Monday, June 29, 2015

Housing Supply in Canada

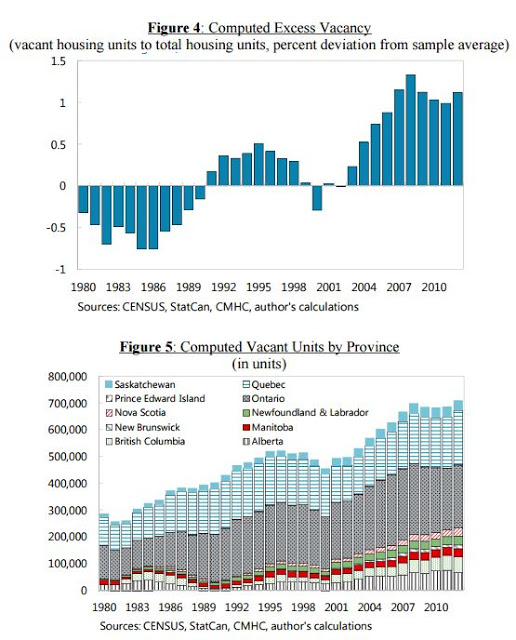

A new IMF working paper sheds “new light on the supply of housing units in Canada. It contributes to the existing literature by (i) providing yearly estimates of housing stock and household formation for the 10 Canadian provinces over the period 1980-2013, (ii) and by estimating excess supply in housing units for the ten Canadian provinces. The empirical results suggest that the Canadian housing market was in excess supply by about 0.5 percent of the total housing stock by end 2013. Read the full article…

Posted by at 8:50 PM

Labels: Global Housing Watch

Thursday, June 25, 2015

House Prices in Ireland

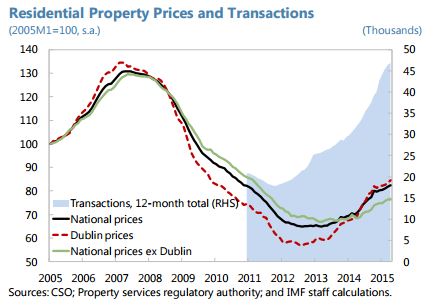

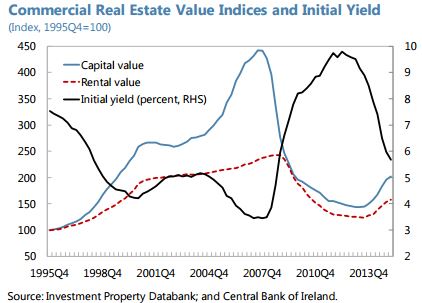

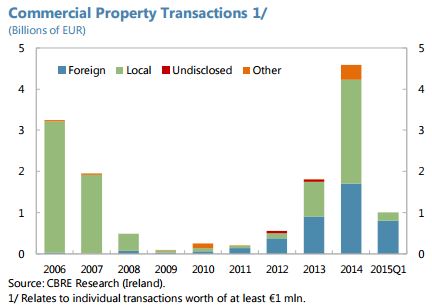

“The share of mortgages on primary dwellings in arrears continues to decline, except for arrears over 720 days. The residential property market is reviving, particularly in Dublin, with some price deceleration in recent months. Commercial property prices and rents rose sharply from a low base in 2014 and transactions rose strongly in 2014 with over one-third by non-residents, and further inflows in Q1,” notes the latest IMF report on Ireland.

Posted by at 2:56 PM

Labels: Global Housing Watch

Friday, June 19, 2015

Fiscal Forecasting Follies: Private Sector vs. Government

Government forecasts of budget deficits invoke considerable skepticism. A prominent critic is Jeff Frankel who mocks the ‘‘budgetary wishful thinking’’ of many government agencies. Frankel notes that during the 2000s, the U.S. Office of Management and Budget ‘‘turned out optimistic forecasts’’ for eight years in a row; likewise, in 2000, the Greek government projected that its budget deficits would shrink below 2 percent of GDP within a year, a far cry from the outcome of 4–5 percent of GDP. Read the full article…

Posted by at 2:44 PM

Labels: Forecasting Forum

Wednesday, June 10, 2015

Housing Finance and Real-Estate Booms: A Cross-Country Perspective

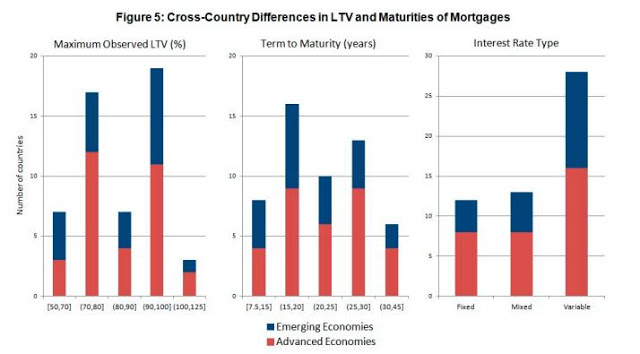

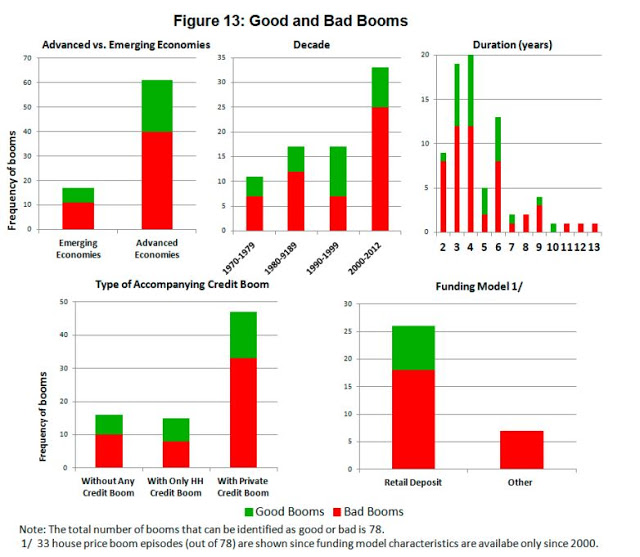

A new IMF paper “analyzes the conflict between the objective of increasing access to housing finance and the dangers associated with fast-growing housing credit. [The paper finds the following:] First, housing finance characteristics vary widely across countries, and several characteristics are correlated with the relative depth of mortgage markets. (…) Second, some of the housing finance characteristics associated with deeper mortgage markets are also associated with increased risks of crisis. (…) Third, in this context, both advanced and emerging markets should avoid relaxing house financing standards in order to achieve deeper mortgage markets, Read the full article…

Posted by at 5:43 PM

Labels: Global Housing Watch

Monday, June 8, 2015

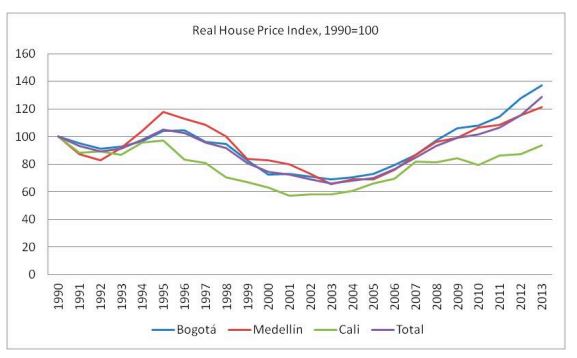

House Prices in Colombia

Moreover, the report says that: “The exposure of households and the financial sector to house price developments continues to be low (…). The growth of mortgages in banks’ loan portfolios remains high, although it has slowed marginally to 17.3 percent in real terms in September 2014. Credit risks are, however, mitigated by a low overall stock of mortgages (about 10.5 percent of total loans), conservative provisioning, and lower housing finance interest rates, which are capped to the lowest rates prevailing for other type of lending. Banks have also been moving towards greater amounts of fixed rate funding for mortgages from variable rates, which should strengthen profitability in a low interest rate environment. Moreover, housing loans extended in recent years have shown less deterioration compared to those made in the past. At 17.5 percent of GDP and 28 percent of disposable income, household debt is moderate, and debt service-to-disposable income is low (9 percent). Although slightly higher than a year ago, LTVs remain low (52 percent).”

“Housing prices have increased rapidly in recent years, raising concerns that the market may be undergoing a bubble. House prices have nearly doubled in real terms over the last decade, equally for subsidized and commercial housing, and are almost 40 percent above their peak in 1996. The price hikes have outstripped increases in construction prices and were mainly driven by a rising trend in the capital and two other large cities. However, the increase in housing prices has been less pronounced after adjusted for income levels and the quality of newly constructed housing. Read the full article…

Posted by at 6:56 PM

Labels: Global Housing Watch

Subscribe to: Posts