Tuesday, May 9, 2017

Macroprudential Policy in New Zealand

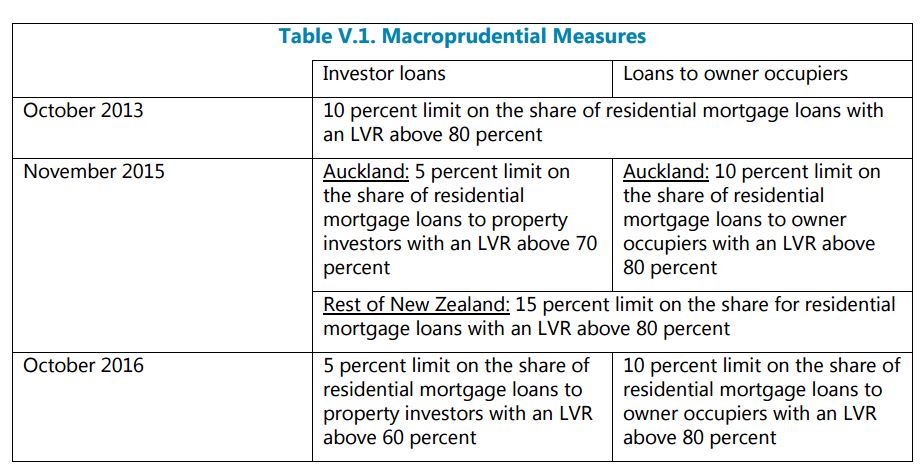

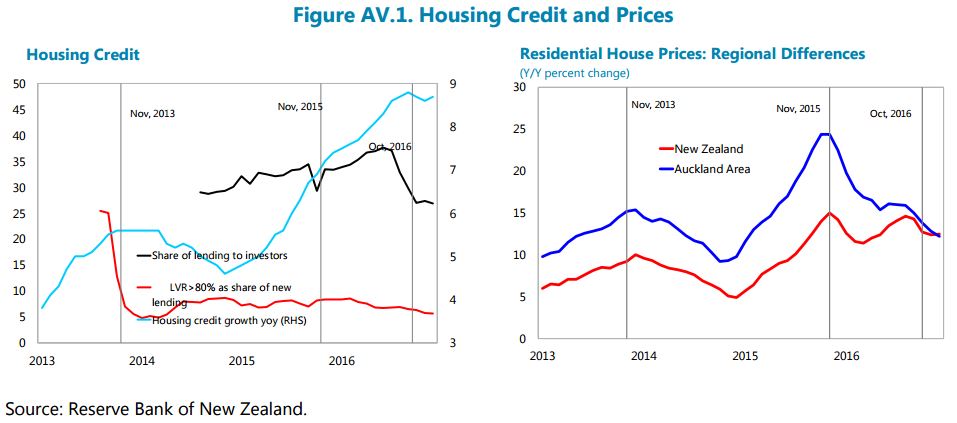

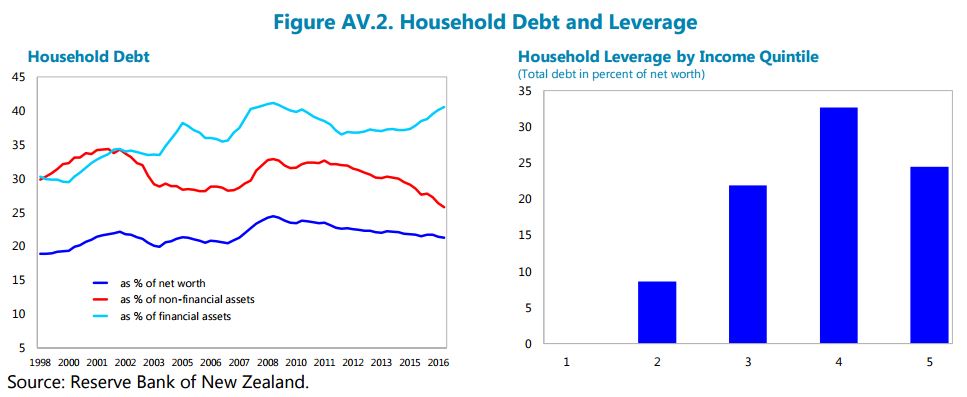

A new IMF report on New Zealand says that “New Zealand’s mainly LVR-related housing market-specific macroprudential measures would appear to have had some moderating influence on mortgage lending, expected and actual house price growth, and the quality of loan composition. In addition, they have also helped to contain household leverage. However, they do not seem to have prevented a continuous deterioration of borrower households’ vulnerability against debt servicing capacity risks, such as higher interest rates or income shocks.”

Also, see a separate IMF report on New Zealand’s financial sector, which also discusses the housing market.

A new IMF report on New Zealand says that “New Zealand’s mainly LVR-related housing market-specific macroprudential measures would appear to have had some moderating influence on mortgage lending, expected and actual house price growth, and the quality of loan composition. In addition, they have also helped to contain household leverage. However, they do not seem to have prevented a continuous deterioration of borrower households’ vulnerability against debt servicing capacity risks, such as higher interest rates or income shocks.”

Posted by at 10:51 AM

Labels: Global Housing Watch

Monday, May 1, 2017

House Prices in Malaysia

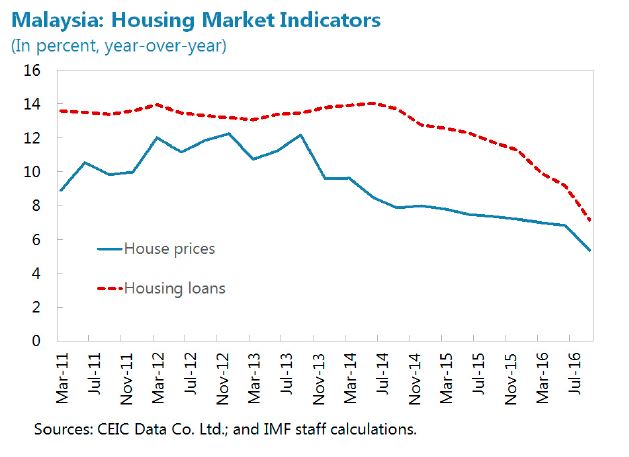

“Risks associated with the housing market appear to be receding. House price growth has moderated, following several years of elevated growth, and risks are circumscribed by ongoing supply constraints, increases in public sector wages, and, from a more structural perspective, Malaysia’s relatively young labor force and urbanizing population. The risk of a sharp decline in house prices should nevertheless be carefully monitored. If rapid house price growth resumes, LTV caps on second and first mortgages could be considered”, says IMF’s latest report on Malaysia.

“Risks associated with the housing market appear to be receding. House price growth has moderated, following several years of elevated growth, and risks are circumscribed by ongoing supply constraints, increases in public sector wages, and, from a more structural perspective, Malaysia’s relatively young labor force and urbanizing population. The risk of a sharp decline in house prices should nevertheless be carefully monitored. If rapid house price growth resumes, LTV caps on second and first mortgages could be considered”,

Posted by at 1:32 PM

Labels: Global Housing Watch

Subscribe to: Posts