Tuesday, August 9, 2016

Can Reform Waves Turn the Tide? Evidence on the Effects of Structural Reforms

A number of advanced economies carried out a sequence of extensive reforms of their labor and product markets in the 1990s and early 2000s. Using the Synthetic Control Method (SCM), this paper implements six case studies of well-known waves of reforms, those of New Zealand, Australia, Denmark, Ireland and Netherlands in the 1990s, and the labor market reforms in Germany in the early 2000s. In four of the six cases, GDP per capita was higher than in the control group as a result of the reforms. No difference between the treated country and its synthetic counterpart could be found in the cases of Denmark and New Zealand, which in the latter case may have partly reflected the implementation of reforms under particularly weak macroeconomic conditions. Overall, also factoring in the limitations of the SCM in this context, the results are suggestive of a positive but heterogeneous effect of reform waves on GDP per capita.

For details, see my new paper.

A number of advanced economies carried out a sequence of extensive reforms of their labor and product markets in the 1990s and early 2000s. Using the Synthetic Control Method (SCM), this paper implements six case studies of well-known waves of reforms, those of New Zealand, Australia, Denmark, Ireland and Netherlands in the 1990s, and the labor market reforms in Germany in the early 2000s. In four of the six cases, GDP per capita was higher than in the control group as a result of the reforms.

Posted by at 5:21 PM

Labels: Inclusive Growth

Monday, August 8, 2016

Global Housing Watch Update

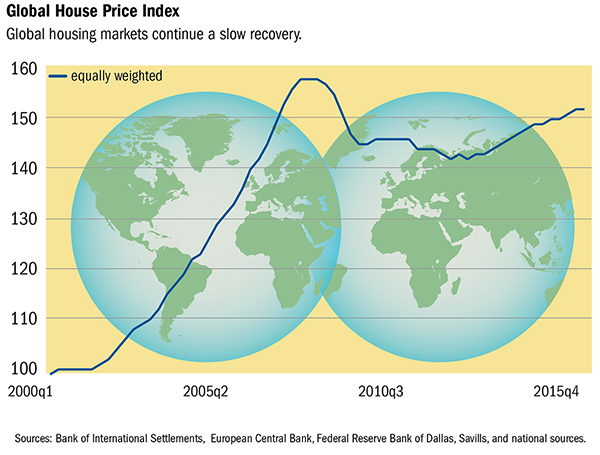

This edition includes: (1) our quarterly update of the Global House Price Index; (2) a discussion of some of the factors associated with the cross-country variation in house prices in recent years; and (3) housing sector developments described in IMF country documents over the past quarter.

The Global House Price Index

Our global house price index shows that, on average, prices are almost back up to where they were at the start of 2007 (Figure 1).

Figure 1

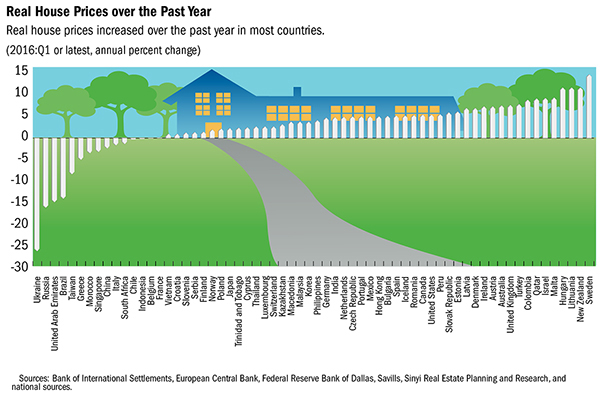

There is a fair bit of cross-country variation, as shown in Figure 2. While house prices have increased over the past year in most countries in our sample, the pace of increase varies quite a bit. And there are still a dozen or so countries where house prices have fallen over the past year, including Brazil, China and Russia.

Figure 2

The underlying data for these charts, as well as charts on credit growth and ratios of house prices to rents and incomes, are available from the IMF’s Global Housing Watch page: http://www.imf.org/external/research/housing/

Probing the Cross-Country Variation in House Prices

Both real house prices and real GDP growth in the 2007-2015 period were well below the boom experienced during 2000-2006. In the earlier period, global real GDP grew by over 4% per year while real house prices surged by about 9% on average. In the more recent period, these grew by just 2% and 1% per year, respectively. The simple correlation between real growth in house prices and GDP growth was very similar in the two periods at about 0.6. Continue reading here.

This edition includes: (1) our quarterly update of the Global House Price Index; (2) a discussion of some of the factors associated with the cross-country variation in house prices in recent years; and (3) housing sector developments described in IMF country documents over the past quarter.

The Global House Price Index

Our global house price index shows that, on average, prices are almost back up to where they were at the start of 2007 (Figure 1).

Posted by at 1:56 PM

Labels: Global Housing Watch

Wednesday, August 3, 2016

Special Issue on Global Labor Markets: Call for Papers

Papers on labor market issues, particularly on low-income countries, welcome for this special issue of Open Economies Review. See call for papers for details. Deadline for submission is Nov. 1, 2016.

Papers on labor market issues, particularly on low-income countries, welcome for this special issue of Open Economies Review. See call for papers for details. Deadline for submission is Nov. 1, 2016.

Posted by at 12:28 PM

Labels: Inclusive Growth

Japan: Minimum wages as a policy tool

A new IMF report discusses whether increases in the minimum wage in Japan will succeed in raising wage growth. It concludes: “In order to revamp growth and permanently exit deflation, Japan needs vigorous wage growth. The government has recognized this and announced substantial increases in the minimum wage and we empirically estimate its impact on average wages. Our econometric results suggest that the 3 percent hourly minimum wage increase could cause monthly wages to increase by about 1.5 percent on a year-on-year basis. The minimum wage policy should be complemented by other income policies—e.g. a “soft target” for wage growth and increases in public wages to create cost-push pressures in line with the inflation target.”

A new IMF report discusses whether increases in the minimum wage in Japan will succeed in raising wage growth. It concludes: “In order to revamp growth and permanently exit deflation, Japan needs vigorous wage growth. The government has recognized this and announced substantial increases in the minimum wage and we empirically estimate its impact on average wages. Our econometric results suggest that the 3 percent hourly minimum wage increase could cause monthly wages to increase by about 1.5 percent on a year-on-year basis.

Posted by at 10:45 AM

Labels: Inclusive Growth

Tuesday, August 2, 2016

Labor Mobility in the United States

The United States has always been regarded as a highly mobile society. Previous work has left the impression that when adverse economic shocks hit their cities or regions, Americans are quickly able to move and find jobs elsewhere within the country. In a new paper, Mai Dao, Davide Furceri and I provide new evidence that questions this view. Our evidence shows that the ability to migrate is not as immediate as previously supposed; in the first year or two after an adverse shock to a state, the bulk of the burden is borne by an increase in the state unemployment and a decline in its labor force participation rate. We also find that while net mobility across states picks up during national recessions, this increase is driven more by a stronger population inflow into states that are doing better rather than stronger population outflow from states that are doing worse; the outflow occurs only toward the end of the recession. Overall, therefore, our results offer a less sanguine view of the ability of U.S. workers to shield themselves from the consequences of adverse shocks than is available in the literature. Here is a link to the paper and to an online appendix which is a wonk’s delight.

The United States has always been regarded as a highly mobile society. Previous work has left the impression that when adverse economic shocks hit their cities or regions, Americans are quickly able to move and find jobs elsewhere within the country. In a new paper, Mai Dao, Davide Furceri and I provide new evidence that questions this view. Our evidence shows that the ability to migrate is not as immediate as previously supposed; in the first year or two after an adverse shock to a state,

Posted by at 4:40 PM

Labels: Inclusive Growth

Subscribe to: Posts