Wednesday, March 9, 2016

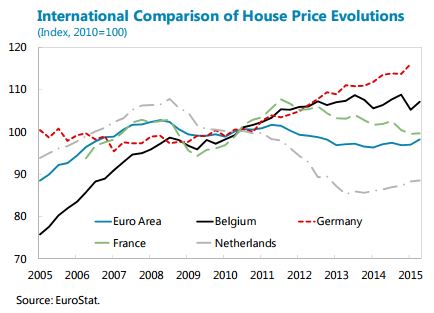

House Prices in Belgium

“After a long period of rapid growth, house prices have stabilized since 2013. A sharp reversal could have a significant impact on consumption, even if banks’ exposures could be managed (…). However, staff analysis does not suggest a major overvaluation, as past price trends were broadly in line with borrowing cost, demographic and income developments”, according to the IMF’s new report on Belgium.

Posted by at 10:00 AM

Labels: Global Housing Watch

Friday, March 4, 2016

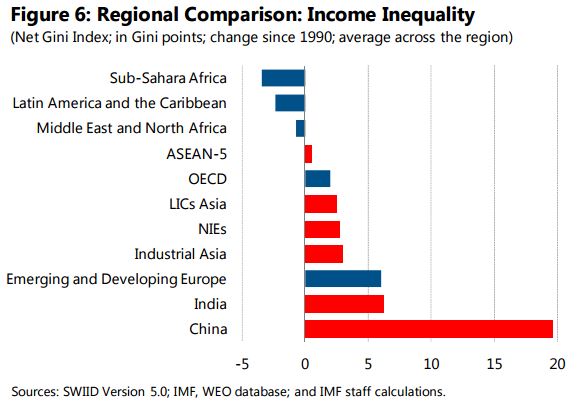

Sharing the Growth Dividend: Analysis of Inequality in Asia

A new IMF “paper focuses on income inequality in Asia, its drivers and policies to combat it. It finds that income inequality has risen in most of Asia, in contrast to many regions. While in the past, rapid growth in Asia has come with equitable distribution of the gains, more recently fast-growing Asian economies have been unable to replicate the “growth with equity” miracle. There is a growing consensus that high levels of inequality can hamper the pace and sustainability of growth. Read the full article…

Posted by at 10:24 PM

Labels: Inclusive Growth

Wednesday, March 2, 2016

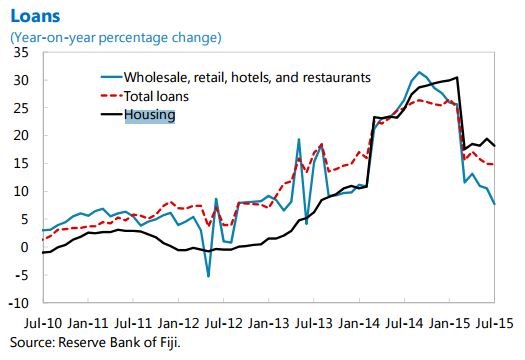

Housing Market in Fiji

“Given still strong credit growth and rapidly rising house prices, the RBF should adopt macroprudential measures to tame the credit and housing price momentum, including through the use of loan-to-value ratios”, says IMF report on Fiji.

Posted by at 10:00 AM

Labels: Global Housing Watch

Monday, February 29, 2016

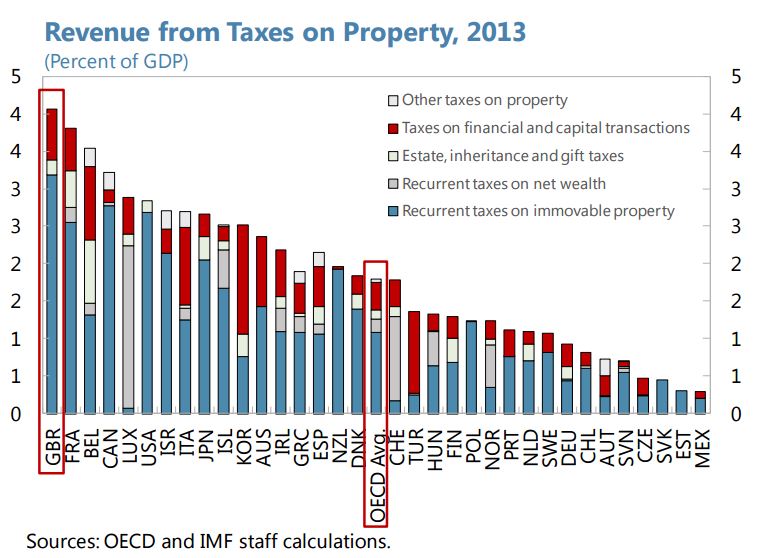

Housing Market in the United Kingdom

A separate IMF paper examines how tax reforms could help ease structural supply constraints in the UK’s housing market. “Property taxation in the UK delivers larger revenue as a percent of GDP than any other OECD country. (…) However, a closer look at the UK’s property tax system suggests that some areas could be reformed to reduce constraints on housing supply and thereby reduce risks stemming from high house prices. In particular, deducing council tax discounts [and (…)] reducing reliance on the stamp duty land tax.”

“Housing markets have decelerated somewhat since mid-2014, but significant pressures remain. (…) Persistent upward pressure on house prices partly reflects supply constraints. (…) High house prices result in some households taking on high leverage, posing financial stability risks. (…) Further macroprudential tightening may thus be needed if the reduction in high leverage mortgages does not continue”, says the IMF’s new report on the United Kingdom.

A separate IMF paper examines how tax reforms could help ease structural supply constraints in the UK’s housing market.

Posted by at 10:00 AM

Labels: Global Housing Watch

Thursday, February 25, 2016

Inequality and opening up to foreign capital and inequality: some new results

In June 1979, shortly after winning a landmark election, Margaret Thatcher eliminated restrictions on “the ability to move money in and out” of the United Kingdom, which some of her supporters regard as “one of her best and most revolutionary acts” (Heath, 2015).

Thatcher’s critics [have] regarded this same liberalization as starting a global trend whose “downside . . . proved to be painful” (Schiffrin, 2016). In their view, while the free mobility of capital across national borders confers many benefits in theory, in practice liberalization has often led to economic volatility and financial crisis. This in turn has adverse consequences for many in the economy, particularly for those who are not well off. Liberalization also affects the relative bargaining power of companies and workers (that is, of capital and labor, respectively, in the jargon of economists) because capital is generally able to move across national boundaries with greater ease than labor. The threat of being able to move production abroad reduces labor’s bargaining power and the share of the income pie that goes to workers.

In studying such distributional effects of capital account liberalization, Davide Furceri and I found that after countries take steps to open their capital account, an increase in inequality in incomes within countries follows (Furceri and Loungani, 2015). The impact is greater when liberalization is followed by a financial crisis and in countries where there is low financial development—that is, where financial institutions are small and access to these institutions is limited. We also find that the share of income going to labor declines in the aftermath of liberalization. Thus, like trade liberalization, capital account liberalization can lead to winners and losers. But while the distributional effects of trade have long been studied by economists, the distributional impacts of opening the capital account are just starting to be analyzed.

Read the rest of this (non-technical) summary of our results here: http://www.imf.org/external/pubs/ft/fandd/2016/03/furceri.htm

Here’s a link to the IMF Working Paper: http://www.imf.org/external/pubs/ft/wp/2015/wp15243.pdf

Earlier versions of this research, based on data for advanced economies, were featured on Krugman’s blog and in VoxEU. These new results extend our results to developing economies as well as lay out possible channels through which capital account liberalization leads to inequality.

After countries remove restrictions on capital flows, inequality often gets worse

In June 1979, shortly after winning a landmark election, Margaret Thatcher eliminated restrictions on “the ability to move money in and out” of the United Kingdom, which some of her supporters regard as “one of her best and most revolutionary acts” (Heath, 2015).

Thatcher’s critics [have] regarded this same liberalization as starting a global trend whose “downside . .

Posted by at 4:11 PM

Labels: Inclusive Growth

Subscribe to: Posts