Wednesday, March 23, 2016

Monetary Policy and Financial Stability: Canada’s House-Price Dilemma

Canada’s housing market is sizzling hot and the Bank of Canada has a monetary policy dilemma: increase interest rates to cool the housing market would hurt borrowers and the economy; keep interest rates low adds fuel to the borrowing that led to the rise in housing prices and in household debt. What to do?

Housing headache

The latest national data on house prices in February suggest a year-on-year increase of 9 percent. House prices in Vancouver and Toronto—that contribute about a third of Canada’s GDP—have led the increase.

Canada’s housing boom has been accompanied by a steady rise in the nation’s household debt to 165 percent of disposable income by the end of 2015 (see chart). One way to cool the housing sector is to increase interest rates, but that would hurt the slowing economy, which has been hit hard by the decline in oil prices. Hence, the dilemma.

Low mortgage rates are an important factor feeding the housing market boom. This has helped keep interest payments low even as the size of the average mortgage has risen. As the figure shows, the share of interest payments in households’ disposable income has declined from 9 percent in 2008 to 6 percent in 2015, while the average size of mortgages has increased by some 40 percent over the same period. This means more households are able to afford more expensive homes, which, in turn, prompts households to borrow more money and get further into debt, while house prices continue to be pushed upward. This process should continue as long as employment is robust and interest rates remain low.

The Bank of Canada is rightly concerned about the rise in household debt, which makes the economy more vulnerable to unanticipated shocks and financial strains more probable. A mini version of this is playing out in Alberta, which has the third highest level of household debt among the provinces—after British Colombia and Ontario—and was hit by a large terms of trade shock from the oil price decline. The Alberta economy is expected to have contracted by almost 2 percent last year amid massive layoffs by the oil industry and house prices fell by 4 percent since their peak in late 2014.

Continue reading here.

Via iMFdirect:

Canada’s housing market is sizzling hot and the Bank of Canada has a monetary policy dilemma: increase interest rates to cool the housing market would hurt borrowers and the economy; keep interest rates low adds fuel to the borrowing that led to the rise in housing prices and in household debt. What to do?

Housing headache

The latest national data on house prices in February suggest a year-on-year increase of 9 percent.

Posted by at 9:00 AM

Labels: Global Housing Watch

Monday, March 21, 2016

Financial Stability and Interest-Rate Policy

The paper notes that “At the current conjuncture Canada represents an interesting case: Monetary policy faces the dilemma of supporting a struggling economy by cutting interest rates and maintaining financial stability in a context of high household debt and ever growing housing prices.”

The paper’s “findings show that it is very unlikely that the benefits of having a meaningfully tighter policy (i.e., at least 25 basis points higher than otherwise) would outweigh its costs, in the current Canadian context. In fact, even though the interest rate increase reduces the growth of real household credit and house prices and the ratio of household debt to GDP, the reduction in the crisis probability is minor and peaks only after about 8 years. At the same time, costs are front loaded and magnified by the tighter economic conditions. The policy rate path which takes into account financial stability risks is, thus, only 6 basis points higher than otherwise (for 8 quarters)—which, quantitatively, is not a meaningful policy alternative. A policy rate that is 25 basis points higher than otherwise (for 8 quarters) is expected to be welfare improving only under a scenario where a crisis would impose severe costs on the economy and real credit is expected to grow (in absence of policy intervention) at or above 9 percent a year for the next 3 consecutive years.”

“Should monetary policy use its short-term policy rate to stabilize the growth in household credit and housing prices with the aim of promoting financial stability? (…) the answer is no— especially when the economy is slowing down”, according to a new IMF working paper by Andrea Pescatori and Stefan Laseen–Financial Stability and Interest-Rate Policy: A Quantitative Assessment of Costs and Benefits.

The paper notes that “At the current conjuncture Canada represents an interesting case: Monetary policy faces the dilemma of supporting a struggling economy by cutting interest rates and maintaining financial stability in a context of high household debt and ever growing housing prices.”

Posted by at 7:50 PM

Labels: Global Housing Watch

Thursday, March 17, 2016

Make in India: Which exports can drive the next wave of growth?

Structural transformation depends not only on how much countries export but also on what they export and with whom they trade. In my new IMF working paper with Rahul Anand and Kalpana Kochhar, we break new grounds in analyzing India’s exports by the technological content, quality, sophistication, and complexity of India’s export basket. The paper can be found here. Here are few key pieces of evidence from our paper:

Technological content of India’s exports

The evolution of Indian exports has not followed a “textbook” pattern. The pattern of evolution points to a dichotomy in the Indian economy – a well integrated, technologically advanced services sector and a relatively lagging manufacturing sector. The share of service exports in total exports has grown to over 32 percent in 2013 from 28 percent in 2000. On the other hand, the share of manufacturing exports in total export has declined to 67 percent from nearly 80 percent during 1990-2013.

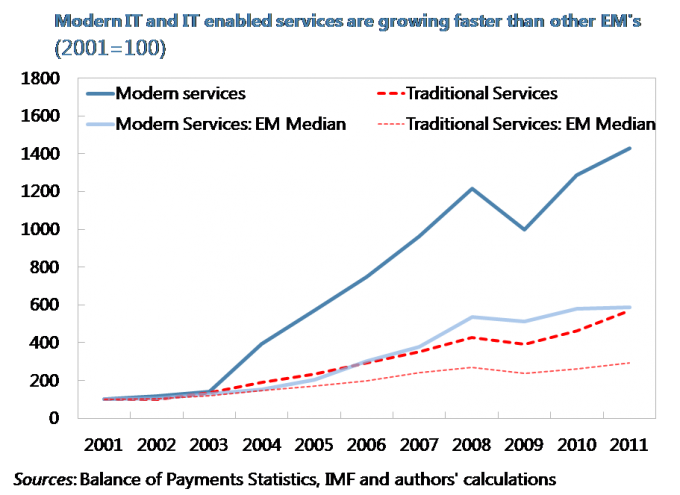

The growth in service exports has been more rapid, resulting in the share of services exports in total exports to increase rapidly over the last decade. This can be explained by technological changes. Many services do not require face-to-face interaction, and can be stored and traded digitally. These services are called modern services. Modern services are the fastest growing sector of the global economy. This is particularly evident in India, where modern services exports account for nearly 70 percent of the total commercial services exports (compared to around 35 percent in EMs) (see Figure 1).

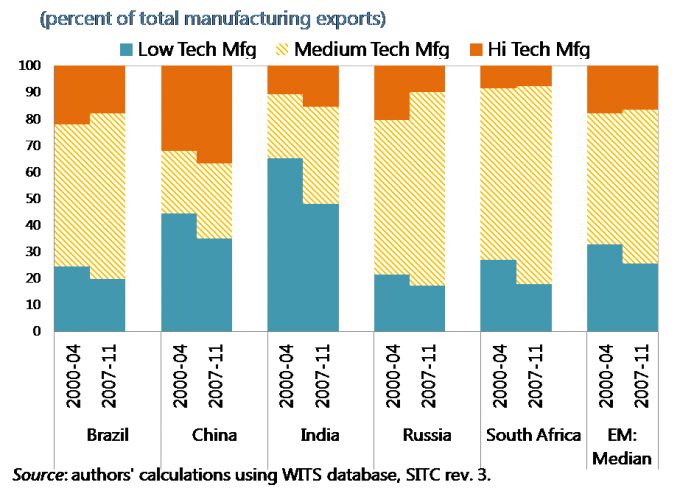

Within manufacturing exports, there is a clear shift away from traditional exports, such as textiles, gems, and leather products, towards high-tech and medium-tech manufacturing products. The relative share of high-tech manufacturing exports has been increasing (however lower when compared to China or other EMs); Resource based production and low-tech manufacturing dominate the goods export basket (Figure 2).

Manufactured machinery accounts for almost 10 percent, while textile and garments account for more than 15 percent of India’s merchandise exports. In resource-based products – refined petroleum oil, cotton, jewelry of precious metals, and rice – constitute majority of export. In low-tech manufacturing exports – jewelry, textile and apparel based exports constitute the majority of India’s exports. In medium-tech manufacturing – the automotive industry dominates the basket, with machinery, various motor vehicle intermediary inputs for cars, bikes, construction, mining equipment and cosmetics making up the major portion. In the high technology export basket – veterinary and pharmaceutical products, television, telecommunication transistors, aircraft components, X-ray equipment and electronic R&D in electro-medical, power and automotive industry are key elements of the export basket. The main contribution of our work is to comprehensively document Indian exports, which has not been done over the past decade.

Continue reading here.

From Saurabh Mishra:

Structural transformation depends not only on how much countries export but also on what they export and with whom they trade. In my new IMF working paper with Rahul Anand and Kalpana Kochhar, we break new grounds in analyzing India’s exports by the technological content, quality, sophistication, and complexity of India’s export basket. The paper can be found here. Here are few key pieces of evidence from our paper:

Technological content of India’s exports

The evolution of Indian exports has not followed a “textbook” pattern.

Posted by at 8:45 PM

Labels: Uncategorized

Wednesday, March 16, 2016

House Prices in Indonesia

“Property prices have been subdued, in tandem with slowing economic growth and weak business sentiment”, notes IMF’s report on Indonesia.

Posted by at 9:00 AM

Labels: Global Housing Watch

Friday, March 11, 2016

House Prices in Montenegro

“Property prices have continued to fall from their crisis peaks, in part because Russian buying has fallen”, notes the IMF’s report on Montenegro.

Posted by at 10:00 AM

Labels: Global Housing Watch

Subscribe to: Posts