Monday, October 10, 2016

Rethinking the Oil Market

by Rabah Arezki

From Project Syndicate

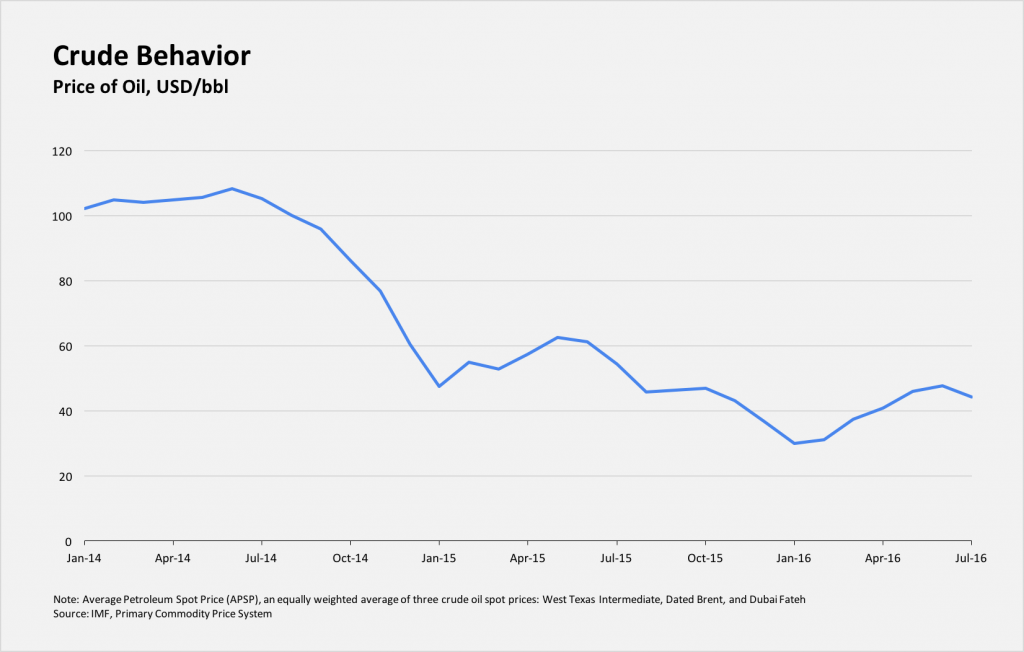

Oil prices have plummeted by about 65% from their peak in June 2014 (see chart below), and there is now intense debate about why. One thing we know for sure is that the oil market has undergone structural changes, thus making this latest episode different from previous dramatic price fluctuations.

The collapse in prices has been driven in part by supply-side factors. These include the United States’ rapid increase in shale-energy production in recent years, and the US government’s decision to end a 40-year crude-oil export ban. Moreover, oil output from war-torn countries such as Libya and Iraq has exceeded expectations, and Iran has returned to world oil markets following its nuclear agreement with the world’s major powers. And Saudi Arabia, the largest member of the Organization of the Petroleum Exporting Countries (OPEC), has increased production to defend its market share.

With this glut in oil, many commentators are now asking if OPEC still matters. High demand for oil since 2000 gave OPEC, and Saudi Arabia in particular, significant influence over prices, but it also spurred investments in higher-cost production methods in other locales, such as oil sands mining in Canada and ultra-deepwater oil extraction in Brazil.

Because of the delay between investment and production for conventional oil production, these projects in non-OPEC countries peaked around the same time the oil market began to slow down, and when expectations about future demand for oil started to falter.

This dynamic prompted OPEC to change its response to price fluctuations. In the past, OPEC, and Saudi Arabia in particular, would stabilize the oil market by cutting production when prices fell too low and increasing output when prices rose too high, relative to OPEC’s price target. This time around, however, at a November 2014 OPEC meeting, Saudi Arabia blocked a motion by other members to reduce production in response to falling prices.

The Saudis have instead boosted output, resulting in immense pressure on higher-cost non-OPEC producers. Saudi Arabia seems to be taking a lesson from a 1986 price-fluctuation event, when massive, unprecedented production cuts in response to increased production by non-OPEC countries failed to stabilize oil prices.

Another factor keeping prices down is that non-OPEC producers have significantly reduced their costs. But this is likely a one-time event. In theory, as the chart below shows, the cost of producing oil is usually assumed to be constant and determined by immutable factors such as the type of oil and the geographical conditions where it is extracted.

Continue reading here.

by Rabah Arezki

From Project Syndicate

Oil prices have plummeted by about 65% from their peak in June 2014 (see chart below), and there is now intense debate about why. One thing we know for sure is that the oil market has undergone structural changes, thus making this latest episode different from previous dramatic price fluctuations.

The collapse in prices has been driven in part by supply-side factors.

Posted by at 1:32 PM

Labels: Energy & Climate Change

Tuesday, October 4, 2016

Jobs and Growth: Outlook and Policy Response

My talk today to the Parliamentary Network of the IMF and the World Bank, a group I always enjoy talking to. This time they had really good questions on the IMF position on public infrastructure. And many of them even asked me why the Okun elasticity differs across countries – what more could a nerd ask for?

My talk today to the Parliamentary Network of the IMF and the World Bank, a group I always enjoy talking to. This time they had really good questions on the IMF position on public infrastructure. And many of them even asked me why the Okun elasticity differs across countries – what more could a nerd ask for?

Posted by at 11:14 AM

Labels: Inclusive Growth

Monday, October 3, 2016

Financial Globalization, Inequality and the Top 1%

Davide Furceri and I have revised our IMF Working Paper on the impacts of financial globalization—specifically, the elimination of restrictions on the capital account—on inequality. We find that episodes of capital account liberalization are followed by an increase in the share of income going to the top 1% (the chart below shows the impact). Our previous work had already shown that the Gini coefficient increases following capital account liberalization. The details, and several other new results, are given in the revised paper.

Davide Furceri and I have revised our IMF Working Paper on the impacts of financial globalization—specifically, the elimination of restrictions on the capital account—on inequality. We find that episodes of capital account liberalization are followed by an increase in the share of income going to the top 1% (the chart below shows the impact). Our previous work had already shown that the Gini coefficient increases following capital account liberalization. The details, and several other new results,

Posted by at 1:28 PM

Labels: Inclusive Growth

IMF Research on Inequality: A Primer

The IMF’s recent research on inequality has attracted a lot of (mostly favorable) attention. My talk to CSOs today describes the main findings of this research. Focusing on within-country inequality, I classify the work into three categories: causes, consequences, cures.

- On causes, the main finding is that—in addition to broad trends like trade, technology and demographics—inequality is driven by economic policies. This is not an earth-shattering finding but it is an important one. The policies that turn out to drive inequality include fiscal policies, capital account liberalization (i.e. policies to foster mobility of capital across national boundaries) and labor market policies. Many of these are ‘bread-and-butter’ issues for the IMF, ones on which it routinely gives advice to its member countries.

- On consequences, there has been a novel research finding: inequality lowers the durability of growth spells. This result also puts inequality squarely with the remit of the IMF’s work: fostering sustained growth, a goal of IMF advice, requires some attention to inequality.

- As it should, the work on cures follows from what has been learnt about the causes and consequences. To take an example: if fiscal policies are a cause of inequality, the IMF’s advice on the design of these polices needs to account for this fact. This is both because the distributional consequences may be important in their own right to some governments and because—as noted—they can have an adverse effect on the sustainability of growth. One new research finding, which has implications for the design of many policies, is that redistribution, unless extreme, does not have an adverse impact on growth; hence redistribution need not be feared as a cure.

Details and links to the underlying papers are given in this PPT.

The IMF’s recent research on inequality has attracted a lot of (mostly favorable) attention. My talk to CSOs today describes the main findings of this research. Focusing on within-country inequality, I classify the work into three categories: causes, consequences, cures.

- On causes, the main finding is that—in addition to broad trends like trade, technology and demographics—inequality is driven by economic policies. This is not an earth-shattering finding but it is an important one.

Posted by at 1:02 PM

Labels: Inclusive Growth

Subscribe to: Posts