Saturday, June 24, 2017

Global Housing Watch – Q2 2017

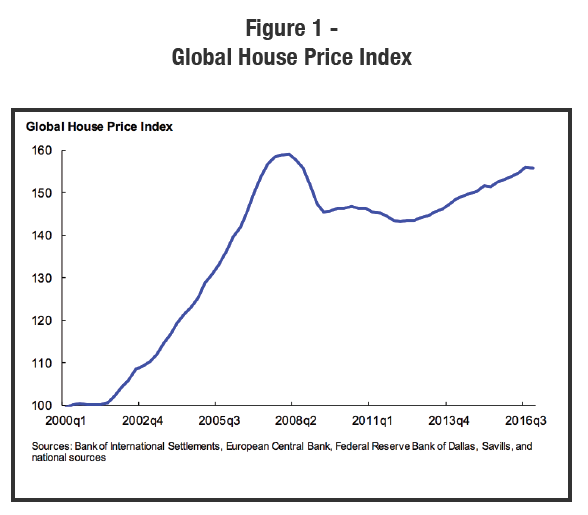

The IMF Global House Price Index is nearly back to its prior peak (see Figure 1). We have previously addressed the question of whether conditions at present are sufficiently similar to those in place during the bubble period of 2005-2008 and answered with a some-what tentative “no” (see Global House Prices: Time to Worry Again?).

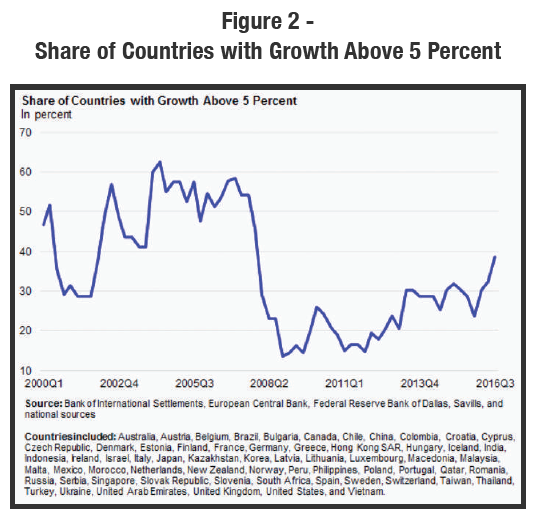

The somewhat sanguine view is partly explained by a lack of synchronicity at present that distinguishes the current state from that experienced a decade ago (see Figure 2). The answer is tentative, because over the last four years the number of countries experiencing rapid growth has approximately doubled, while remaining significantly below the prior peak.

Continue reading here.

The IMF Global House Price Index is nearly back to its prior peak (see Figure 1). We have previously addressed the question of whether conditions at present are sufficiently similar to those in place during the bubble period of 2005-2008 and answered with a some-what tentative “no” (see Global House Prices: Time to Worry Again?).

The somewhat sanguine view is partly explained by a lack of synchronicity at present that distinguishes the current state from that experienced a decade ago (see Figure 2).

Posted by at 5:14 PM

Labels: Global Housing Watch

Thursday, June 22, 2017

Forecasting Long-Term Interest Rates: A Long History of Errors

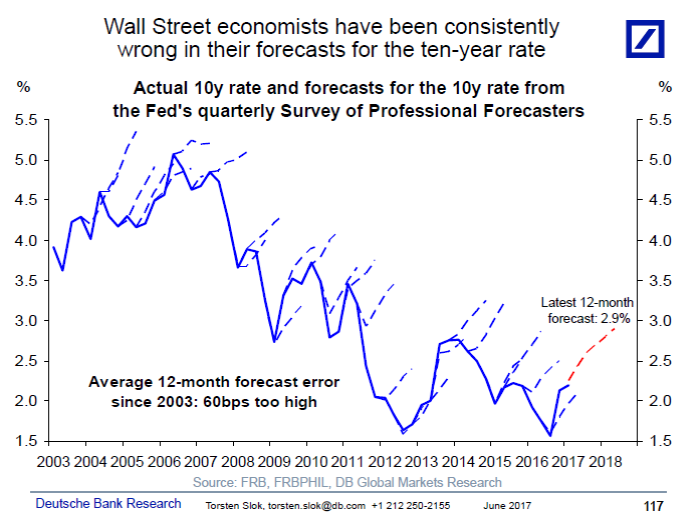

Deutsche Bank’s chief international economist Torsten Slok writes: “The Fed’s Survey of Professional Forecasters for 2017 Q2 shows that 10-year rates are expected to rise to 2.9% over the coming 12 months. The problem is that Wall Street economists have been consistently too optimistic for the past 15 years, see chart below. To correct for the excessive optimism among forecasters, one can subtract the average forecast error, i.e. the average mistake made for the past 15 years by the forecasting community, which is 0.6%-points. Doing that gives a 12-month forecast for 10-year rates of 2.3%.”

Deutsche Bank’s chief international economist Torsten Slok writes: “The Fed’s Survey of Professional Forecasters for 2017 Q2 shows that 10-year rates are expected to rise to 2.9% over the coming 12 months. The problem is that Wall Street economists have been consistently too optimistic for the past 15 years, see chart below. To correct for the excessive optimism among forecasters, one can subtract the average forecast error, i.e. the average mistake made for the past 15 years by the forecasting community,

Posted by at 3:37 PM

Labels: Forecasting Forum

House Prices in Iceland

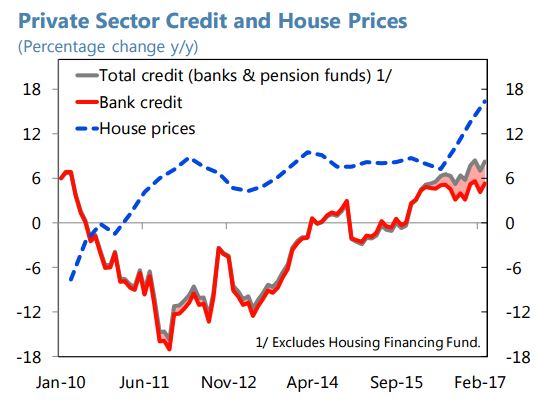

“Housing prices have surged despite still moderate credit growth. Total credit to the private sector, including loans from pension funds which now account for about half of new mortgages, has been growing at close to 8 percent y/y. Despite the recent pick up in (mostly inflation indexed) mortgage lending, the ratio of household debt to GDP has fallen from a peak of some 120 percent in 2010 to below 80 percent in 2016. Housing prices climbed almost 10 percent in 2016, centered on Reykjavík where the crowding out of homebuilding by hotel construction, and of rentals to residents by rentals to tourists, is most acute. A supply response appears to be kicking in, however, with residential investment expanding by 34 percent in 2016. For now, investment financing has a large element of retained earnings”, according to the new IMF report on Iceland.

The report also says that “Housing pressures could tip the economy into overheating. Mortgage lending, while still moderate, is picking up, calling for vigilance. Macroprudential tools should address this if needed, and should include new powers to limit foreign currency lending to unhedged borrowers and, potentially, to prohibit lending by pension funds. Construction could keep lagging demand, pushing housing prices higher. If rising living costs kept foreign workers away, labor market conditions would heat up. Another round of large wage increases would compound domestic demand pressures.”

“Housing prices have surged despite still moderate credit growth. Total credit to the private sector, including loans from pension funds which now account for about half of new mortgages, has been growing at close to 8 percent y/y. Despite the recent pick up in (mostly inflation indexed) mortgage lending, the ratio of household debt to GDP has fallen from a peak of some 120 percent in 2010 to below 80 percent in 2016. Housing prices climbed almost 10 percent in 2016,

Posted by at 2:28 PM

Labels: Global Housing Watch

Wednesday, June 21, 2017

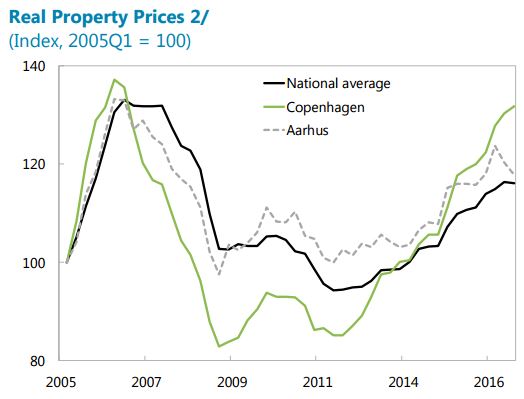

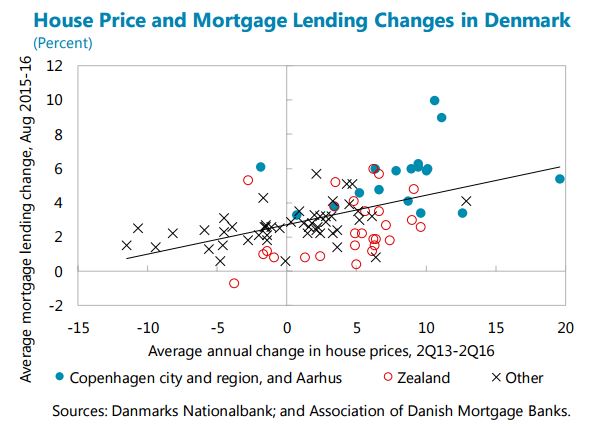

Denmark’s Housing Market

“House prices continue to rise, particularly in regions with strong new credit creation (…) While a shock to the housing market would probably not pose an acute threat to the banking system, macroeconomic risks are substantial (…) The authorities are considering additional macroprudential measures to curb risks (…) A recently agreed reform of property taxation is a step forward (…) [IMF] Staff advocated pushing ahead with macroprudential and other policies to safeguard macrofinancial stability. Recommended measures span several policy areas. (…) Staff reiterated its call for putting in place a DTI limit and welcomed the SRC’s proposal (…) The broad housing recovery and current low interest rates provide a conducive environment for reducing the tax deductibility of mortgage interest expenses and for further lowering, beyond what is currently planned, the value of the deduction for interest payments (…) Addressing longstanding housing supply constraints, such as strict zoning regulations, procedures for land development, and rental market regulations, can also help ease housing price pressures by improving the responsiveness of supply to housing demand (…) The authorities agreed that house price increases in certain areas called for vigilance”, according to the IMF’s latest report on Denmark.

“House prices continue to rise, particularly in regions with strong new credit creation (…) While a shock to the housing market would probably not pose an acute threat to the banking system, macroeconomic risks are substantial (…) The authorities are considering additional macroprudential measures to curb risks (…) A recently agreed reform of property taxation is a step forward (…) [IMF] Staff advocated pushing ahead with macroprudential and other policies to safeguard macrofinancial stability. Recommended measures span several policy areas.

Posted by at 2:26 PM

Labels: Global Housing Watch

Thursday, June 15, 2017

Rodrik on Financial Globalization and Inequality

Dani Rodrik writes:

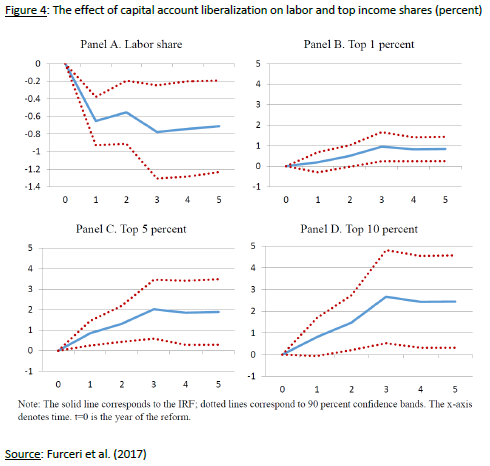

“Financial globalization appears to have produced adverse distributional impacts within countries as well, in part through its effect on incidence and severity of financial crises. In a remarkable series of papers, researchers at the IMF have documented these negative inequality impacts (Jaumotte et al. 2013; Furceri and Loungani 2015). Most noteworthy is the recent analysis by Furceri et al. (2017) that looks at 224 episodes of capital account liberalization, most of them taking place during the last couple of decades. Liberalization episodes are identified by big changes in a standard measure of financial openness (the Chinn-Ito index) and large subsequent capital flows. They find that capital-account liberalization leads to statistically significant and long-lasting declines in the labor share of income and corresponding increases in the Gini coefficient of income inequality and in the shares of top 1, 5, and 10 percent of income (see Figure 4 for their key results). Furthermore, these adverse effects on inequality are stronger in cases where de jure liberalization was accompanied by large increase in capital flows. Financial globalization appears to have complemented trade in exerting downwards pressure on the labor share of income.

Why would financial globalization increase inequality and the capital share in particular? There is no analogue to trade theory’s Stolper-Samuelson theorem in international macroeconomics. So to some extent these distributional consequences of financial globalization are a genuine surprise. But there may be an obvious, bargaining-related explanation (as argued in Rodrik 1997, chap. 2). As long as wages are determined in part by bargaining between employees and employers, the outside options of each party play an important role. Capital mobility gives employers a credible threat: accept lower wages, or else we move abroad. Indeed, Furceri et al. (2017) provide some evidence that the decline in the labor share is related to the threat of relocating production abroad. As a proxy for the potential threat they use layoff propensities of different industries. They find the effect of capital account liberalization on labor shares is particularly strong in those sectors with a higher natural layoff rate. The bargaining explanation is also consistent with the finding in Jaumotte et al. (2013) that it is foreign direct investment in particular that is associated with the rise in inequality.”

Continue reading here.

Dani Rodrik writes:

“Financial globalization appears to have produced adverse distributional impacts within countries as well, in part through its effect on incidence and severity of financial crises. In a remarkable series of papers, researchers at the IMF have documented these negative inequality impacts (Jaumotte et al. 2013; Furceri and Loungani 2015). Most noteworthy is the recent analysis by Furceri et al. (2017) that looks at 224 episodes of capital account liberalization, most of them taking place during the last couple of decades.

Posted by at 9:11 AM

Labels: Inclusive Growth

Subscribe to: Posts