Tuesday, January 26, 2016

Housing and Systemic Risk

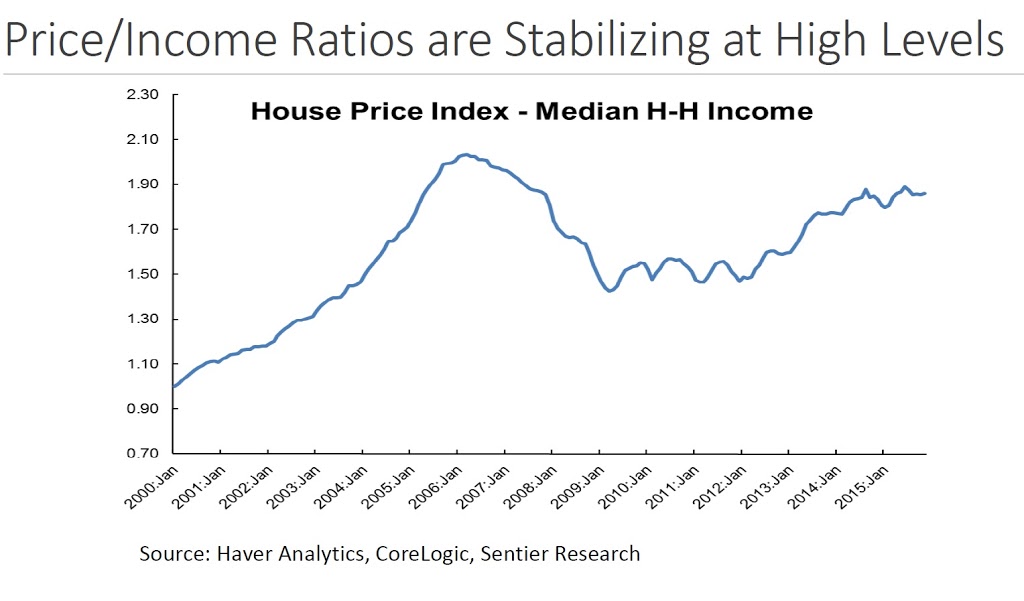

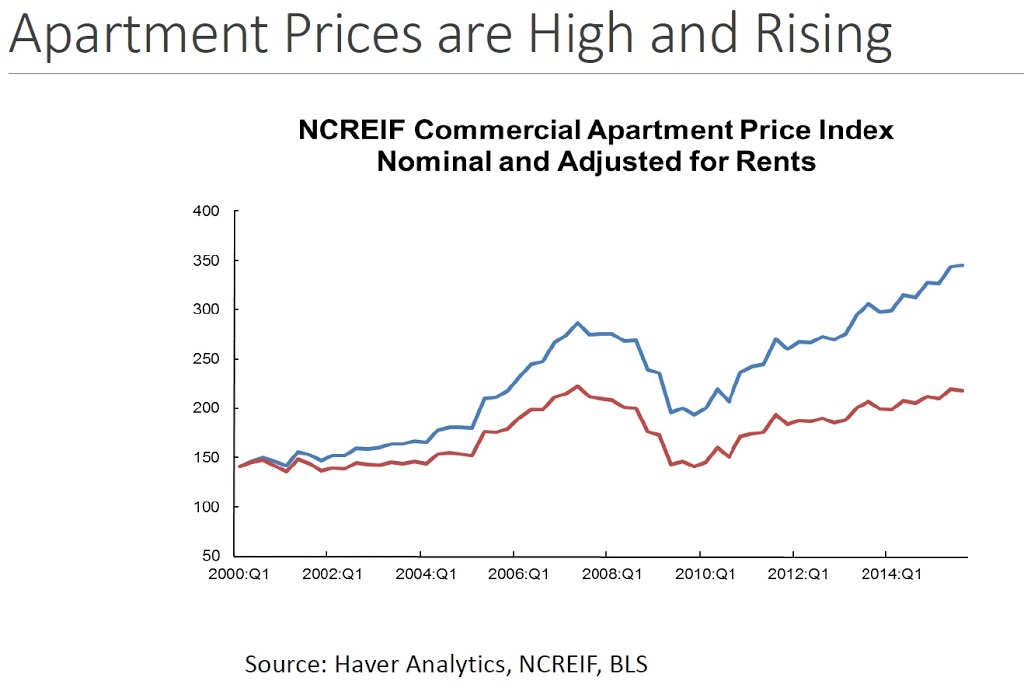

“Single family housing is looking modestly expensive from an affordability perspective, as home prices have generally grown faster than median incomes during the recovery. Similarly, the value of apartment buildings has grown very quickly even compared to the rapid rise in rents in many areas”, says Richard Koss (Global Housing Watch Initiative) in his recent presentation to the Risk Management Association.

Posted by at 1:23 AM

Labels: Global Housing Watch

Wednesday, January 20, 2016

Housing Market in Malta

“While the default rates on mortgages and household indebtedness have been low, further consideration should be given to precautionary measures, such as loan-to-value (currently at 74 percent for residential and 69 for commercial in 2014) and debt-to-income ratios, given the rapid increase in mortgages, relatively high overall exposure to real estate, and pick up in real estate prices—fueled by a combination of factors, such as tax incentives for first time buyers, increase in rental demand stemming from the international investor program, Read the full article…

Posted by at 5:51 PM

Labels: Global Housing Watch

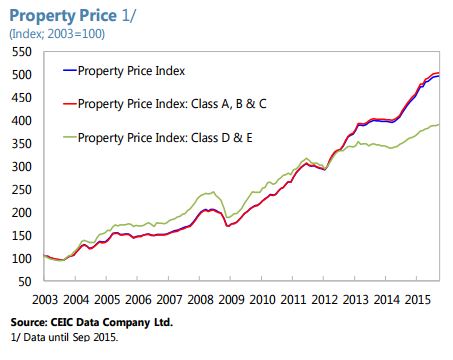

Hong Kong Property Prices: Ripe for a Correction?

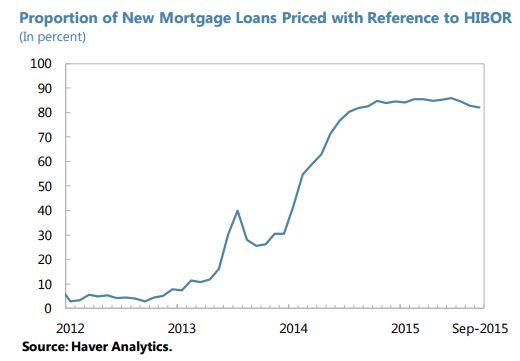

The report also notes that “In the recent run-up, despite the well telegraphed increases in U.S. interest rates, households have continued to opt for floating rate mortgages which will reset in the aftermath of the Fed liftoff. Over 80 percent of new mortgages have been priced off HIBOR in recent months, up from close to zero in 2012. A turbulent and faster-than-expected increase in interest rates could therefore sharply slow property price growth if demand softens in response to the higher cost of borrowing. (…) The authorities noted that the property market may lose some momentum with the interest rate upcycle, but the overall impact was hard to predict. Much will also depend on how the demand-supply imbalance evolves.”

“The propensity for property price run-ups in Hong Kong SAR is rooted in a fundamental demand-supply imbalance at work for some time (…). Nevertheless, around the rising trend, there have been times when prices have slowed or hit a plateau before accelerating again. Prices have also declined around periods of heightened financial volatility (2008-09 and 2011-12). At present, the market appears to be experiencing the onset of relative calm after having gathered steam over the past 18 months”, Read the full article…

Posted by at 5:31 PM

Labels: Global Housing Watch

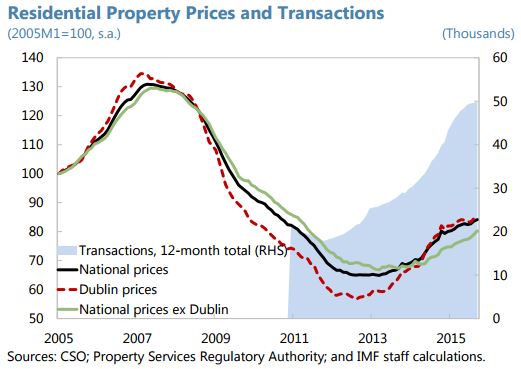

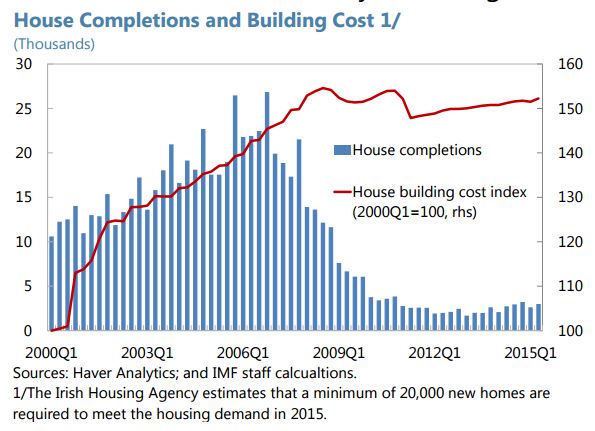

Housing Market in Ireland

“Housing prices have risen by about 33 percent since their nadir in 2013. Cash purchases have lately accounted for about half of total housing purchases. Nonetheless, the CBI’s announcement in October 2014 of macroprudential measures (in force since February 2015) has been associated with moderating expectations of future price increases, and has thus reduced the speculative demand for housing. Though slower, the rate of housing price appreciation continues, in part reflecting a weak supply response”, according to the IMF’s new report on Ireland. Read the full article…

Posted by at 5:08 PM

Labels: Global Housing Watch

Thursday, January 14, 2016

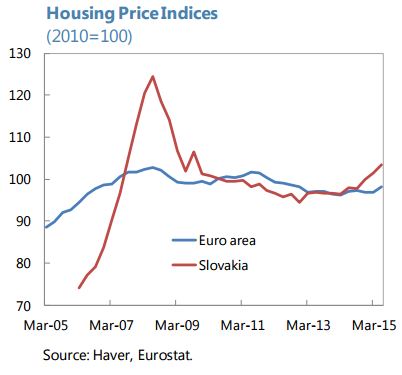

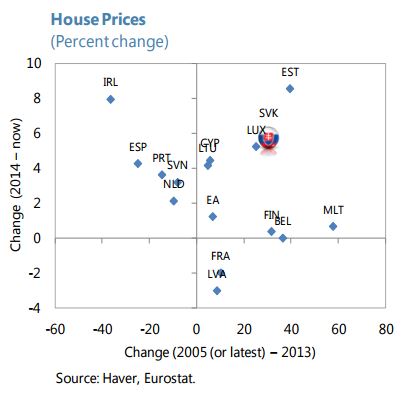

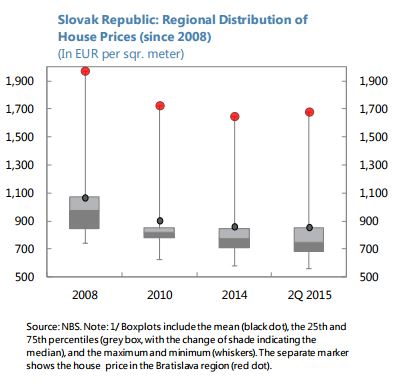

Housing Developments and Macroprudential Measures in Slovak Republic

“Despite a relatively low level of private debt, and (still) high system-wide resilience to potential shocks, fast credit expansion could result in financial imbalances. This paper reviews current credit conditions and household indebtedness, and explores the need for tightening the macroprudential stance. It proposes a set of additional supervisory measures that would build on steps taken by the National Bank of Slovakia (NBS) and guard against adverse impacts on financial stability and the housing market from rapid credit growth. Read the full article…

Posted by at 4:34 PM

Labels: Global Housing Watch

Subscribe to: Posts