Monday, November 20, 2017

Housing in Sweden

From IMF’s latest report on Sweden:

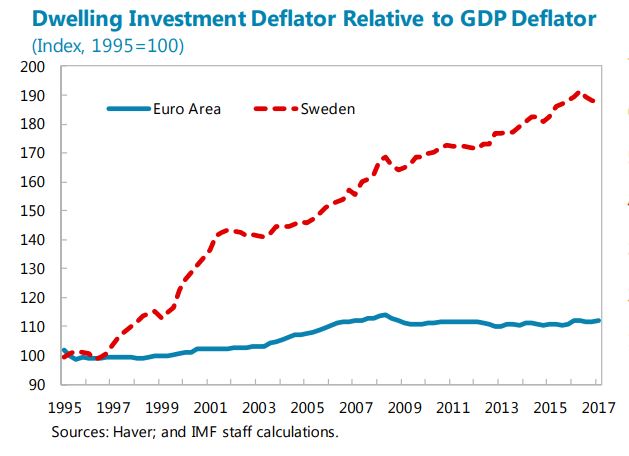

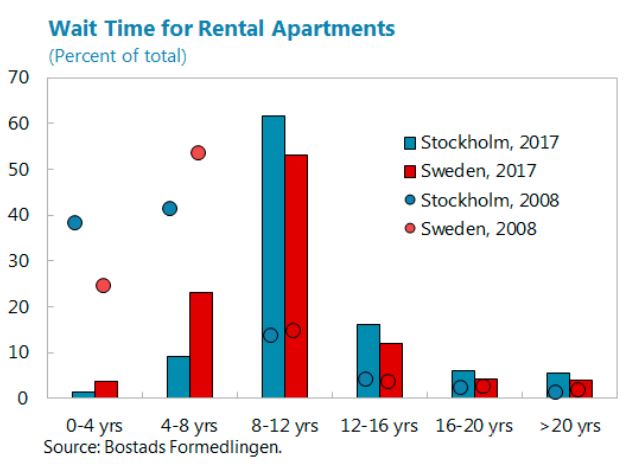

“The Swedish housing market has deep structural problems. Large house price increases were necessary to overcome the hurdle of high construction costs before construction began rising. These costs reflect a combination of complex building regulations and limited competition in the sector owing to cumbersome municipal land sale and planning and approval procedures. The resulting supply shortfalls are present in 255 out of 290 municipalities, but are mostly in the three major metropolitan areas (Stockholm, Gothenburg, and Malmo) owing to ongoing urbanization. Moreover, strict rent controls have resulted in a declining supply of rental apartments as they are converted into tenant-owned condominiums and as existing renters are “locked-in”. The resulting long waiting times for rental apartments leave many households with no option but to purchase housing, which is incentivized by the tax deductibility of mortgage interest payments.”

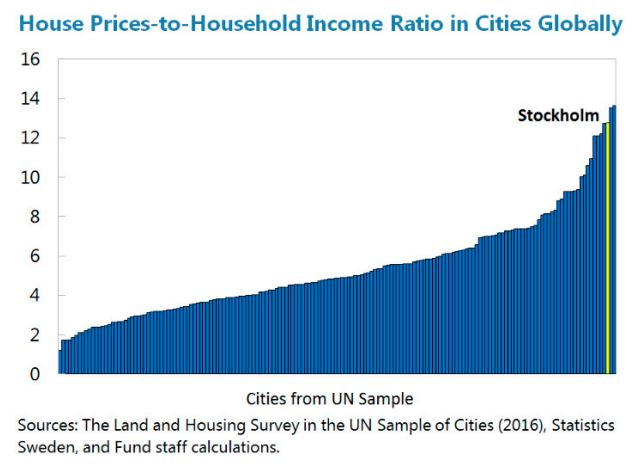

“Low housing affordability undermines financial stability, growth, and equality. Home costs relative to median household income have more than doubled since the mid-1990s (…). In Stockholm, the price-to-income ratio is nearly twice the national average and is among the highest worldwide. These factors reduce labor mobility, especially for those from outside the main centers, hindering inclusive growth. Equity is further undermined by overcrowding among low-income groups and the need to rely on parental savings for housing purchases. Households must borrow more at higher house prices, lifting household debt to 182 percent of disposable income (…), with new purchasers taking on debts averaging 402 percent of their disposable income.”

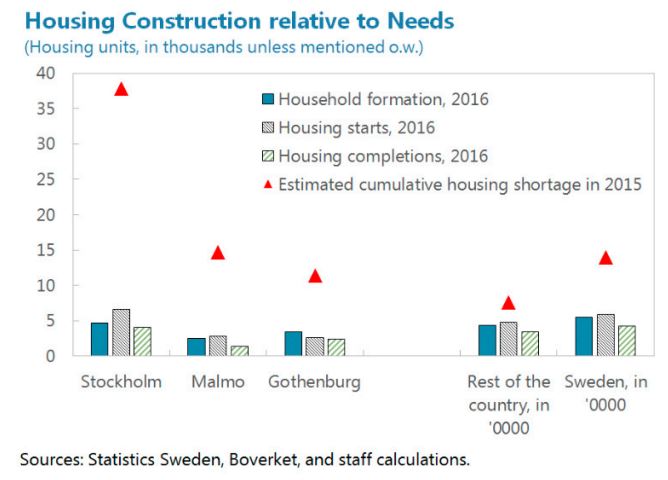

“Policies to bolster construction are welcome yet are unlikely to be sufficient to rebalance the housing market. The government targets building 250,000 dwellings during 2015– 20, including by subsidizing (0.1 percent of GDP) construction of affordable rental housing—which meets energy efficiency and rent limit requirements—and through state financing to municipalities for infrastructure related to housing development. Although construction has risen (…), housing starts only modestly exceed estimated household formation in most of the country, indicating that shortages will persist. Moreover, due to high land prices and construction costs, new development has been focused on the high-end of the market or located in more remote areas.”

“Improving housing affordability should be a central priority, supported by deep structural reforms to promote more efficient use of existing property:

- Sustaining housing supply. High construction costs in Sweden need to be addressed by streamlining building regulations and promoting competition in the sector, including by harmonizing fragmented planning and approval processes. Improving public transportation within regions would help relieve demand pressures in major centers. Budgetary support for construction of rental housing that meets affordability tests should be expanded.

- Phasing out rent control. Providing incentives to better match housing to household needs will effectively increase supply in areas with high demand. All new construction of rental apartments should be fully exempt from controls. Rents on apartments under control should be steadily aligned with market rates, with low-income households protected by the housing allowance.

- Addressing tax incentives. To promote efficient use of space, the composition of property taxes should be shifted by cutting capital gains taxes that deter sales while raising the recurrent property tax, which in 2008 was capped at a level among the lowest in OECD. If the property tax cannot be raised, it becomes more critical to reduce mortgage interest deductibility to ease demand and discourage high leverage. The macroeconomic impact would be modest while interest rates are low and such reforms could be part of a package that benefits households.”

“Authorities’ Views. The authorities recognize the structural challenges in the Swedish housing market, as reflected in the appointment of committees to review the planning and building regulations as well as the model for setting rents on newly produced rental housing. The authorities also recognize the need for further measures to reduce incentives for over-indebtedness. Political opposition to property tax is strong as it is considered to be unfair, and while a lower capital gains tax could improve property turnover, it could have distributional effects favoring older households that had often accumulated significant wealth. The government’s view is that a reduction in mortgage interest deductibility is more feasible if broad political consensus can be reached. With rents on newly-produced rental properties being very high, the government is concerned that a transition to market-based rents would bring high rents, and it also has doubts that the supply of rental housing within the reach of lower income households would increase significantly. The Riksbank, on the other hand, stresses that a more market-based rent system would increase supply, benefitting young people.”

From IMF’s latest report on Sweden:

“The Swedish housing market has deep structural problems. Large house price increases were necessary to overcome the hurdle of high construction costs before construction began rising. These costs reflect a combination of complex building regulations and limited competition in the sector owing to cumbersome municipal land sale and planning and approval procedures. The resulting supply shortfalls are present in 255 out of 290 municipalities, but are mostly in the three major metropolitan areas (Stockholm,

Posted by at 1:29 PM

Labels: Global Housing Watch

Friday, November 17, 2017

Growth and Jobs in Developing Economies: Trends and Cycles

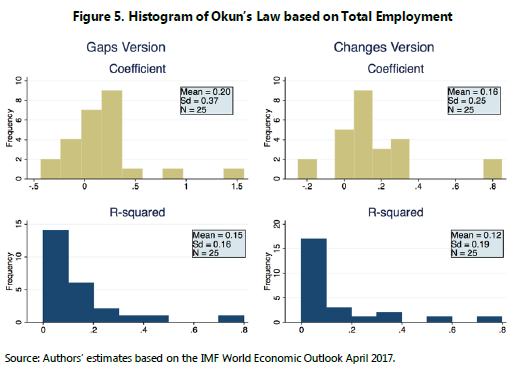

A new IMF working paper investigates the relationship between economic growth and job creation in developing economies with a focus on low and lower middle-income countries along two dimensions: growth patterns and short-run correlations. Analysis on growth patterns shows that regime changes are quite common in both economic growth and employment growth, yet they are not synchronized with each other. Okun’s Law—the short-run relationship between output and labor market—holds in half of the countries in our sample and shows considerable cross-country heterogeneity.

A new IMF working paper investigates the relationship between economic growth and job creation in developing economies with a focus on low and lower middle-income countries along two dimensions: growth patterns and short-run correlations. Analysis on growth patterns shows that regime changes are quite common in both economic growth and employment growth, yet they are not synchronized with each other. Okun’s Law—the short-run relationship between output and labor market—holds in half of the countries in our sample and shows considerable cross-country heterogeneity.

Posted by at 5:20 PM

Labels: Inclusive Growth

Housing View – November 17, 2017

On cross-country:

- 8th Global Housing Finance Conference (May 30-June 01, 2018) – World Bank

- How Cities Are Tightening the Leash on Airbnb – Citylab

- Housing policy and marriage: evidence from Egypt, Jordan and Tunisia – Economic Research Forum

On the US:

- Implications of US Tax Policy for House Prices, Rents, and Homeownership – American Economic Review

- America’s Republicans take aim at mortgage subsidies – Economist

- How Many Hours Americans Need to Work to Pay Their Mortgage – Visual Capitalist

- Labor Market Improvement and the Use of Subsidized Housing Programs – Federal Reserve Bank of Kansas City

- Stuck in Subprime? Examining the Barriers to Refinancing Mortgage Debt – Federal Reserve Bank of Philadelphia

- Home Equity Wealth at New High – HousingViews

- Low-Income Housing Tax Credit: Costly, Complex, and Corruption-Prone – Cato Institute

- Bank Think Mortgage deduction helps housing lobby, but not homeowners – American Banker

- New research says it’s better to buy than rent—and it has nothing to do with money – Quartz

On other countries:

- [Australia] A rare dose of honesty in the housing affordability debate – MacroBusiness

- [Canada] Immigration, Capital Flows, and Housing Prices – British Columbia

- [Canada] Vancouver Limits Airbnb, in an Effort to Combat Its Housing Crisis – New York Times

- [Germany] Ticking time-bomb lies under Berlin’s property market – Financial Times

- [Germany] Spreading housing shortage hits over 850,000 people in Germany – Reuters

- [India] Home Price Rises Slow in India Thanks to Modi’s Cash Ban – Bloomberg

- [Ireland] Irish house prices: Déjà vu all over again? – Economic & Social Research Institute

- [Netherlands] Amsterdam returns Dutch house prices to 2008 highs – Financial Times

- [Sweden] UPDATE 3-Sweden’s FSA proposes tighter mortgage rules as housing market slows – Reuters

- [Sweden] Sweden’s big banks call an end to decades-long housing boom – Financial Times

- [Sweden] The Shock of Sweden’s Housing Market is Hitting the Country’s Currency – Bloomberg

- [United Kingdom] However you analyse it, housing in Britain is a mess – Financial Times

- [United Kingdom] Solving UK housing crisis requires more than new homes – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- 8th Global Housing Finance Conference (May 30-June 01, 2018) – World Bank

- How Cities Are Tightening the Leash on Airbnb – Citylab

- Housing policy and marriage: evidence from Egypt, Jordan and Tunisia – Economic Research Forum

On the US:

- Implications of US Tax Policy for House Prices, Rents, and Homeownership – American Economic Review

- America’s Republicans take aim at mortgage subsidies – Economist

- How Many Hours Americans Need to Work to Pay Their Mortgage – Visual Capitalist

- Labor Market Improvement and the Use of Subsidized Housing Programs – Federal Reserve Bank of Kansas City

- Stuck in Subprime?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, November 16, 2017

Inequality in Financial Inclusion, Gender Gaps, and Income Inequality

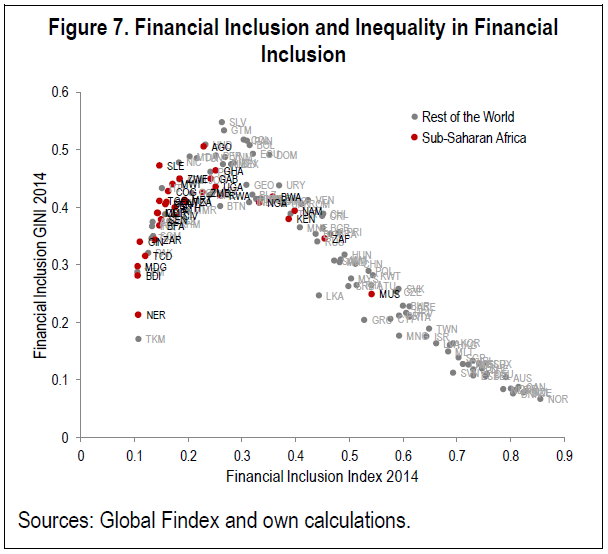

From a new IMF working paper:

“We investigate the link between gender inequality in financial inclusion and income inequality, with three contributions to the recent literature. First, using a micro-dataset covering 146,000 individuals in over 140 countries, we construct novel, synthetic indices of the intensity of financial inclusion at the individual and country level. Second, we derive the distribution of individual financial access “scores” across countries to document a “Kuznets”-curve in financial inclusion. Third, cross-country regressions confirm that our measure of inequality in financial access is significantly related to income inequality, above and beyond other factors previously highlighted in the literature.”

From a new IMF working paper:

“We investigate the link between gender inequality in financial inclusion and income inequality, with three contributions to the recent literature. First, using a micro-dataset covering 146,000 individuals in over 140 countries, we construct novel, synthetic indices of the intensity of financial inclusion at the individual and country level. Second, we derive the distribution of individual financial access “scores” across countries to document a “Kuznets”-curve in financial inclusion.

Posted by at 10:32 PM

Labels: Inclusive Growth

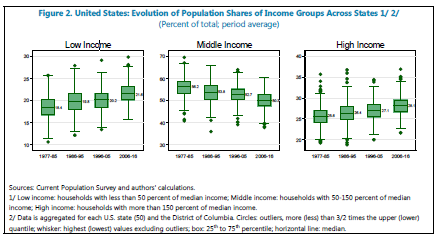

Hollowing Out: The Channels of Income Polarization in the United States

From a new IMF working paper:

“Data show that middle-income households have continued to move down, and less so up, the income distribution in the United States since the 1970s—a phenomenon that is often referred to as the polarization or “hollowing out” of the income distribution. While the level of income polarization is generally lower in the richer states (defined as those with higher median household income levels), there have been wide variations in income polarization over time and across states. We develop two indices to measure income polarization, including a novel hollowing-out index. We also examine the proximate causes of income polarization, using an econometric analysis at both state and household levels. The results suggest that technology, measured by job routinization, and international trade, measured by job offshoring, can explain more than half of the rise in income polarization, with broadly equal contributions. Household characteristics, particularly better education, have had important countervailing effects on income polarization. Policies should continue promoting technological progress and international trade, but also recognize that these positive forces have important side-effects on the income distribution and household welfare that need to be understood and mitigated.”

From a new IMF working paper:

“Data show that middle-income households have continued to move down, and less so up, the income distribution in the United States since the 1970s—a phenomenon that is often referred to as the polarization or “hollowing out” of the income distribution. While the level of income polarization is generally lower in the richer states (defined as those with higher median household income levels), there have been wide variations in income polarization over time and across states.

Posted by at 11:04 AM

Labels: Inclusive Growth

Subscribe to: Posts