Tuesday, February 24, 2015

Uncertainty and U.S. Unemployment

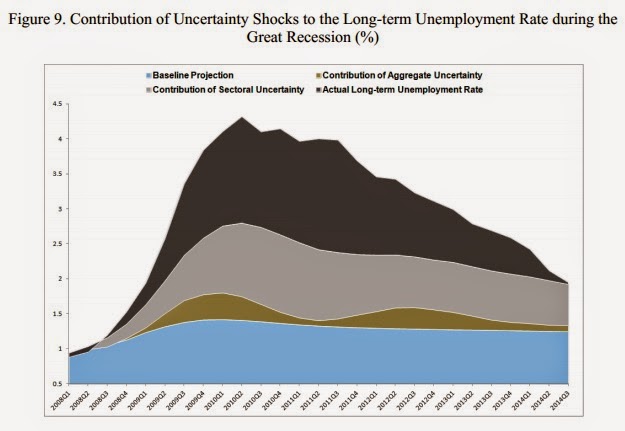

My new paper with Sam Choi updates (through 2014:Q3) estimates of how much uncertainty has contributed to U.S. unemployment (particularly long-term unemployment) during the Great Recession. Our measures of aggregate and sectoral uncertainty are both back to pre-crisis levels. Consequently, the contribution to uncertainty to long-term unemployment has diminished considerably since 2010.

Our aggregate uncertainty measure is the realized volatility of S&P 500 index returns, Read the full article…

Posted by at 12:34 PM

Labels: Inclusive Growth

Friday, February 20, 2015

New Results on Capital Account Liberalization and Inequality

My talk at the New School today included an update of results on the impact of capital account liberalization on inequality (with Davide Furceri and Florence Jaumotte). In past work, we had shown that liberalization leads to an increase in inequality in advanced economies — see this F&D article and VoxEU blog and the discussion of these results by Paul Krugman. The results for a broader group of countries are given in this paper; Read the full article…

Posted by at 5:29 PM

Labels: Inclusive Growth

Thursday, February 19, 2015

House Prices in Slovenia

House prices are are still declining in Slovenia, according to the latest IMF economic report on Slovenia.

Posted by at 3:40 PM

Labels: Global Housing Watch

Wednesday, February 18, 2015

Tom Sargent on U.S. and Europe: A Blast from the Past

Sargent: Yes. I think Europe can learn from the U.S history. In the 1780s, the U.S. consisted of 13 sovereign states and a weak center. The states could levy taxes, the federal government could not. Government debt, federal plus state, was 40 percent of GDP, very high for a poor country. It was a crisis. Creditors worried that they could not be repaid.

Loungani: How was it resolved? There wasn’t an IMF …

Sargent: Well, in the end the outcome was that the U.S. founding fathers rewrote the constitution so that it gave better protection to creditors. The constitution reflected a grand bargain: the central government bailed out the states, and the states gave up the power to levy tariffs. Knowing that the federal government had the power to raise tax revenues gave creditors reassurance that their debts would be repaid.

A fiscal union

Loungani: You’re saying the present U.S. constitution was adopted to give better protection to creditors?

Sargent: Yeah, makes me sound like a Marxist, doesn’t it? But it’s all there in our history. Alexander Hamilton was basically creating a fiscal union—bailing out the states in return for a transfer of tax-levying authority to the center. And the point of a fiscal union was to change the expectations of creditors about the chances of being repaid now and in the future. Note, by the way, that the U.S. had a fiscal union before it had a monetary union.

Loungani: So what are the lessons for Europe today?

Sargent: Don’t some aspects of the EU today remind you of the historical experience I’ve described? The member states have the power to tax, not the center. Many EU-wide fiscal actions require unanimous consent by member states. But reforms that could lead to a fiscal union are being proposed, as they were in the U.S. in the 1780s. I think at the very least the historical episode—not just the one I described but several others that I could—shows that many configurations of fiscal and monetary arrangements are possible, and some of these work to provide assurance to creditors that there will be enough tax revenues to service the debt. I offer this as hope, but I must say that I am not an expert on day-to-day European economics or on their politics.

Curing U.S. unemployment

Loungani: You are an expert on the U.S., and particularly on unemployment, which you’ve also worked on over the years. What would you do about the high U.S. unemployment rate?

Sargent: I would deal with the fundamental causes of financial crisis—the housing market particularly, where there are debts that haven’t been settled and people can’t yet see how they will be settled. And then to the extent that uncertainty about the course of government regulations is holding things back, I’d tackle that.

Loungani: That could take time. How would you ease the pain of the unemployed in the meantime?

Sargent: Some of the European countries, Germany and the U.K., have the right idea. They seem to do better on what’s called welfare-to-work programs—ways of helping the unemployed get into new jobs. We could have done more of that here in the U.S.

Loungani: We extended unemployment benefits many times. Were you in favor of that?

Sargent: I worry that can be a trap—we could end up with persistently high unemployment.

Loungani: Why?

Sargent: You have to go back to the basic ideas in the work that I’ve done with colleagues over the years. Our work builds on the finding that after about 1980 something changed. The [adverse] hits that people suffered to their incomes became more permanent in nature. In the jargon of our profession, the volatility in the permanent component of earnings increased; workers were more likely to suffer permanent shocks to their human capital. Tom Friedman’s The World is Flat has many examples of all this and the reasons why it happened. So we talk about the Great Moderation at the macro level but for individual workers it was just the opposite.

An unemployment trap

Loungani: How does this lead to the trap?

Sargent: Well, think about what can happen when workers suffer a permanent hit to their incomes, and you offer then the alternative of generous and long-lasting unemployment benefits. For older workers, particularly, the benefits become an attractive option relative to looking hard for another job, which is not going to pay as much because your human capital just took a hit. And getting retrained is hard. I mean I was just 30 when my human capital was hit. You know I went to Harvard, right? I actually got pretty good at playing around with the IS/LM model, which is what I learnt there. And then a new thing—rational expectations—came along and I had to learn all this math and it was hard. Well, if you’re in your 50s you’re not going to be eager to try out the hard things. You’ll try to get by with the unemployment benefits. You end up with lots of workers who are detached from the labor force. I think that’s what happened in Europe in the 1980s. They’d always had more a generous welfare system but the impact of that wasn’t felt until the nature of the shocks to incomes changed in the manner that I described.

Loungani: Yes, the interaction of shocks and institutions. Olivier Blanchard once said when the shocks changed Europe became like someone wearing a winter jacket in the summertime—the labor market institutions curbed flexibility when it was needed.

Sargent: Exactly. So I think the people who want to keep extending U.S. unemployment benefits have the right motives but we can end up in the wrong place—a world of persistent high unemployment. So, while in the case of fiscal institutions Europe could look to early U.S. history, in the case of labor market institutions, the U.S. should keep in mind the European experience of not so long ago.

Nobel-Prize winner Tom Sargent has an op-ed in the WSJ. Some of it was in an interview he did with me a couple of years ago.

Loungani: Europe’s fiscal challenges are foremost on minds here. This is something you have worked on in the past—the interplay of monetary and fiscal policy.

Sargent: Yes. I think Europe can learn from the U.S history. In the 1780s, the U.S. consisted of 13 sovereign states and a weak center. Read the full article…

Posted by at 11:49 AM

Labels: Profiles of Economists

Thursday, February 12, 2015

Oil Prices and Employment: Some Evidence from US States

A new IMF working paper finds that an addition of an oil rig “results in the creation of 37 jobs immediately and 224 jobs in the long run, though our robustness checks suggest that these multipliers could be bigger.”

Posted by at 2:35 PM

Labels: Inclusive Growth

Subscribe to: Posts