Tuesday, July 19, 2016

House Prices in Peru

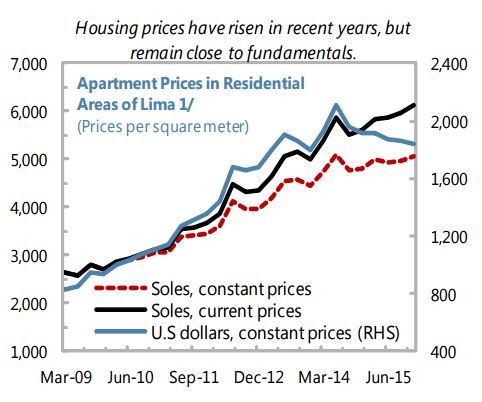

“Housing prices, as reflected by the median apartment prices in Lima, appear high although the price increases since the second half of 2014 have been more subdued than in the previous four years (the average annual growth of apartment prices (in constant soles) from 2011 to first half of 2014 was 14 percent). This may not accurately reflect the segmentation in the market, where there is an oversupply of high-end condominiums in certain residential areas in Lima while low-income housing is in short supply”, says IMF’s report on Peru.

“Housing prices, as reflected by the median apartment prices in Lima, appear high although the price increases since the second half of 2014 have been more subdued than in the previous four years (the average annual growth of apartment prices (in constant soles) from 2011 to first half of 2014 was 14 percent). This may not accurately reflect the segmentation in the market, where there is an oversupply of high-end condominiums in certain residential areas in Lima while low-income housing is in short supply”,

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, July 15, 2016

Housing Market in Poland

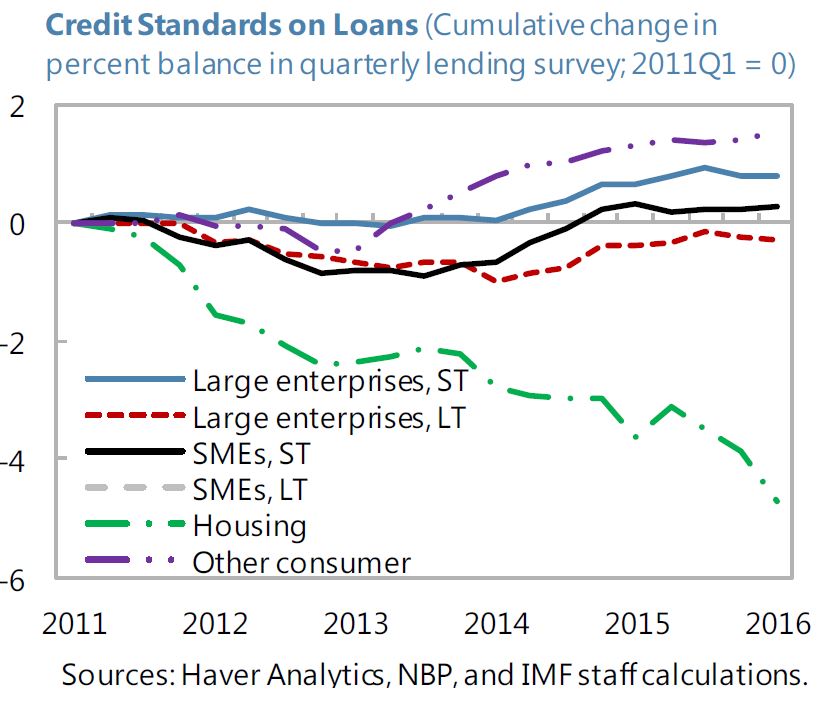

“Credit standards on loans have remained broadly unchanged in recent quarters, with the exception of housing loans, where standards tightened on the back of new prudential recommendations and reduced appetite among some banks for expanding the housing loan portfolio”, says IMF new report on Poland.

“Credit standards on loans have remained broadly unchanged in recent quarters, with the exception of housing loans, where standards tightened on the back of new prudential recommendations and reduced appetite among some banks for expanding the housing loan portfolio”, says IMF new report on Poland.

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, July 13, 2016

House Prices in Czech Republic

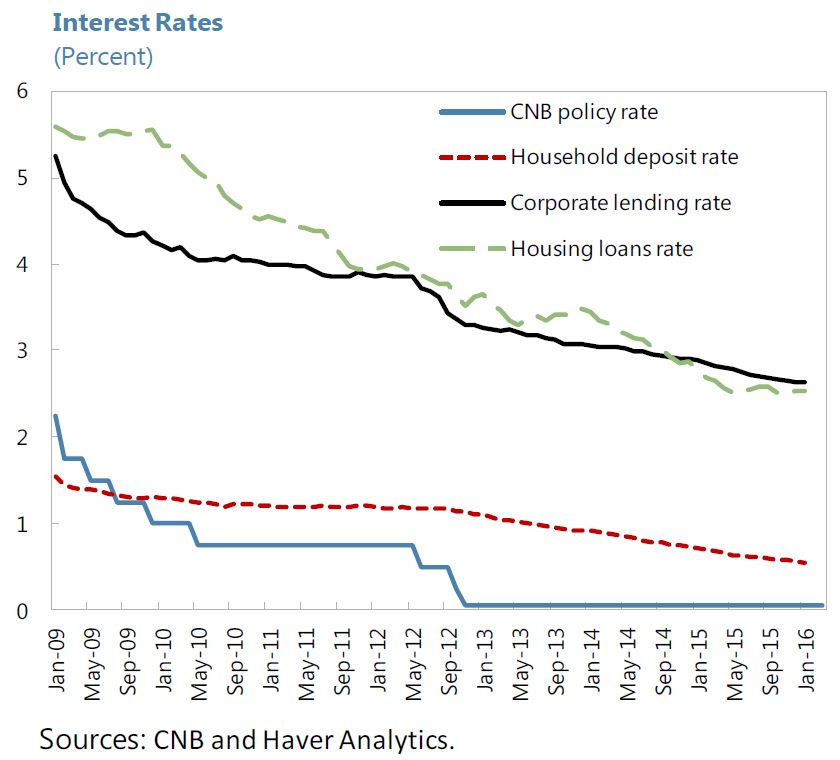

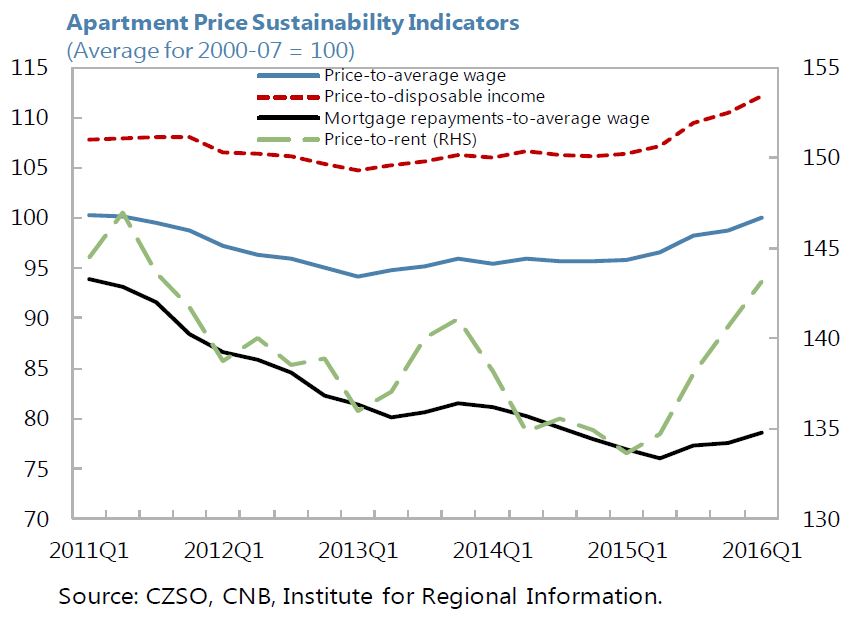

“A strong housing market is becoming a potential source of risk. Mortgage rates are at historic lows and have boosted new mortgage lending to a 10-year high, thus putting upward pressure on prices. Residential housing offer prices increased by 10 percent y-o-y in 2015:Q4, despite a 16 percent increase in housing starts. A slight deterioration in the affordability-of-housing indicators has taken place recently despite strong wage growth and a continued decline in interest rates. On the other hand, the estimated average apartment price-to-annual wage ratio of 4 is still low by international standards. (…) Going forward, continued vigilance will be needed and, if current trends in the mortgages segment continue in the coming months, the macroprudential stance should be further tightened. Preference should given to targeted measures, including raising risk weights on mortgages, lowering LTV limits with possible regional differentiation, and issuing clear guidance on maximum debt-to income limits”, says IMF’s report on Czech Republic.

“A strong housing market is becoming a potential source of risk. Mortgage rates are at historic lows and have boosted new mortgage lending to a 10-year high, thus putting upward pressure on prices. Residential housing offer prices increased by 10 percent y-o-y in 2015:Q4, despite a 16 percent increase in housing starts. A slight deterioration in the affordability-of-housing indicators has taken place recently despite strong wage growth and a continued decline in interest rates. On the other hand,

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, July 12, 2016

What Keeps France’s Unemployment High?

Structural unemployment in France has long been elevated, and appears to have edged up further since the crisis. This reflects both demand and supply factors, including: high labor taxes, wage stickiness, a growing skill gap, hysteresis effects from the crisis years, a lengthy period of elevated economic uncertainty, inactivity traps created by the unemployment and welfare benefit systems, and demographic factors that have pushed up the labor force. The cyclical recovery is projected to bring down the unemployment rate only slowly, and the NAIRU is estimated to remain above 8 percent over the medium term. We investigate the structural causes of unemployment and potential remedies.

Reducing labor tax wedges can increase both output and employment. In France, CICE, PRS and other recent reforms have reduced the labor tax wedge for the low-paid workers. The wedge remains elevated for middle and upper incomes, but further reductions would require difficult policy trade-offs given the high level of public spending.

Strictness of employment protection in France is above the EU average. Labor arbitration procedures are cumbersome and allow making an appeal for a very long time after dismissal, which adds to uncertainty for companies. Reforms easing dismissal regulations could have a sizable positive impact on output and employment when economic conditions are strong. Early studies suggest that the proposed “El Khomri” law, by reducing judicial uncertainty around dismissals, could have a moderate impact on overall unemployment, while stimulating hiring on open-ended (CDI) contracts as opposed to temporary recruitment (on CDD).

Efficiency of collective bargaining depends on flexibility at the firm level, the reach of sector-level agreements, and the effectiveness of coordination among agents. IMF research suggests that France can be classified among countries with “low trust” and “some coordination”, which entails poor unemployment outcome. In France, trade unions play a leading role in collective negotiations even though membership is low. The El Khomri law would extend the scope for firm-level collective agreements.

While the replacement rate of unemployment benefits in France is broadly in line with other countries, eligibility criteria are relatively lax, with rapid qualification and accumulation of benefit rights, and weak job search requirements. Moreover, specificities of the benefit formula create incentives for alternating between ultra-short contracts and unemployment periods.

The ratio of minimum to median wage in France is among the highest in the OECD, which may adversely affect job market chances for the young, the low-skilled, and the long-term unemployed. Its automatic annual adjustment can contribute to wage stickiness.

A detailed analysis by my IMF colleague Nicoletta Batini.

Structural unemployment in France has long been elevated, and appears to have edged up further since the crisis. This reflects both demand and supply factors, including: high labor taxes, wage stickiness, a growing skill gap, hysteresis effects from the crisis years, a lengthy period of elevated economic uncertainty, inactivity traps created by the unemployment and welfare benefit systems, and demographic factors that have pushed up the labor force.

Posted by at 12:28 PM

Labels: Inclusive Growth

Monday, July 11, 2016

House Prices in Norway

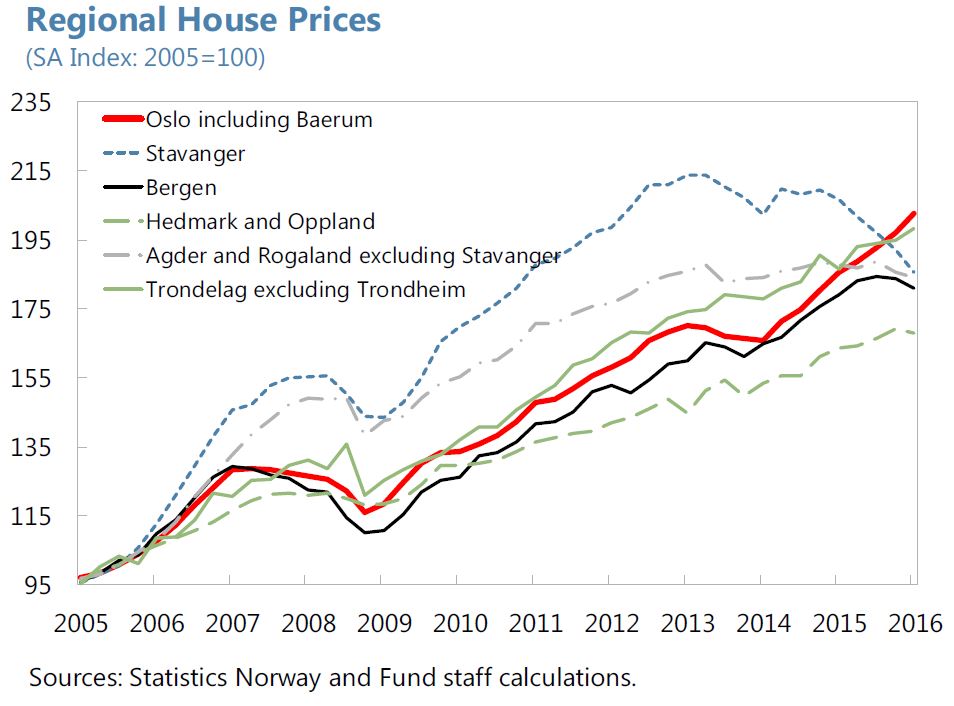

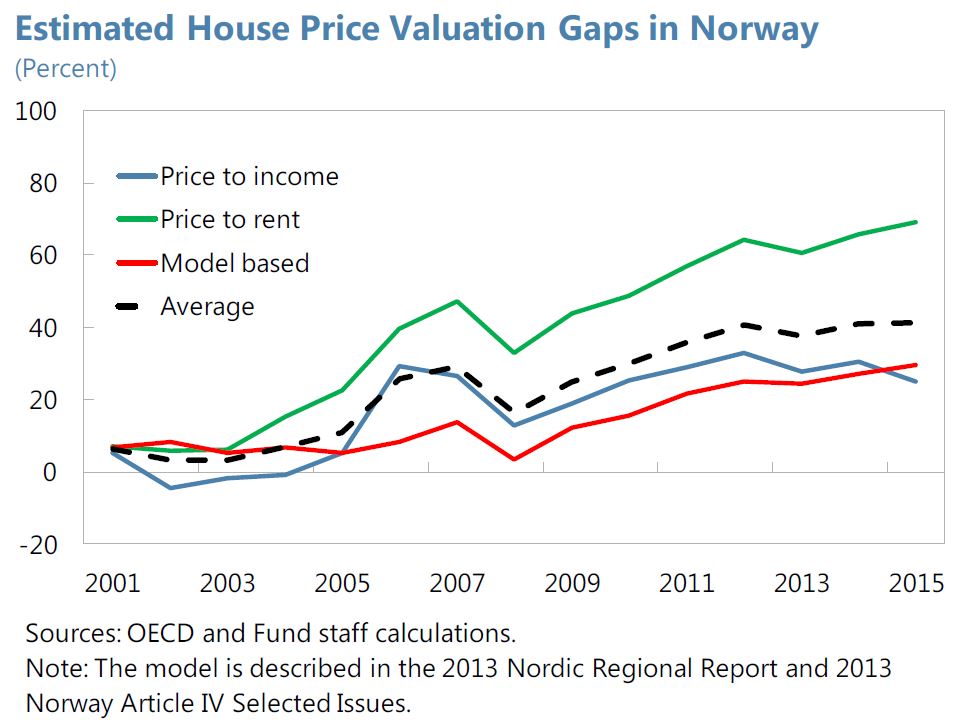

“High and rising house prices and household debt in Norway pose important macro-financial stability risks. Real house prices have risen more than 80 percent in Norway since 2000. Currently, house prices are estimated to be 40 percent overvalued (…) The authorities have introduced a number of measures targeted at the housing market in recent years. (…) Empirical evidence suggests that LTV limits and mortgage risk weights can have significant effects on the growth of mortgage credit and house prices. (…) Results based on a DSGE model suggest that tightening macroprudential measures can reduce household debt ratios with relatively little impact on consumption over the medium-term. (…) Systemic risks from overvalued house prices and high household debt levels suggest that macroprudential policy measures could be tightened further. Addressing structural factors contributing to high household debt and house prices, such as mortgage interest tax deductibility, would reinforce the impact of macroprudential policy measures”, according to the IMF’s report on Norway. See a separate note here on macroprudential policies.

“High and rising house prices and household debt in Norway pose important macro-financial stability risks. Real house prices have risen more than 80 percent in Norway since 2000. Currently, house prices are estimated to be 40 percent overvalued (…) The authorities have introduced a number of measures targeted at the housing market in recent years. (…) Empirical evidence suggests that LTV limits and mortgage risk weights can have significant effects on the growth of mortgage credit and house prices.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts