Sunday, September 17, 2017

Global House Prices: An Update

Global Housing Watch Newsletter: September 2017

In this interview, Kate Everett-Allen talks about Knight Frank’s dataset on global house prices. She also talks about the state of global house prices at the national level, city level, and at prime residential level. Kate Everett-Allen is a Partner at Knight Frank, and specializes in residential research.

House prices across countries…

Hites Ahir: Why and in what way does Knight Frank track global house prices?

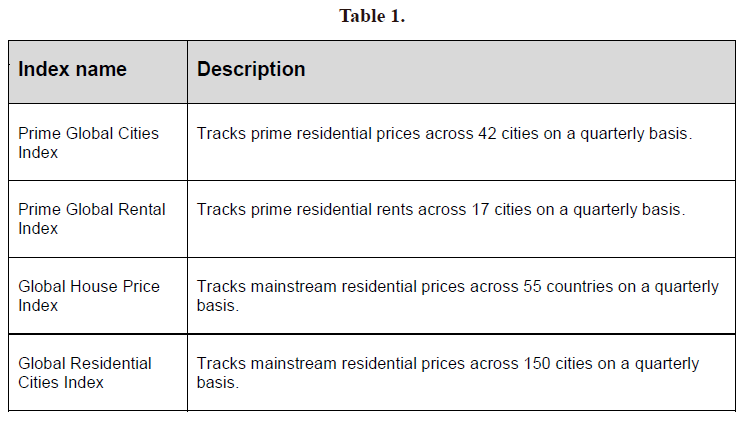

Kate Everett-Allen: We have been monitoring house price movements for the last decade in order to meet the needs of our clients who want to gauge market performance on a like-for-like basis. With this in mind, we have developed four residential indices that track both mainstream, and prime prices, and rents at a country, and city level.

Hites Ahir: What does the latest reading of Knight Frank’s Global House Price Index show?

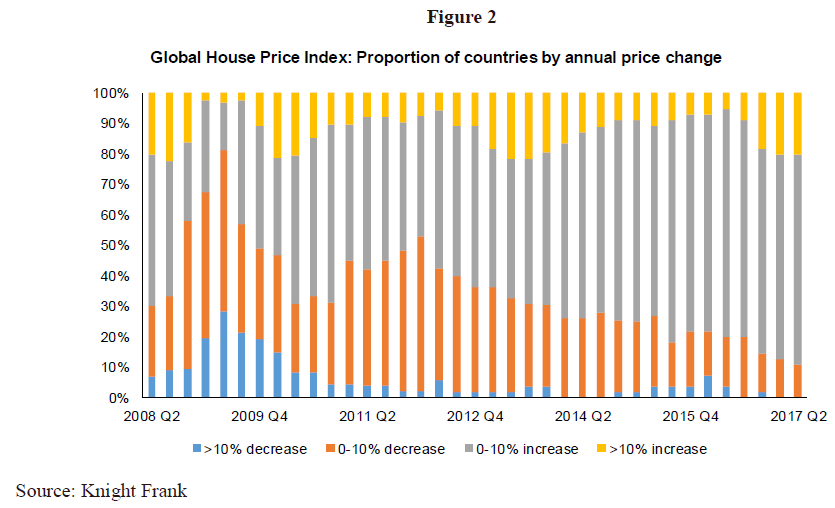

Kate Everett-Allen: Our latest Global House Price Index, which tracks the movement in average house prices across 55 countries worldwide, shows the extent to which housing markets have recovered from the global financial crisis. Following Lehman Brothers’ collapse in 2008, 42 percent of the countries in our index recorded positive annual growth, in Q2 2017 this figure has accelerated to 89 percent.

That is not to say there are no headwinds. The latest edition of our index, which covers the year to Q2 2017, saw the index’s overall rate of annual growth decline for the first time since Q4 2015. As policymakers step away from economic stimulus (UK, US, Japan), Brexit negotiations dominate the UK and European landscape and geopolitical tensions persist across multiple continents (N Korea, Middle East, Ukraine) there are signs this is filtering through to buyer and investor sentiment.

Hites Ahir: In terms of momentum, are we seeing more countries with higher house price growth?

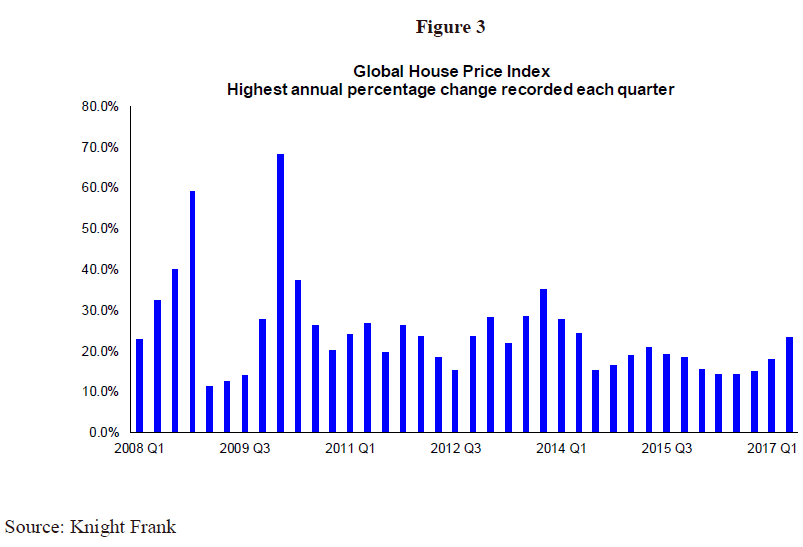

Kate Everett-Allen: Eleven of the 55 countries tracked by our index recorded double-digit annual price growth in the year to June 2017, the last time this figure was exceeded was in Q3 2013. The uptick occurred in Q4 2016 with countries such as Iceland, New Zealand, Canada and Turkey all performing strongly.

Extracting the highest-ranking annual percentage change recorded each quarter provides further evidence of this trend with a slight uptick evident in the last two quarters.

House prices across cities…

Hites Ahir: You have also collected house price data at the city level. What does the latest reading of Knight Frank’s Global Residential Cities Index show?

Kate Everett-Allen: The Global Residential Cities Index, which tracks average house prices across 150 cities worldwide, has risen for four consecutive quarters.

The latest edition, covering the 12 months to Q1 2017, highlights the outperformance of China’s first tier cities. Seven of our top ten rankings are occupied by Chinese cities, with Wuxi (31.7 percent) and Nanjing (28.8 percent), each home to a population of over 6 million, occupying the highest rankings.

Toronto (24.8 percent) sits in fourth place, however, with the introduction of a new homebuyer tax in March this year, we expect price growth to moderate, mirroring the trend seen in Vancouver (12.2 percent).

In Europe, the Norwegian capital, Oslo (21 percent), and the four largest Dutch cities – all recording annual growth in excess of 10 percent – are emerging as key centers of growth.

Hites Ahir: Could you tell us a bit about the house price developments at the city level for China vs. the United States?

Kate Everett-Allen: The index tracks twenty cities in both countries. On average residential prices across the US cities increased by 6.4 percent in the year to June 2017, whilst Chinese cities recorded a 15.9 percent rise.

However, analysis of price changes over a three-month period casts a different light. The average price of a property in the US cities rose 2.2 percent between March and June this year, whilst Chinese cities mustered only a 0.7 percent uplift.

These figures suggest the latest round of cooling measures introduced across Chinese cities, which range from higher mortgage down payments to limits on second home purchases and quotas on new home sales, are influencing market performance.

Luxury residential prices across cities…

Hites Ahir: What does the latest reading of Knight Frank’s Prime Global Cities Index show?

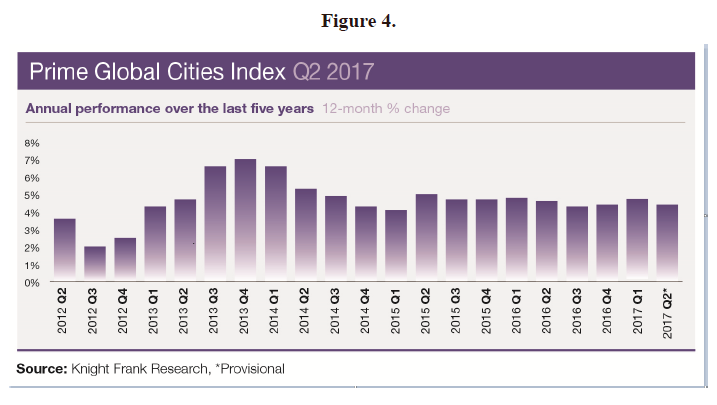

Kate Everett-Allen: Our Prime Global Cities Index, which tracks luxury prices across more than 40 cities, shows less volatility than our average residential price indices. The rate of price growth recorded by our Prime Global Cities Index has been largely static since 2014, registering an uplift of between 4 percent and 5 percent year-on-year for the last 12 quarters.

Asian cities are well-represented at the top of our latest annual rankings with Guangzhou (35.6 percent), Seoul (20.7 percent), Shanghai (19.9 percent), Beijing (15.0 percent), Sydney (11.5 percent) and Melbourne (9.1 percent) all sat within the top ten.

Hites Ahir: How is economic and political uncertainty affecting prime property market?

Kate Everett-Allen: Slow economic growth has influenced markets such as Tokyo (-2.8 percent) and Moscow (-11.8 percent) in the last year where GDP growth has declined, oil prices slipped and currencies weakened.

Conversely, economic uncertainty has strengthened safe haven capital flows into other luxury property markets such as Berlin, Madrid and Paris from markets such as Turkey, Venezuela and the Middle East prompted by political or security concerns.

This movement of wealth, particularly where it occurs on a large scale, is sparking the attention of policymakers (Toronto, London, Sydney) keen to curb price inflation by deterring speculative investment via foreign buyer taxes or stamp duty hikes.

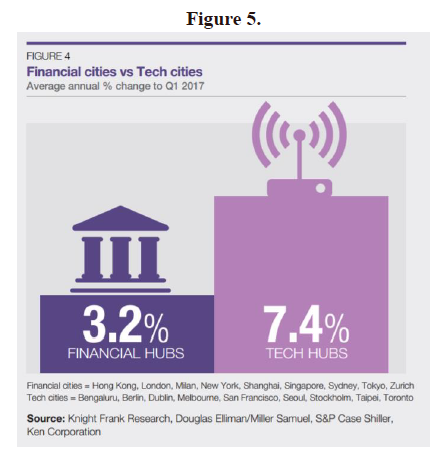

Hites Ahir: How does prime residential prices compare in financial cities, tech cities, and other cities?

Kate Everett-Allen: In the Q1 2017 edition of our Prime Global Cities Index we compared the price performance of established financial cities such as London, New York, Hong Kong against emerging technology hubs such as Berlin, San Francisco, Stockholm.

Perhaps unsurprisingly, the vibrant technology hubs that are attracting new pools of creative talent, but where new supply has yet to catch up with demand, came out on top. Here, prime prices recorded a 7.4 percent rise year-on-year, compared with a 3.2 percent rise for the world’s top financial capitals over the same period.

For more information on any of the indices please contact Kate Everett-Allen or visit www.knightfrank.com/research

Global Housing Watch Newsletter: September 2017

In this interview, Kate Everett-Allen talks about Knight Frank’s dataset on global house prices. She also talks about the state of global house prices at the national level, city level, and at prime residential level. Kate Everett-Allen is a Partner at Knight Frank, and specializes in residential research.

House prices across countries…

Hites Ahir: Why and in what way does Knight Frank track global house prices?

Posted by at 6:00 PM

Labels: Global Housing Watch

Friday, September 15, 2017

Housing View – September 15, 2017

On cross-country:

- Our Home in Days Gone By: Housing Markets in Advanced Economies in Historical Perspective – Freie Universität Berlin

- Stabilising the housing market – VOX

- Partnership on Housing delivers guidance on state aid and a toolkit for affordable housing – European Commission

- The State of Housing in the EU 2017 – Housing Europe

- World’s Housing Market Set to Slow – Bloomberg

- Why “affordable housing” in Africa is rarely affordable – Economist

- Demographic change and house prices: Headwind or tailwind? – Economic Letters

On the US:

- Tarnishing the Golden and Empire States: Land-Use Restrictions and the U.S. Economic Slowdown – NBER

- Who Defaults on Their Mortgage, and Why? Policy Implications for Reducing Mortgage Default – Federal Reserve Bank of Minneapolis

- Maybe Cities Are the Future of Suburbs – Bloomberg

- How Harvey Will Affect Houston’s Housing Market – Bloomberg

- Houston’s Unsinkable Housing Market Undaunted by Storm – New York Times

- House Prices to Median Household Income – Calculated Risk

On other countries:

- [Denmark] Short-Term Expectation Formation Versus Long-Term Equilibrium Conditions: The Danish Housing Market – University of Copenhagen

- [Germany] Three Risks for the German Residential Property Market – Cologne Institute of Economic Research

- [Hong Kong] Hong Kong Finance Chief Warns Again of Property Risk on Fed – Bloomberg

- [Ireland] Report finds Irish housing subsidy not key price driver – Reuters

- [Ireland] Central Bank singles out cash buyers as key driver of house prices – The Irish Times

- [Pakistan] ‘Land Mafia’ Killing Exposes Dark Underbelly of Pakistan’s Property Boom – Bloomberg

- [New Zealand] Macroprudential policies in a low interest-rate environment – Reserve Bank of New Zealand

- [Sweden] Swedish central bank wants tighter mortgage rules as soon as possible – Reuters

- [United Arab Emirates] Dubai Property Set to Fall Further as Vacancies Climb – Bloomberg

On cross-country:

- Our Home in Days Gone By: Housing Markets in Advanced Economies in Historical Perspective – Freie Universität Berlin

- Stabilising the housing market – VOX

- Partnership on Housing delivers guidance on state aid and a toolkit for affordable housing – European Commission

- The State of Housing in the EU 2017 – Housing Europe

- World’s Housing Market Set to Slow – Bloomberg

- Why “affordable housing” in Africa is rarely affordable – Economist

- Demographic change and house prices: Headwind or tailwind?

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, September 13, 2017

Increasing Resilience to Large and Volatile Capital Flows: The Role of Macroprudential Policies in Cambodia

On Cambodia, the new IMF report says that:

“The rapid pace of credit growth, its relatively long duration, and tilt towards real estate has increased systemic financial risks. Strong credit growth commenced in 2003–04, was briefly interrupted in 2009, and reached 30 percent year on year on average between 2010 and 2016. Although credit growth moderated to near 20 percent in early 2017, the credit gap remains large and is estimated to exceed 10 percent of GDP. Real estate, construction and mortgages have been the fastest growing segments of lending, with growth rates exceeding 50 percent in recent years, before slowing in 2016. Lending to the construction, real estate and mortgage sector accounted for 21.5 percent of the total credit stock at end-2016.

The rapid expansion of the real estate sector, funded in part by external borrowing, has led to a build-up of macro-financial stability risks. Rapid construction risks an eventual oversupply in the real estate market, which could precipitate a disorderly adjustment (with the risks particularly pronounced in the middle-range condominium segment, which has been mostly driven by foreign investors), adversely affecting the banking sector via a spike in NPLs, potentially putting a drag on credit growth and economic activity (see Article IV 2016). The critical link between capital flows and real estate projects was illustrated in 2009, when a reversal of flows led to the collapse of major construction projects, particularly in Phnom Penh, contributing to a severe if temporary economic slowdown.

The authorities have sought to address the risks stemming from significant capital inflows and credit growth through a range of macroprudential measures:

- Liquidity tools. Reserve requirements have been the main instrument used to contain excess liquidity fueled by external funding, and to moderate the pace of credit growth. In 2008, the NBC doubled the reserve requirement on foreign currency bank deposits to 16 percent amid large sustained capital inflows, although this was subsequently relaxed to 12 percent in early 2009 during the global financial crisis. As inflows resumed, the authorities raised bank reserve requirements for foreign currency deposits again by a slight 50 basis points to 12.5 percent in September 2012. To address risks associated with growing non-core funding sources, banks’ external borrowings were included in the reserve requirement base in March 2015. Reserve requirement rates are now 8 percent for local currency liabilities (unremunerated) and 12.5 percent (of which 4.5 percent is remunerated) for foreign currency liabilities (including external borrowing).

- Broad-based capital tool. Regulatory increases in minimum capital requirements have aimed at further strengthening the resilience of the financial sector.

- Sectoral asset-side tool. A lending cap of 15 percent was imposed on the property sector of banks’ total loan portfolios in 2008.

The authorities have also aimed to contain risks pertaining to real-financial linkages which could increase procyclicality. In addition to a lending cap on the property sector imposed in 2008, the authorities have recently tightened licensing and supervision on real estate developers, and expanded the coverage of stamp duty on real estate transactions (without differentiating by residency). A new regulation effective April 2017 caps the interest rate on all MFI loans at 18 percent, regardless of loan maturities. This reflects the authorities’ concerns about excessive debt accumulation in rural areas.

The Article IV consultations in 2015 and 2016 recommended additional measures to build resilience and help engineer a soft landing of the credit cycle. While supervisory capacity has improved since the 2010 FSAP recommendations, gaps in financial supervision and regulation have remained. A critical challenge highlighted was to close the regulatory gap stemming from the fact that MFIs are competing with banks for the same funding base and are subject to similar credit, liquidity and FX risks as banks, but subject to looser regulations. Article IV consultations recommended an expanded range of micro and macroprudential tools. These include sectoral tools such as higher risk weights, concentration limits, and LTV/DTI limits on real estate lending; and liquidity tools such as limits on LTD ratios to strengthen internal sources of funding and serve as a brake on excessive credit growth.”

On Cambodia, the new IMF report says that:

“The rapid pace of credit growth, its relatively long duration, and tilt towards real estate has increased systemic financial risks. Strong credit growth commenced in 2003–04, was briefly interrupted in 2009, and reached 30 percent year on year on average between 2010 and 2016. Although credit growth moderated to near 20 percent in early 2017, the credit gap remains large and is estimated to exceed 10 percent of GDP.

Posted by at 4:52 PM

Labels: Global Housing Watch

Increasing Resilience to Large and Volatile Capital Flows: The Role of Macroprudential Policies in Sweden

On Sweden, the new IMF report says that:

“The robust economy and low interest rates, together solid population growth and inelastic housing supply, boosted housing prices and hence household debt:

- As a percentage of disposable income, household indebtedness has almost doubled since 1996 and now stands at about 180 percent, with a growing share of new borrowers taking on high debts relative to income. The growth in debt has primarily reflected rising housing prices owing to prolonged supply demand imbalances exacerbated by low amortization, low interest rates, and tax incentives to hold real estate and to finance it with debt.

- House prices have also doubled in real terms since 1996 and Swedish homes are highly valued from a historical perspective. The price-to-income ratio is 40 percent above

its 20-year average—highest among the OECD countries. Model-based estimates of overvaluation are notably smaller, at about 10 percent, but are subject to significant

uncertainty.Cheap wholesale funding, from a mix of Swedish and foreign sources, including in foreign currency, has underpinned mortgage growth. Customer deposits represent around 40 percent of banks’ total funding since Swedish households invest a large proportion of savings in mutual funds rather than bank accounts, in part reflecting high mandatory contributions to

pension funds (Figure 2). With banks having one of the highest loan-to-deposit ratios in European countries (about 200 percent), the long-maturity residential mortgages rely on wholesale funding, such as covered bonds, unsecured bonds and commercial paper, giving rise to refinancing risks. Nonetheless, a substantial portion of this wholesale funding comes from Swedish pension funds and insurance companies, who may be less flighty investors. About half of the wholesale funding is in foreign currency predominantly in euro and USD. The Riksbank estimates that about 25 percent of the major banks’ foreign funding is used to fund Swedish assets. The banks use currency swaps to hedge this funding to match their SEK denominated loans.Home ownership financed by high levels of mortgage debt make households vulnerable to falling house prices. Although the immediate effect of a potential decline in housing prices on Swedish household default rates appears to be contained, the indirect macroeconomic impact can be sizeable. Analysis by Sweden’s National Institute of Economic Research finds a 20 percent drop in housing prices would lead to a recession-like impact on household consumption and unemployment, with an even greater impact if this drop coincided with a global downturn. In an extreme but plausible scenario, this can combine with a broader loss of confidence in housing collateral and potentially higher funding interest rates. Given the

high interconnectedness among the Nordic-Baltic financial systems, such a shock could also have significant cross-border spillovers.Swedish banks’ heavy reliance on wholesale funding in FX could reinforce the risks. As illustrated by the financial crisis, the build-up of unease on international financial markets from 2007 had an impact on the Swedish covered bond market. During the second half of 2007, foreign investors reduced their holdings of Swedish covered bonds by almost one-third affecting the banks’ possibilities of obtaining funding and prompting government intervention.

The authorities have responded to rising household debt with a range of macroprudential measures to protect the resilience of households and the banking sector (Table 1). An 85 percent cap on loan-to-value (LTV) ratios was adopted in 2010 in order to protect households against the risk of negative equity which could increase the risk of default.10 A requirement for a stress test on households at the time of mortgage origination aims to ensure households have adequate buffers against significantly higher interest rates. In May 2013, the FSA introduced a 15 percent floor for risk weights on Swedish residential mortgages to address IRB model risks. In 2014, the floor was raised to 25 percent as a macroprudential measure, to target risks arising from high growth rates in residential mortgage lending. The countercyclical capital buffer has been increased three times since 2015 to support banks’ resilience to shocks. The recently introduced minimum amortization requirement applies to mortgages issued after June 2016, until LTV ratios reach 50 percent. The minimum annual amortization is 2 percent for LTV ratios above 70 percent, and 1 percent for LTV ratios between 50 and 70 percent.

The authorities also introduced a Liquidity Coverage Ratio (LCR) requirement11 to reinforce the banks’ resilience to shocks in FX funding. The requirement of 100 percent, introduced in January 2013, applies separately to EUR and USD as well as to all currencies and ensures that the banks have enough liquid FX assets to withstand FX liquidity stress in the short term. The decision to also introduce separate currency requirements was justified by Swedish banks’ extensive dependence on market funding in foreign currency, which makes them particularly sensitive to liquidity shocks in these currencies. In addition, as the Riksbank’s ability to provide liquidity assistance in foreign currency is limited, the authorities argued that it is important that the banks themselves ensure that they have FX buffers to deal with liquidity disruptions in the main foreign currencies.

Macroprudential measures appear to have helped contain vulnerabilities, and may have slowed housing prices and lending, but it is not yet clear how lasting the latter impacts will be. Average LTV ratios on new mortgages have declined from 71 percent in 2010 to 69 percent in 2016, and credit growth to households has remained at a single digit pace since 2010, even as house prices gains accelerated to around 15 percent in 2014-15. The announcement of the mortgage amortization requirement in late 2015 was followed by a period of significantly slower housing price increases, especially in apartments, which was reflected in slower credit growth with a lag. But following the actual implementation of the measure, prices appears to rebound somewhat in the second half of 2016. Nonetheless, housing price increases remain well below the pace seen in 2014-15. For new mortgages, average amortization has risen to 4.6 percent of income in 2016, from 3.3 percent in 2015. Further analysis of the impact of the amortization requirements by the Swedish supervisor finds it has resulted in households buying less expensive homes and borrowing less, which suggests the potential for a more lasting effect on the level of housing demand and household debt. The share of households taking on high debt burdens (exceeding 600 percent of gross disposable income) had risen from 10 percent in 2011 to 17 percent 2015, but edged back to 16.4 percent in 2016.

The Article IV consultations in 2015 and 2016 recommended additional measures to address the risks associated with rising housing prices and housing indebtedness. The consultations emphasized the need for deep reforms of Sweden’s poorly functioning housing market, including to (i) sustain the increase in housing supply; (ii) tax reforms to reduce housing demand and incentives for debt financing, and; (iii) phasing out rent controls which leave many household with no option other than to purchase. It also recommended that a limit on the share of high debt-to-income (DTI) loans be adopted soon to contain increases in the interest sensitivity of consumption and protect household resilience to incomes losses, to automatically reduce LTVs on high DTI loans when housing prices rise faster than income, and to make lending responses to housing price increases less elastic, dampening potential for an upward credit-price spiral.”

On Sweden, the new IMF report says that:

“The robust economy and low interest rates, together solid population growth and inelastic housing supply, boosted housing prices and hence household debt:

- As a percentage of disposable income, household indebtedness has almost doubled since 1996 and now stands at about 180 percent, with a growing share of new borrowers taking on high debts relative to income. The growth in debt has primarily reflected rising housing prices owing to prolonged supply demand imbalances exacerbated by low amortization,

Posted by at 4:41 PM

Labels: Global Housing Watch

Tuesday, September 12, 2017

Does Okun’s Law Hold in Swaziland?

No, the causes for high unemployment rate appear to be more structural in nature, as an IMF report documents.

No, the causes for high unemployment rate appear to be more structural in nature, as an IMF report documents.

Posted by at 9:16 AM

Labels: Inclusive Growth

Subscribe to: Posts