Monday, February 2, 2015

On Groundhog Day, Honoring A Forecasting Giant

Herman believes that forecasters should predict recessions early and often: “… the cost of a recession is so great that a forecaster should never miss one … Some people argue that turning points are unpredictable. I disagree. I have never had trouble predicting recessions. In fact, I have predicted n+x of the last n recessions.”

Herman’s colleagues and friends organized a conference on his 80th birthday and the proceedings have just been published in a special issue of the International Journal of Forecasting. The conference versions of the papers are available here.

The issue has an article by Fred Joutz, Tara Sinclair and me, which summarizes Herman’s extraordinary career—the early work on forecasting turning points and why forecasters seem to miss nearly every one of them; the first forecasting assessments of the Fed’s Greenbook forecasts; and much more.

Forecasting is difficult and I honor the people who have to do it. My own interest in the topic was triggered by my awful forecasts for growth in the Asian crisis economies in 1997-98. I have continued my own “astonishing record of complete failure” by completely failing to forecast the recent sharp decline in oil prices. I did call the Patriots-Seahawks outcome correctly.

This Groundhog Day I want to honor economic forecasters—and one in particular, Herman Stekler—rather than make fun of them, which is what I’ve tended to do on past Groundhog Days. Herman has had a 60-year career in forecasting and is still making predictions on everything that moves, including Super Bowl games. He recalls that the interview for his first job at Berkeley “occurred during the famous NY Giants–Baltimore Colts championship football game of 1959. Read the full article…

Posted by at 2:21 PM

Labels: Forecasting Forum

Sunday, February 1, 2015

Global Housing Watch Newsletter

This newsletter aims to present a snapshot of the month’s news and research on global housing markets. If you have suggestions on new material that could be included, you can send it by clicking here. The January 2015 issue includes:

- IMF issues report on housing markets in Denmark, Ireland, the Netherlands and Spain

- The impact of decline in oil prices on housing

- Housing affordability emerging as an issue

- News and research for the following countries: Brazil, Canada, China, Germany, Hong Kong, Israel, Netherland, Norway, Philippines, Singapore, South Korea, United Kingdom, United States, and cross country research.

Read the full newsletter here.

This newsletter aims to present a snapshot of the month’s news and research on global housing markets. If you have suggestions on new material that could be included, you can send it by clicking here. The January 2015 issue includes:

- IMF issues report on housing markets in Denmark, Ireland, the Netherlands and Spain

- The impact of decline in oil prices on housing

- Housing affordability emerging as an issue

- News and research for the following countries: Brazil,

Posted by at 3:47 PM

Labels: Global Housing Watch

House Prices in Advanced and Emerging Economies

In a new paper, Alessandro Rebucci (Johns Hopkins University) and his co-authors have assembled a database that expands the availability of historical house price data for emerging markets.The authors used this database to study the impact of increased global liquidity—an increase in the international supply of credit—on house prices. The paper finds that an increase in global liquidity by 1 percent of world GDP raises house prices in emerging markets by 3 percent, over three times the impact in advanced economies. Read the full article…

Posted by at 3:19 PM

Labels: Global Housing Watch

Friday, January 30, 2015

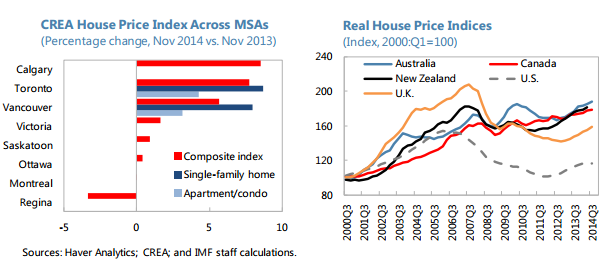

House Prices in Canada

“Housing markets strong with signs of overvaluation to differing degrees. After a brief pause, Canada’s housing market rebounded in 2014, fueled by low and declining interest rates (…). House prices have been rising at 5–6 percent (y/y) nominally through most of 2014 (almost twice the average pace in 2013). Most of the appreciation has been driven by Calgary’s housing market and single-family homes in Toronto and Vancouver (…). Since 2001, house prices have risen significantly—similar to other Commonwealth commodity-exporter countries— though Canada’s cycle seems to be lagging and relatively smoother. Read the full article…

Posted by at 9:42 PM

Labels: Global Housing Watch

Thursday, January 29, 2015

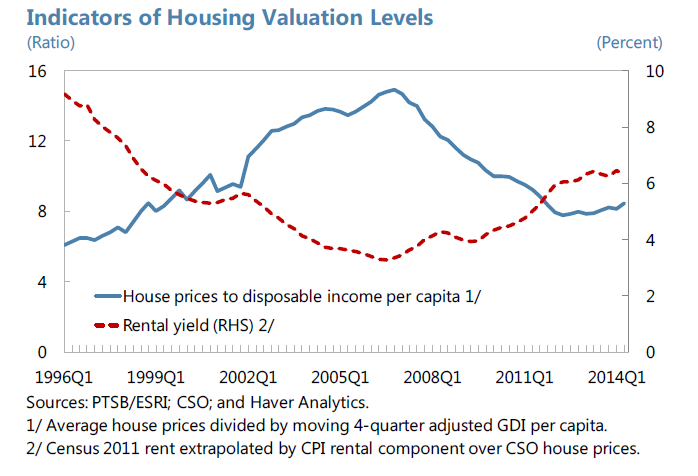

House Prices in Ireland

“Property values are up sharply, though valuation risks are not yet evident, and mortgage lending is beginning to rise from a low base. National housing prices rose 16.3 percent y/y in October, with Dublin prices surging 24.2 percent y/y, though they remain 38 percent below their pre crisis peak. New mortgage loans grew about 50 percent y/y in Q3 2014, from a low base, with about half of all residential property transactions in cash. Residential rents are also rising, and house price ratios to rents and incomes do not yet signal valuation concerns. Read the full article…

Posted by at 11:12 PM

Labels: Global Housing Watch

Subscribe to: Posts