Monday, July 11, 2016

House Prices in Norway

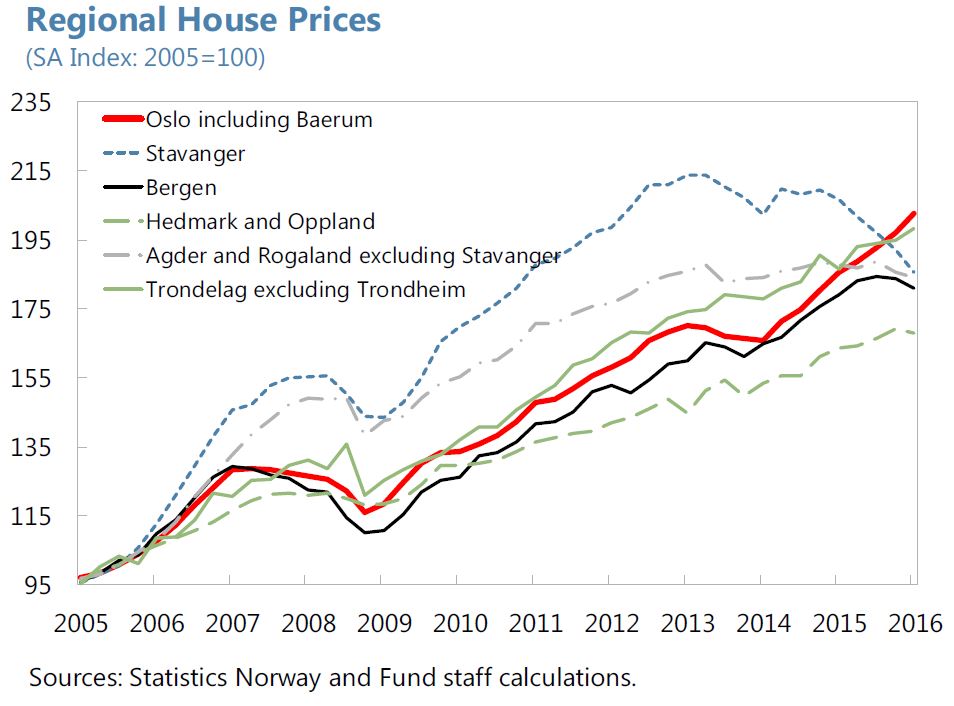

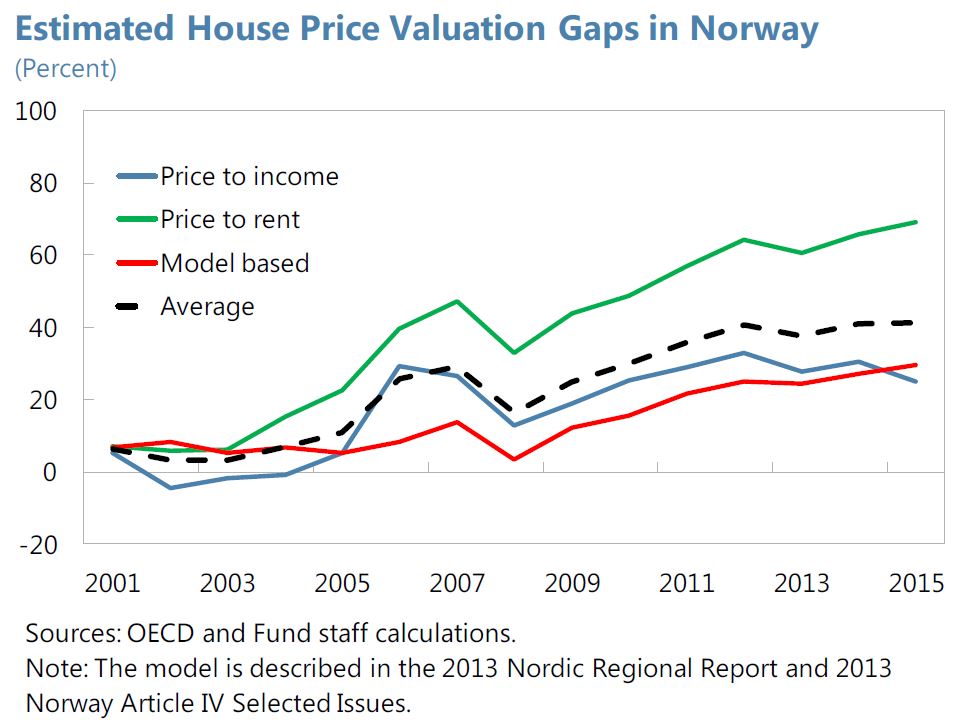

“High and rising house prices and household debt in Norway pose important macro-financial stability risks. Real house prices have risen more than 80 percent in Norway since 2000. Currently, house prices are estimated to be 40 percent overvalued (…) The authorities have introduced a number of measures targeted at the housing market in recent years. (…) Empirical evidence suggests that LTV limits and mortgage risk weights can have significant effects on the growth of mortgage credit and house prices. (…) Results based on a DSGE model suggest that tightening macroprudential measures can reduce household debt ratios with relatively little impact on consumption over the medium-term. (…) Systemic risks from overvalued house prices and high household debt levels suggest that macroprudential policy measures could be tightened further. Addressing structural factors contributing to high household debt and house prices, such as mortgage interest tax deductibility, would reinforce the impact of macroprudential policy measures”, according to the IMF’s report on Norway. See a separate note here on macroprudential policies.

“High and rising house prices and household debt in Norway pose important macro-financial stability risks. Real house prices have risen more than 80 percent in Norway since 2000. Currently, house prices are estimated to be 40 percent overvalued (…) The authorities have introduced a number of measures targeted at the housing market in recent years. (…) Empirical evidence suggests that LTV limits and mortgage risk weights can have significant effects on the growth of mortgage credit and house prices.

Posted by at 5:00 AM

Labels: Global Housing Watch

Saturday, July 9, 2016

Female Labor Force Participation in Poland

An IMF report notes: “Poland is facing a rapidly aging population, which is expected to weigh on public finances and economic growth. Yet, there is an important underutilized source of qualified labor—Poland’s women. Women in Poland are on average just as educated as men and have a longer potential working lifespan. Nonetheless, female labor force participation is low relative to that for men and low relative to that in many other European countries. Unlocking this valuable source of growth would require leveling the playing field between men and women in the workplace, including by providing high quality affordable childcare for young children, removing tax disincentives for the second earner in a family, and allowing the retirement age to increase as envisaged by the 2013 reforms. For Poland to unleash its full economic potential, it needs to embrace the vital contribution that women can make to its economy.”

An IMF report notes: “Poland is facing a rapidly aging population, which is expected to weigh on public finances and economic growth. Yet, there is an important underutilized source of qualified labor—Poland’s women. Women in Poland are on average just as educated as men and have a longer potential working lifespan. Nonetheless, female labor force participation is low relative to that for men and low relative to that in many other European countries.

Posted by at 6:26 AM

Labels: Inclusive Growth

Friday, July 8, 2016

OPEC’s Strategic Actions and the 2014 Oil Price Crash

A new IMF working paper notes: “In November 2014, OPEC announced a new strategy geared towards improving its market share. Oil-market analysts interpreted this as an attempt to squeeze higher-cost producers including US shale oil out of the market. Over the next year, crude oil prices crashed, with large repercussions for the global economy. We present a simple equilibrium model that explains the fundamental market factors that can rationalize such a “regime switch” by OPEC. These include: (i) the growth of US shale oil production; (ii) the slowdown of global oil demand; (iii) reduced cohesiveness of the OPEC cartel; (iv) production ramp-ups in other non-OPEC countries. We show that these qualitative predictions are broadly consistent with oil market developments during 2014-15. The model is calibrated to oil market data; it predicts accommodation up to 2014 and a market-share strategy thereafter, and explains large oil-price swings as well as realistically high levels of OPEC output.”

A new IMF working paper notes: “In November 2014, OPEC announced a new strategy geared towards improving its market share. Oil-market analysts interpreted this as an attempt to squeeze higher-cost producers including US shale oil out of the market. Over the next year, crude oil prices crashed, with large repercussions for the global economy. We present a simple equilibrium model that explains the fundamental market factors that can rationalize such a “regime switch”

Posted by at 6:06 AM

Labels: Energy & Climate Change

Thursday, July 7, 2016

The Role of Productivity Growth in Reducing Regional Economic Disparities in Poland

Below are extracts from a report written by IMF colleagues: Krzysztof Krogulski, Robert Sierhej, and Aaron Thegeya.

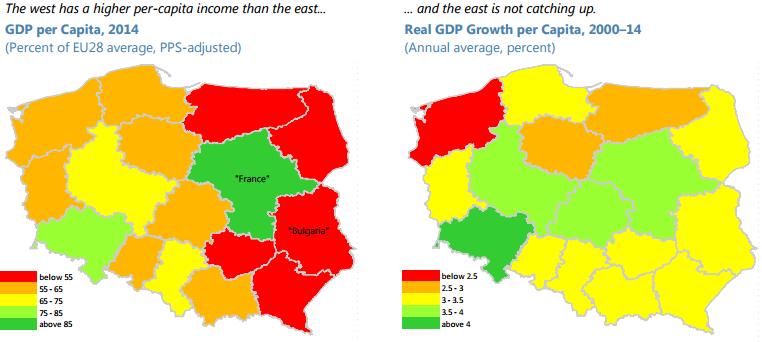

Although Poland has enjoyed strong growth and steady income convergence with the EU over the last two decades, important disparities persist at the regional level. Per-capita income is higher in the west—which is integrated into the German supply chain and enjoys higher levels of FDI—than in the east—where the economy depends more on less productive agriculture. Despite strong overall economic growth, the east has not been catching up to the west. This chapter identifies policies to increase productivity in the east, reduce regional income disparities, and promote overall income convergence. This would require improving educational attainment and reducing skill mismatches in the east, scaling up public infrastructure to attract investment to less productive regions, and facilitating labor mobility.

Despite strong economic performance over the last two decades, there are significant and enduring income disparities between western and eastern regions of Poland. These disparities are strongly correlated with labor productivity differences. While labor productivity growth in poorer eastern regions has been driven significantly by structural transformation, in wealthier western regions it has been driven by higher investment and integration with the German supply chain. Education and labor market conditions had a significant impact on labor productivity growth across regions. Similar growth rates in labor productivity across regions have prevented eastern regions from catching up to western regions.

The analysis of regional productivity determinants points to policies that could be conducive to regional productivity convergence.

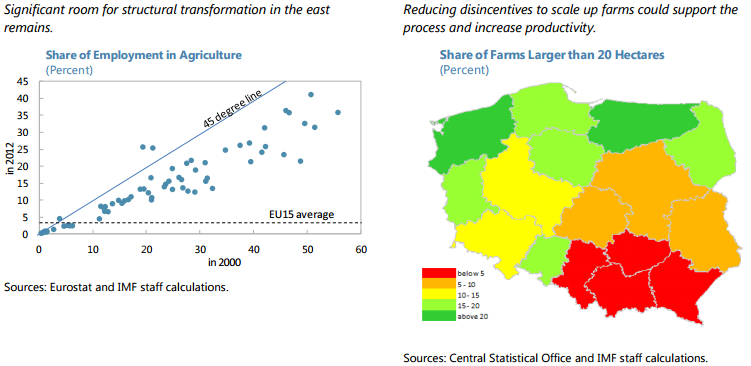

- Support structural transformation and boost productivity in agriculture: Significant room remains to boost labor productivity growth within poorer regions by supporting the reallocation of labor from low-productivity agriculture to higher-productivity industry and service sectors. To unleash the potential for such structural transformation, a review of incentives pertaining to employment in agriculture would be appropriate to identify mechanisms that may encourage people to stay in low productivity farms. In particular, the highly subsidized pension scheme for farmers could be reformed to gradually align it with the regular system to discourage inefficient farming motivated by pension arbitrage. The more productive farms in western regions tend to be larger, so there may be merit in promoting consolidation of agricultural production also in the poorer eastern regions to exploit the economies of scale. In this regard, moving from the current agricultural taxation based on farm size and quality of land to an income-based tax would reduce disincentives to scale up farms and help define the base for social security contributions. To facilitate structural transformation, such reforms should be accompanied with measures to address skill mismatches and bottlenecks in labor mobility, as described below.

- Encourage labor mobility and reduce structural unemployment: Decomposition of productivity growth shows that the contribution from reallocating labor across regions has been relatively minor. This suggests bottlenecks in labor market mobility that could be addressed with proper policies, for example, by improving the functioning of the housing rental market. Currently, the rental housing market in Poland is shallow, discouraging labor relocation. Econometric analysis also suggests that high structural unemployment negatively affects regional productivity growth. While a declining working age population should generally reduce the unemployment rate, addressing high structural unemployment in less productive regions would require greater investment in active labor market policies to improve job searching efficiency across regions, upgrade skills, and reduce skill mismatches.

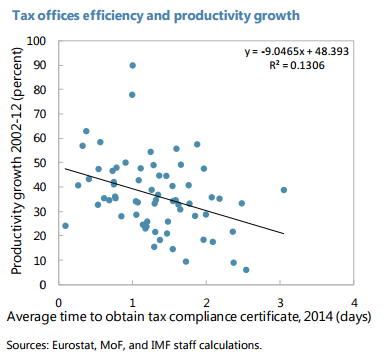

- Attract investments to less productive regions: Empirical findings show that higher FDI is associated with faster regional productivity growth. FDI is more prevalent in wealthier regions, and this pattern needs to change to support regional productivity catch-up. Some factors important for investors could be altered by government policies to support such a change. Specifically, strengthening transportation networks in poorer regions would help, and better targeting of EU funds could support this process. Furthermore, investor surveys suggest that access to skilled labor is important for location of projects. In this context, investing in education and tailoring it to local development needs is important; aligning vocational curricula closely to the needs of industry would facilitate the absorption of new production methods and technologies. While local governments’ role in boosting productivity appears less statistically significant, it does not imply that quality of local administration is irrelevant. For example, data suggest a positive correlation between regional productivity and the efficiency of local tax administration.

Below are extracts from a report written by IMF colleagues: Krzysztof Krogulski, Robert Sierhej, and Aaron Thegeya.

Although Poland has enjoyed strong growth and steady income convergence with the EU over the last two decades, important disparities persist at the regional level. Per-capita income is higher in the west—which is integrated into the German supply chain and enjoys higher levels of FDI—than in the east—where the economy depends more on less productive agriculture.

Posted by at 11:13 AM

Labels: Inclusive Growth

Wednesday, July 6, 2016

Norway: The Transition from Oil and Gas

By IMF colleague: Giang Ho

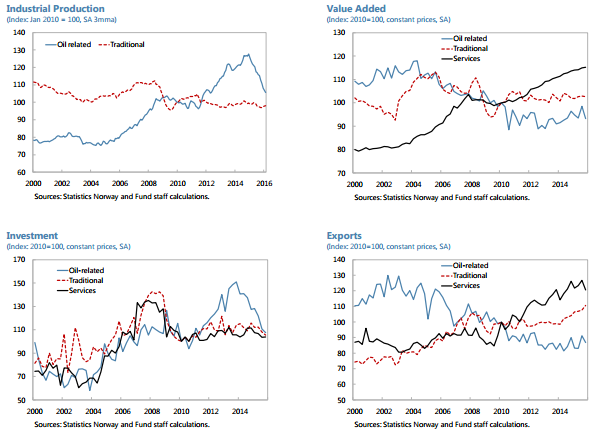

“As offshore investment drops from its peak and oil prices retreat from their high in 2014, the Norwegian economy is going through a transition away from oil dependence,” according to an IMF report. “The transition from oil and gas is a gradual process, and more time would be required before a credible assessment can be made of its progress. The preliminary data show an ongoing marked decline in oil-related production and investment, whereas activity in the traditional goods sector is holding up but not sufficiently to pick up the slack. The divergent performance is perhaps most pronounced within manufacturing between oil-related industries (i.e. machinery and equipment, ships, boats and oil platforms) and nonoil industries. Overall, although the real value added share of the oil-related sector has shrunk from over 36 percent on average during 2000–13 to about 29 percent during 2014–15, much of this appears to have been picked up by the business services sector. The traditional goods producing sector remains a relatively small part of the economy, with value added share at a little over 7 percent and hours worked share declining to 11 percent.”

By IMF colleague: Giang Ho

“As offshore investment drops from its peak and oil prices retreat from their high in 2014, the Norwegian economy is going through a transition away from oil dependence,” according to an IMF report. “The transition from oil and gas is a gradual process, and more time would be required before a credible assessment can be made of its progress. The preliminary data show an ongoing marked decline in oil-related production and investment,

Posted by at 9:02 AM

Labels: Energy & Climate Change

Subscribe to: Posts