REITs). The Urban Land Institute provides a useful summary of these efforts.

In many cases, the public funds come from regional entities (generally states in the US). These are known as Housing Finance Agencies (HFA’s). The US Treasury lends support to more distressed local communities through entities known as Community Development Financial Institutions (CDFI’s). All-in-all there are many hundreds of such vehicles and structures, revealing great innovative thinking that can be targeted at particular needs in distinct communities. There are far too many to list here, but an example that has received attention is the JP Morgan Partners in Raising Opportunity (PRO) programme that provides funding to CDFI’s across the country.”

Continue reading here.

From Shaping the Future of Construction: Insights to redesign the industry

by Richard Koss

“Overview

Attracting private capital into programmes for affordable housing has been a long-run challenge in both developed and developing countries. In general, the problem is that purely private capital is incentivized to devote its resources towards the development of high-end properties for upper-income households.

Purely public forms of capital can be brought to bear to support affordable housing construction,

Posted by at 2:58 PM

Labels: Global Housing Watch

Shaping the Future of Construction: Insights to redesign the industry

A new White Paper from the World Economic Forum says that:

“While most other industries have undergone tremendous changes over the past few decades and have reaped the benefits of process, product and service innovations, the construction sector has been hesitant to fully embrace the latest innovation opportunities and its labour productivity has stagnated or even decreased over the last 50 years.

This mediocre track record can be attributed to various internal and external challenges: the persistent fragmentation of the industry, inadequate collaboration between the players, the sector’s difficulty in adopting and adapting to new technologies, the difficulties in recruiting a talented and futureready workforce, and insufficient knowledge transfer from project to project, among others.

In the context of the Forum’s Future of Construction initiative, over the past year six Working Groups comprised of industry leaders, academics and experts met regularly to develop and analyse innovative ideas, their impact, the barriers to implementing solutions and the way forward to overcoming obstacles and implementing modern approaches in the construction and engineering industry.

This white paper presents the outcome of this work in the form of insight articles proposing innovative solutions on how to address the construction sector’s key challenges in the following fundamental challenge areas:

- Project Delivery – Creating certainty of timely delivery and to budget, and generally improving the productivity of the construction sector

- Life cycle Performance – Reducing the life cycle costs of assets and designing for re-use

- Sustainability – Achieving carbon-neutral assets and reducing waste in the course of construction

- Affordability – Creating high-quality, affordable infrastructure and housing

- Disaster Resilience – Making infrastructure and buildings resilient to climate change and natural disasters

- Flexibility, Liveability and Well-being – Creating infrastructure and buildings that improve the well-being of end-users”

A new White Paper from the World Economic Forum says that:

“While most other industries have undergone tremendous changes over the past few decades and have reaped the benefits of process, product and service innovations, the construction sector has been hesitant to fully embrace the latest innovation opportunities and its labour productivity has stagnated or even decreased over the last 50 years.

This mediocre track record can be attributed to various internal and external challenges: the persistent fragmentation of the industry,

Posted by at 2:49 PM

Labels: Global Housing Watch

Wednesday, March 1, 2017

Morocco: Reducing Gender Inequality Can Boost Growth

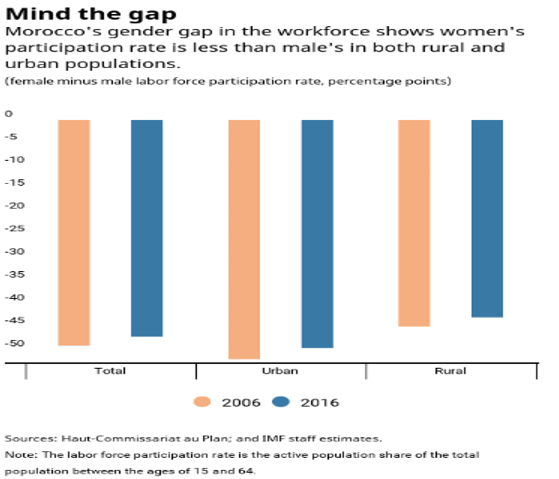

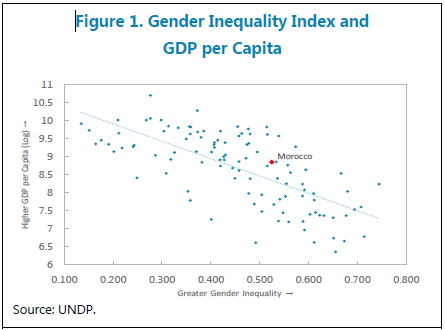

A new IMF report “quantifies the effect of gender inequality in Morocco on growth, compared to groups of faster growing countries. It also estimates income losses due to low female labor force participation. The results highlight that closing overall gender gaps would help Morocco close its GDP per capita gap with benchmark countries in other regions by up to 1 percentage point. Simulations also show that gradually closing gender gaps in the labor force participation rate could lead to significant income gains over the long term. Policy recommendations to promote gender equality include investing in secondary education for women and in infrastructure, and reforming gender-discriminatory tax policies and laws.”

A new IMF report “quantifies the effect of gender inequality in Morocco on growth, compared to groups of faster growing countries. It also estimates income losses due to low female labor force participation. The results highlight that closing overall gender gaps would help Morocco close its GDP per capita gap with benchmark countries in other regions by up to 1 percentage point. Simulations also show that gradually closing gender gaps in the labor force participation rate could lead to significant income gains over the long term.

Posted by at 11:45 AM

Labels: Inclusive Growth

Sunday, February 26, 2017

Housing Market in Africa: What We Do and Don’t Know

From Global Housing Watch Newsletter: February 2017

Kecia Rust is the Executive Director and founder of the Centre for Affordable Housing Finance in Africa (CAHF). In this issue of the Global Housing Watch newsletter, Rust talks about how CAHF is tracking the housing market in Africa, the “Big Mac Index” for housing, why housing finance remains elusive, why housing matters to all stakeholders, and more.

CAHF Team

From left to right: Kecia Rust, Kudakwashe Mativenga, Miriam Maina, Adelaide Steedley, Samuel Suttner, Sireena Ramparsad, Kgomotso Tolamo, Aqua Suliali, Noluthando Ntshanga, Joseph Tembe, and Alfred Namponya.

Hites Ahir: How do you track the housing market in African countries?

Kecia Rust: Historically, not many people have looked at housing market activity in African countries. Policy makers have seen housing as a social good that satisfied a right to shelter, while the private sector had very little involvement in housing markets as the majority of even high income households built their homes themselves. Trading activity simply was not monitored.

With the development of land titling systems and mortgage markets in many countries, and increased investment attention on residential property, however, this is changing, and there are a number of agencies that highlight residential property dynamics in their respective countries.

The focus of most of these efforts, however, is on higher value, and luxury property markets. While this is certainly of interest to investors and participants in those markets, it overlooks the potential and dynamics of the much larger market of middle class and emerging middle class households who are also beginning to express a demand for housing. The key challenge in this market segment, of course, is affordability.

For the past six years, CAHF has conducted an annual survey of local, in-country experts, to get an indication of the state of housing markets and housing affordability. We have asked them to define, from their professional perspectives, the price of the cheapest newly built house, built in the past year by a private developer. We also ask for the size of that house. The data does not indicate the cheapest house that can be built, but rather the cheapest house that is being built. This distinction is important: developers choose their markets based on a variety of factors including their sense of local affordability (a function not only of income but also the availability of end user finance), access to materials and construction finance, and their sense of local expectations.

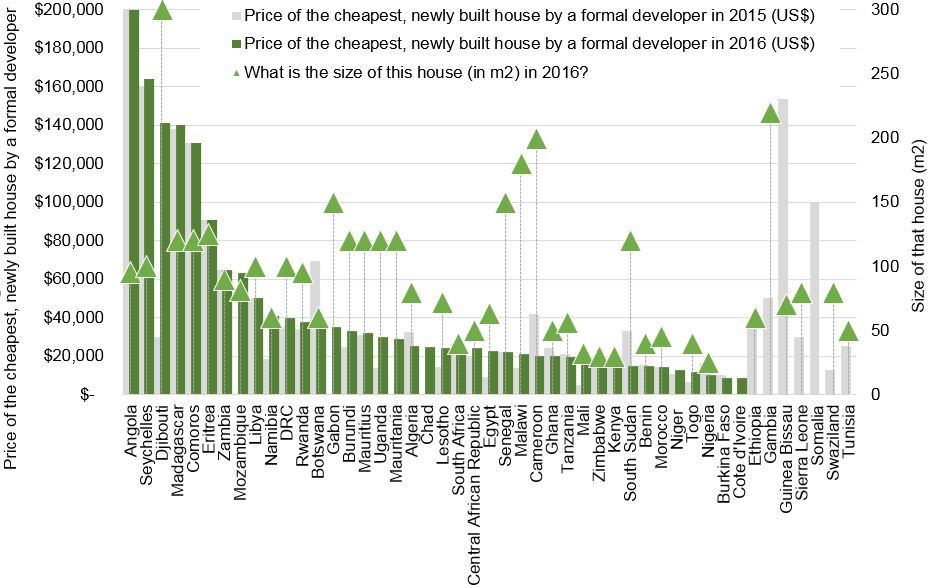

Figure 1: Price of the cheapest, newly built house by a formal developer: 2015 and 2016

Hites Ahir: What do current house prices tell us?

Kecia Rust: We can see a wide variation in the prices of the cheapest, developer-built houses. Of course, these are not equivalent structures. The US$200,000 house in Angola is about 100 square meters, whereas the US$10,000 Nigerian house is about 25 square meters.

But size doesn’t necessarily correlate with price. In Uganda, a 120 square meter house is recorded as costing US$30,000, while in Cameroon, a 200 square meter house was delivered and sold for about US$20,000. Our method clearly wasn’t comparing apples with apples, and local variation is invisible.

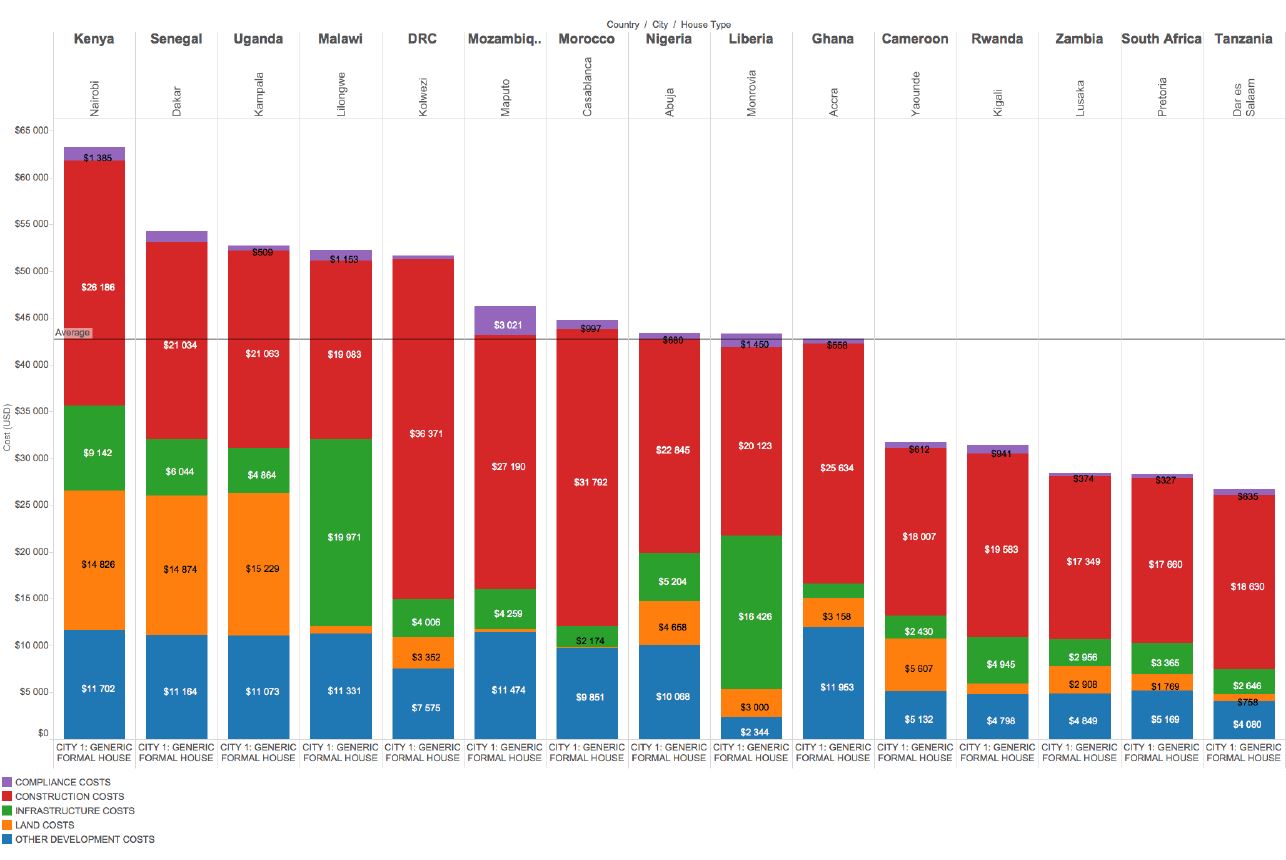

For this reason, we’ve tried a new methodology to track housing prices, by building something like a “Big Mac Index” for housing. Working with the Affordable Housing Institute, we designed a typical entry-level house: 46 square meters with a 9 square meter verandah, on a 120 square meter plot of land, in a 20-unit development. We prepared a Bill of Quantities down to brick level – with over 400 cost components – and sent this to Quantity Surveyors in 15 countries. We asked the Quantity Surveyors to prepare a quotation for this spec in the capital city, and another major city in the country. Then we checked the data, going back and forth with the Quantity Surveyors and thinking about local construction sector dynamics in the different countries. The data is about to be released, but we have some preliminary findings we can share.

We found that the price of this standard house ranged from just under US$30,000 in Dar es Salaam, Tanzania, to just over US$60,000 in Nairobi, Kenya. Significant variation was found in construction costs – the highest being in Kolwezi, Democratic Republic of Congo; as well as in infrastructure costs, which are particularly elevated in Lilongwe, Malawi and Monrovia, Liberia. High land prices, likely a result of urbanization pressures, were evident in Nairobi, Dakar, and Kampala.

The bigger story that this data is telling us is currently being explored, and we’ll publish it shortly, but a very clear takeaway at this stage is that it is about much more than the price of bricks: in the construction costs category, the major difference for the countries where these costs are highest (Democratic Republic of Congo, Morocco), is labour – over a third of the total construction value. In Nigeria, while the overall house price is close to the average of just above US$40,000, more than half of the construction component is labour. In some countries, indirect costs are a significant component of the construction component (Mozambique and Cameroon). Another category where there is quite significant variation is “other development costs”. This includes Marketing, Finance & Holding Costs, and Sales Taxes. Sales taxes were found to be highest in Nairobi (US$8,723, on a US$64,000 house, or 13 percent of the total price), Kampala, Dakar, Lilongwe, Casablanca and Kolwezi. Finance and Holding Costs were highest in Maputo (US$6,346, in a US$46,000 house).

Figure 2: Construction Costs by Categories

Hites Ahir: Are these prices affordable?

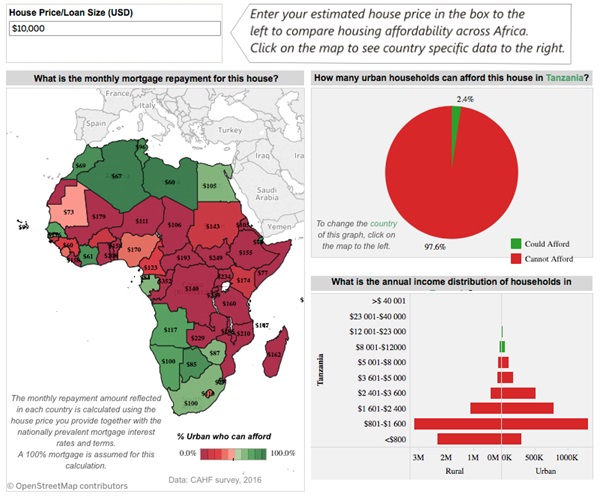

Kecia Rust: No. Not even to a large minority. We have an affordability calculator on our website that calculates the monthly mortgage repayment on a loan for a house. The user can input the house price, and based on the mortgage loan terms and income distribution in that particular country, if the loan were indeed available, the calculator reports the monthly repayment, and the proportion of the urban population that can afford that house.

While a US$20,000 housing loan is affordable to about 55 percent of urban households in Namibia, 49 percent of urban households in Morocco, and 59 percent of households in Cote d’Ivoire, it is affordable to only 3.8 percent of urban households in Kenya, 3.1 percent of urban households in Zambia, 0.7 percent of urban households in Tanzania, and 0.5 percent in Mozambique. If we reduced the house to US$10,000, the proportion of households with affordability does increase – just over 10 percent in Kenya, 6.7 percent in Zambia, 2.4 percent in Tanzania, and 1.7 percent in Mozambique – but it is still very limited.

Figure 3: Housing Affordability Calculator

There are two ways we might deal with this. On the one hand, housing affordability is a function not only of house price but also the terms of financing it. In Kenya, a mortgage loan is available for over ten years at 17.1 percent, while in Zambia the rate on a mortgage in 2016 was 27 percent over 15 years. In Tanzania, a mortgage can be accessed for a 25-year term, but the interest rate is still high at 19 percent. In Mozambique, a 20-year mortgage comes at a rate of 25 percent. If we flip the analysis around, we find that just on the basis of mortgage conditions in a country, a household in Tanzania that could afford to repay a house costing US$10,000, could afford a house in South Africa costing US$17,500, and in Cote d’Ivoire costing US$28,500.

Hites Ahir: Why is housing finance underdeveloped?

Kecia Rust: Housing finance markets in Africa are underdeveloped for a number of reasons. A key issue relates to the overall macroeconomic environment and the implications this has for access to and the cost of capital for lending. Lenders struggle to access capital to fund their housing loan portfolios – whether these are for mortgage or unsecured housing finance.

Many governments have set their Treasury Bill rates high, to attract investor capital to fund their own plans. This ‘risk free’ rate sets the baseline for any other investments that an investor may make. As the perception of risk increases, investors seek higher returns and this translates into the high interest rates that prevail – very many above 10 percent – across Africa.

The World Bank has been working in a number of countries to address this issue, with the introduction of mortgage liquidity facilities in Egypt, Tanzania, Nigeria and the WAEMU region. CAHF has developed a case study about these liquidity facilities.

There are also housing supply-side issues. Without housing stock being created in the price range that the market can afford to buy at scale, there isn’t much argument for lenders to develop their housing finance products. Housing and finance are very closely interlinked – the performance of each is dependent on the performance of the other.

Housing finance – investment capital, construction capital, end user finance, and all the facilitative interventions (guarantees, insurance, subsidies, etc.) that happen in between – is a critical ingredient to addressing the housing challenge in Africa. This section of the financial sector is underdeveloped for two reasons. First, financial sector development initiatives focus largely on other sectors: insurance, agriculture, small business development, and mobile money. The notion of a housing sector in the African context is still very new and the financial sector is unfamiliar with its dynamics. This is possibly because of the second reason: that housing finance is dependent on a much wider array of activities and sectors that together comprise the housing value chain – activities that are beyond the financial sector’s reach.

Hites Ahir: What are some of the challenges for the housing sector?

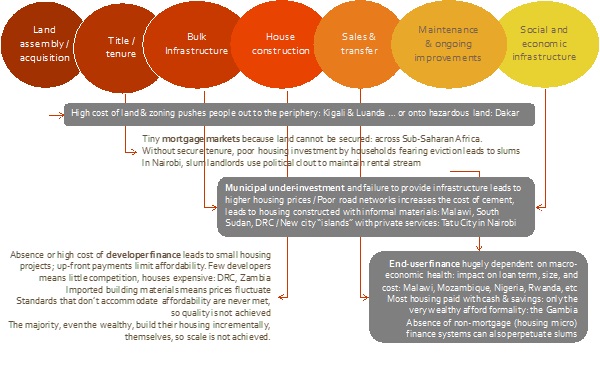

Kecia Rust: Challenges exist along the entire housing value chain, and each constraint in the system impacts on the availability of finance. Improving the flow of finance for housing requires improvements along the value chain – some of which extend outside of the housing finance sector. A weak value chain discourages investors, so they seek other targets and relegate housing sector investment to government. Government, however, does not have the capacity invest in the nation’s housing process on its own – investor interest must be captured and maintained if the housing sector is to grow and develop and meet the needs of all residents.

Figure 4: Housing Value Chain

Hites Ahir: How can policymakers address these challenges?

Kecia Rust: As a first step, policymakers must acknowledge that housing is a matter for attention across multiple sectors and multiple departments. This means that it is not only the housing and land department that must champion housing investment, but also the Central Bank and national treasury, as well as the National Deeds Registry. This is a matter for Cabinet attention.

On the housing and land side, there is a critical need for focused interventions into land and titling, and into infrastructure to support residential development. Housing delivery at scale cannot happen without those ingredients, and their absence is a key reason why housing continues to be delivered mostly by households themselves. Much of housing delivery is influenced by what is happening at the local level, however – and it is here that municipalities can apply specific levers to influence market dynamics and stimulate supply. Zoning, subdivisions, building plan processes and approvals, as well as administrative incentives that ease the costs in both time and money of the housing delivery process, are all levers that municipalities can apply to stimulate investment in housing.

On the finance side, macro-economic interventions to reduce the cost of capital and contain interest rates to reasonable levels for long-term finance are critically needed. Beyond that, policy makers should also consider the policy and regulatory issues that make mortgage lending possible and influence the cost of construction. In this regard, taxation appears to be a significant issue. Policy makers might wish to restrict taxes to upmarket housing for the wealthy, offering relief to the emerging middle class in the purchase of lower cost housing, or review how their current tax regime impacts on the attractiveness of this particular asset class. The Doing Business Indicators show us that in some countries, the cost of formally transferring property can be more than 10 percent of the value of the property. This becomes a serious disincentive to formal transactions.

To understand all of this, a clear and targeted monitoring and evaluation system is required. City, provincial, and national governments should be collecting data on housing market performance and making this available in the public domain for analysis and engagement by investors and other stakeholders. CAHF believes that a key constraint is the lack of market intelligence – accurate and trended market information, a clear indication of risk and return, and track records that prove long-term viability – specifically targeting the opportunities and the challenges that relate to the affordable housing market. Without this information, practitioners move to familiar territory and high margin activities, while governments are left wondering why they don’t engage. Bringing together the efforts of the public and the private sectors towards workable interventions that target increased opportunities for housing that is affordable to all market segments, is a key aim of CAHF’s work.

Hites Ahir: Are there any success stories that policymakers can learn from?

Kecia Rust: On the government reporting side, there are some very interesting interventions underway. The central banks of both Kenya and Tanzania publish mortgage market updates that provide information on the development of their mortgage markets. And the Nigerian Mortgage Refinance Corporation is in the process of developing a Nigerian Housing Finance Hub, to collect data about Nigeria’s housing finance market and share this with market players.

Some governments are improving their administrative regimes: Guinea Bissau has made significant improvements in the time it takes to transfer property, while Senegal has reduced the cost of registration significantly.

Then there are very interesting investors that have made improvements with the force of their interest in making development happen: International Housing Solutions managed to stimulate the construction of over 27,000 houses for the working class in South Africa, through its first fund and is now seeking to replicate this experience in a second fund. Phatisa’s Pan African Housing Fund is active in developments in Zambia, Rwanda, and Kenya. IFC’s investment in the Chinese multinational construction and engineering company, CITIC Construction, is intended to set development precedents, targeting a scale delivery approach that is currently not very common across the continent. And there are more. Policy makers should actively engage with these efforts by the private sector to identify where they can smooth the value chain to enable more and better investment.

From Global Housing Watch Newsletter: February 2017

Kecia Rust is the Executive Director and founder of the Centre for Affordable Housing Finance in Africa (CAHF). In this issue of the Global Housing Watch newsletter, Rust talks about how CAHF is tracking the housing market in Africa, the “Big Mac Index” for housing, why housing finance remains elusive, why housing matters to all stakeholders,

Posted by at 7:12 PM

Labels: Global Housing Watch

Subscribe to: Posts