Tuesday, October 4, 2016

Jobs and Growth: Outlook and Policy Response

My talk today to the Parliamentary Network of the IMF and the World Bank, a group I always enjoy talking to. This time they had really good questions on the IMF position on public infrastructure. And many of them even asked me why the Okun elasticity differs across countries – what more could a nerd ask for?

My talk today to the Parliamentary Network of the IMF and the World Bank, a group I always enjoy talking to. This time they had really good questions on the IMF position on public infrastructure. And many of them even asked me why the Okun elasticity differs across countries – what more could a nerd ask for?

Posted by at 11:14 AM

Labels: Inclusive Growth

Monday, October 3, 2016

Financial Globalization, Inequality and the Top 1%

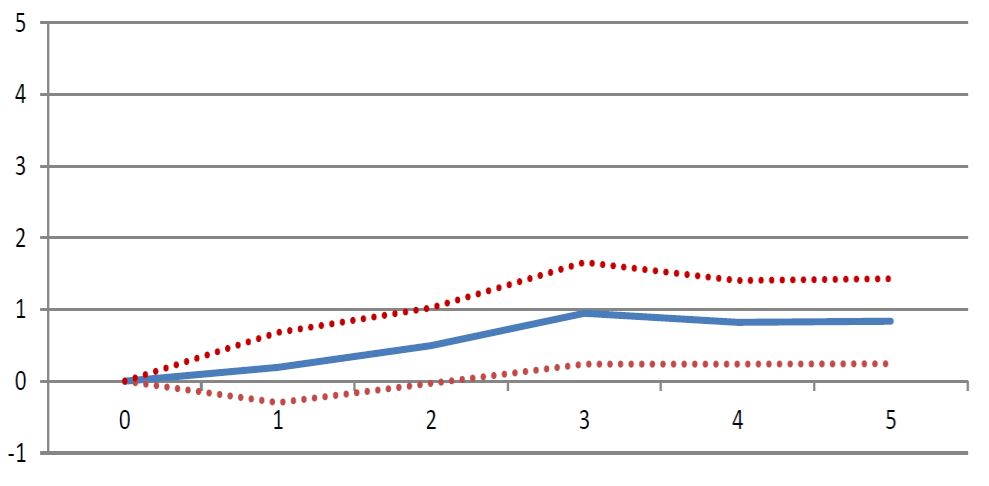

Davide Furceri and I have revised our IMF Working Paper on the impacts of financial globalization—specifically, the elimination of restrictions on the capital account—on inequality. We find that episodes of capital account liberalization are followed by an increase in the share of income going to the top 1% (the chart below shows the impact). Our previous work had already shown that the Gini coefficient increases following capital account liberalization. The details, and several other new results, are given in the revised paper.

Davide Furceri and I have revised our IMF Working Paper on the impacts of financial globalization—specifically, the elimination of restrictions on the capital account—on inequality. We find that episodes of capital account liberalization are followed by an increase in the share of income going to the top 1% (the chart below shows the impact). Our previous work had already shown that the Gini coefficient increases following capital account liberalization. The details, and several other new results,

Posted by at 1:28 PM

Labels: Inclusive Growth

IMF Research on Inequality: A Primer

The IMF’s recent research on inequality has attracted a lot of (mostly favorable) attention. My talk to CSOs today describes the main findings of this research. Focusing on within-country inequality, I classify the work into three categories: causes, consequences, cures.

- On causes, the main finding is that—in addition to broad trends like trade, technology and demographics—inequality is driven by economic policies. This is not an earth-shattering finding but it is an important one. The policies that turn out to drive inequality include fiscal policies, capital account liberalization (i.e. policies to foster mobility of capital across national boundaries) and labor market policies. Many of these are ‘bread-and-butter’ issues for the IMF, ones on which it routinely gives advice to its member countries.

- On consequences, there has been a novel research finding: inequality lowers the durability of growth spells. This result also puts inequality squarely with the remit of the IMF’s work: fostering sustained growth, a goal of IMF advice, requires some attention to inequality.

- As it should, the work on cures follows from what has been learnt about the causes and consequences. To take an example: if fiscal policies are a cause of inequality, the IMF’s advice on the design of these polices needs to account for this fact. This is both because the distributional consequences may be important in their own right to some governments and because—as noted—they can have an adverse effect on the sustainability of growth. One new research finding, which has implications for the design of many policies, is that redistribution, unless extreme, does not have an adverse impact on growth; hence redistribution need not be feared as a cure.

Details and links to the underlying papers are given in this PPT.

The IMF’s recent research on inequality has attracted a lot of (mostly favorable) attention. My talk to CSOs today describes the main findings of this research. Focusing on within-country inequality, I classify the work into three categories: causes, consequences, cures.

- On causes, the main finding is that—in addition to broad trends like trade, technology and demographics—inequality is driven by economic policies. This is not an earth-shattering finding but it is an important one.

Posted by at 1:02 PM

Labels: Inclusive Growth

Thursday, September 29, 2016

Macroprudential Policy in Ireland

“The Central Bank of Ireland’s analysis of systemic vulnerabilities is sophisticated and timely. The Central Bank of Ireland has the power to request data directly from regulated entities, and also has powers to require information from unregulated entities under the Central Bank Acts. The Central Bank of Ireland also has powers to change the levels and regulatory perimeter of macroprudential instruments under national law, such as the LTV and LTI limits. There is a dedicated division (Financial Stability Division) that leads systemic risk analysis and macroprudential policy discussions. The biannual Macro-Financial Review (MFR) covers well the stability of individual sectors and property markets. There is, however, still room for further improvement, in particular as to filling data gaps. First, information on domestic and cross-border bilateral liability positions of banks and non-bank financial institutions is still incomplete in places. Second, detailed information on important elements of commercial real estate market activities is lacking. Third, balance sheet data for non-financial corporations is not fully available. Fourth, the absence of a comprehensive credit register precludes the Central Bank of Ireland from connecting credit information of borrowers across financial institutions in Ireland. Moreover, the Macro-Financial Review can usefully cover financial interconnectedness among sectors, as well as within each sector”, according to an IMF report on Ireland.

“The Central Bank of Ireland’s analysis of systemic vulnerabilities is sophisticated and timely. The Central Bank of Ireland has the power to request data directly from regulated entities, and also has powers to require information from unregulated entities under the Central Bank Acts. The Central Bank of Ireland also has powers to change the levels and regulatory perimeter of macroprudential instruments under national law, such as the LTV and LTI limits. There is a dedicated division (Financial Stability Division) that leads systemic risk analysis and macroprudential policy discussions.

Posted by at 2:11 PM

Labels: Global Housing Watch

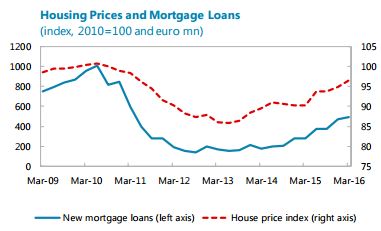

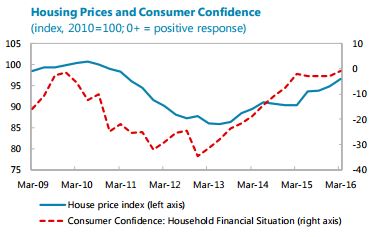

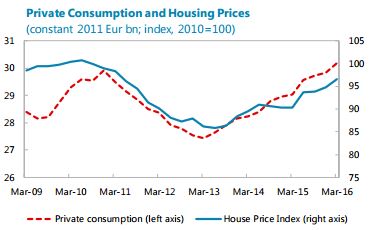

Housing Market in Portugal

“On the real estate side, Portugal has 5.9 million housing units with an estimated value of €300 billion. House prices rose 9.9 percent between 2013Q1 and 2015Q4. Accordingly, the estimated value of the real estate assets owned by households increased by €25 billion, while household savings declined by €5 billion”, notes IMF report on Portugal.

“On the real estate side, Portugal has 5.9 million housing units with an estimated value of €300 billion. House prices rose 9.9 percent between 2013Q1 and 2015Q4. Accordingly, the estimated value of the real estate assets owned by households increased by €25 billion, while household savings declined by €5 billion”, notes IMF report on Portugal.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts