Thursday, February 11, 2016

House Prices in the Netherlands

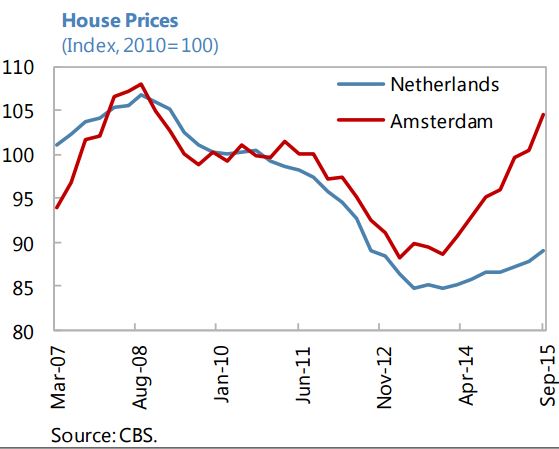

Moreover, the report notes that “House prices have started to recover. However, they remain well below peak levels. Prices have risen by more than 5 percent since the 2013 trough, but they are still 17 percent below their 2008 peak in 2015:Q3. More than a quarter of Dutch households have mortgage debt in excess of the house value, primarily among younger households. The recovery in housing prices is uneven. The market is buoyant in Amsterdam, where house prices are less than 4 percent below the 2008 peak, and to a lesser extent in other major cities. However, house price increases are more subdued in outlying areas.”

“The turnaround in house prices presents an opportunity to implement policies to better insulate Dutch households and the overall economy from the effect of future house price declines and remove some of the incentives for excessive leverage—thereby reducing the likelihood and intensity of boom-bust cycles”, according to the IMF’s report on the Netherlands.

Moreover, the report notes that “House prices have started to recover. However, they remain well below peak levels. Prices have risen by more than 5 percent since the 2013 trough,

Posted by at 6:57 PM

Labels: Global Housing Watch

House Prices in New Zealand

A separate IMF paper “analyzes long-run trends in house prices and household debt in New Zealand. The key findings are that economic fundamentals such as financial liberalization, lower interest rates, demographics and supply constraints are important factors in the large run up in house prices. Although higher house price and household debt can largely be explained, it still has implications for financial stability.”

“House price inflation in Auckland has remained high. House prices in Auckland (where about one-third of the population lives) have continued their strong upward trend, rising by 22.5 percent (y/y) in December 2015, and the housing inventory available for sale remains low. Moreover, prices in neighboring areas are beginning to accelerate as buyers are priced out of the Auckland market. Supply shortages are a fundamental driver of house price inflation, exacerbated by high net immigration. On the demand side, Read the full article…

Posted by at 6:45 PM

Labels: Global Housing Watch

House Prices in Morocco

“There is little evidence of a housing bubble, as the price increase over the past 10 years appears modest relative to nominal GDP growth”, according to IMF’s report on Morocco. The report also notes that “Several prudential tools have been used to manage systemic risk. A code of ethics was adopted by banks in 2008 to tighten lending standards for real estate. In addition, an increased tax on nonprimary housing was used to discourage speculative house purchases in 2006–08. Read the full article…

Posted by at 6:32 PM

Labels: Global Housing Watch

Monday, February 1, 2016

A Groundhog Day Tradition: The Stekler Award for Courage in Forecasting

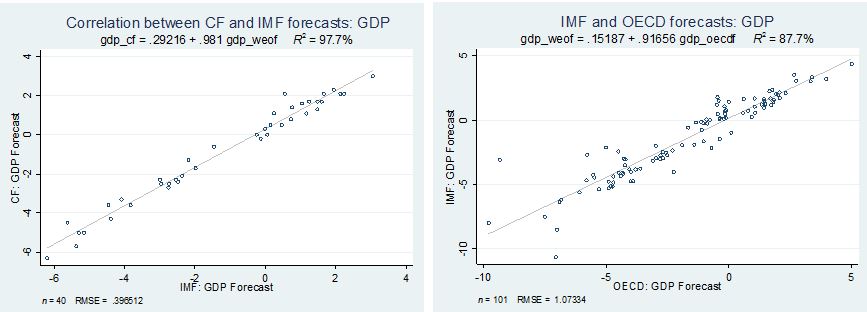

The Stekler Award is named after the famous forecasting expert and academic Herman Stekler who believes that recessions should be forecast “early and often.” In practice, recessions are almost never forecast in advance. The Economist recently re-discovered this long-standing finding and highlighted the poor record of the IMF in forecasting recessions. The record of other public institutions or the private sector is just as poor. For instance, see the charts below on forecasts made by the IMF, OECD and the private sector (labeled ‘CF’ in the charts) over the course of 2009—each point shows the forecast for a particular country. The forecasts are virtually identical. And the forecasts for recessions (negative growth) were not made in advance by any of the sources.

The race is on for the 2017 award. Suggestions are welcome and can be sent to ploungani@gmail.com. The Stekler Award recognizes forecasts that depart significantly from the consensus view. Predictions need not be restricted to forecasts of recessions but they must be specific (so “oil prices will rebound someday” doesn’t cut it) and well reasoned (so no “we have been on the path to doom which is bound to come one day”-type of forecasts).

We mined a recent article in Politico to see if we could get some front runners for the 2017 award. There were a range of predictions, some quite clever (Dean Baker predicted that during 2016, unlike 2015, oil prices would not fall another $60 a barrel), some specific (Ann Harrison predicts that “India will replace China as the leading destination for foreign investment” in 2016), most quite gloomy. On the U.S. economy in 2016, most experts surveyed stuck to the center, though Robert Reich said: “I expect the U.S. economy to sputter in 2016”; if he’d been a little more specific he ‘coulda been a contender’.

The 2016 Stekler Award for Courage in Forecasting goes to Michael (“Mish”) Shedlock. At the start of 2015, the blogger popularly known as “Mish” had predicted recessions in Canada and the United States during 2015. While these events did not come to pass, enough anxiety was generated about the health of these economies over the course of the year that Mish deserves some credit for anticipating a degree of weakness that was not being widely talked about at the start of last year. Read the full article…

Posted by at 6:21 PM

Labels: Forecasting Forum

Friday, January 29, 2016

The Unemployment Picture in 2016

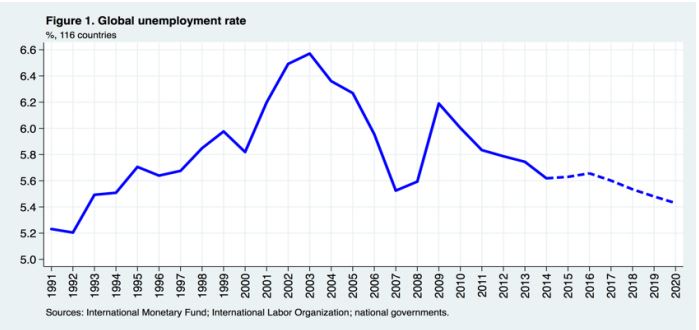

Figure 1 provides a measure of the global unemployment rate based on data for 116 countries, of which 37 countries are classified as ‘advanced’ (i.e. high-income) countries and the remaining 79 as ‘emerging market and developing economies.’ (We refer to the second group using the acronym ‘EMDE’.)

Let’s begin with how the global unemployment picture looked before the IMF’s January 2016 WEO Update. Figure 1 provides a measure of the global unemployment rate based on data for 116 countries, of which 37 countries are classified as ‘advanced’ (i.e. high-income) countries and the remaining 79 as ‘emerging market and developing economies.’ (We refer to the second group using the acronym ‘EMDE’.) Focusing on the recent cycle, global unemployment rate peaked in 6.2 percent in 2009 and has since been returning slowly to its pre-crisis level. Over the coming year, the global unemployment rate is expected to go up slightly.

To understand where this increase is coming from, Figure 2 shows the unemployment rate for the two main groups of countries separately. This reveals that the increase comes from the emerging markets and developing countries (EMDE) group. Moreover, the increase in unemployment among this group occurs because of the expected increase in unemployment among fuelexporting countries (Figure 3).

How will the growth revisions affect the unemployment picture?

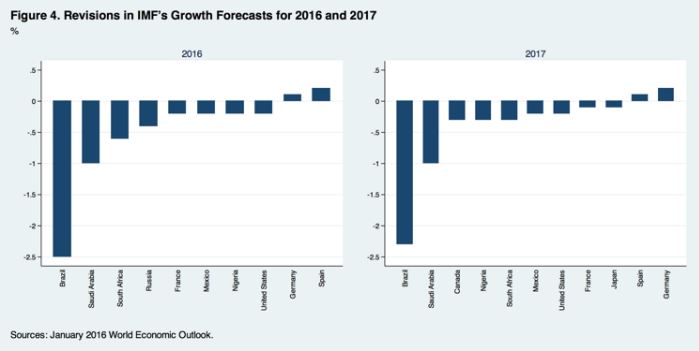

Now let’s consider how the revisions to the growth forecasts that the IMF announced in the January 2016 WEO Update could change the unemployment picture. At the global level, the forecast for GDP growth in 2016 was revised down by 0.2 percent, which would in turn increase the global unemployment rate only a little bit above the path projected in Figure 1. However, for some countries the revisions in growth forecasts are larger, as shown in Figure 4 below. The biggest change is in Brazil, followed by Saudi Arabia, South Africa and Russia.

Continue reading here.

From the International Jobs Report–January 2016

Figure 1 provides a measure of the global unemployment rate based on data for 116 countries, of which 37 countries are classified as ‘advanced’ (i.e. high-income) countries and the remaining 79 as ‘emerging market and developing economies.’ (We refer to the second group using the acronym ‘EMDE’.)

Let’s begin with how the global unemployment picture looked before the IMF’s January 2016 WEO Update.

Posted by at 7:31 PM

Labels: Inclusive Growth

Subscribe to: Posts