Friday, October 16, 2015

Spillovers of Unconventional Monetary Policy

The first panel, “Theory and Evidence of Spillovers,” included presentations by Steven Kamin, (Federal Reserve System); Prakash Loungani (IMF); and Michael Klein (Tufts University).

The second panel on “Policy Implications of Spillovers” featured analyses by Joseph E. Gagnon (PIIE) and Reuven Glick (Federal Reserve Bank of San Francisco). Tae Soo Kang (John Hopkins School of Advanced International Studies), discussed their views from his perspective.

The conference concluded with a high-level panel featuring Olivier Blanchard (PIIE); Jose De Gregorio (University of Chile); and Guillermo Mondino (Citi).

The Peterson Institute for International Economics (PIIE) hosted a conference on “Spillovers of Unconventional Monetary Policy” on October 15. Experts from a wide range of official and private institutions shared their perspectives on the global spillovers of recent policies from the Federal Reserve and other major central banks.

The first panel, “Theory and Evidence of Spillovers,” included presentations by Steven Kamin, (Federal Reserve System); Prakash Loungani (IMF); and Michael Klein (Tufts University).

Posted by at 1:03 PM

Labels: Uncategorized

Monday, October 12, 2015

Dialogue with Angus Deaton

Before the world can answer questions about how poverty is reduced, it needs to know how progress can be measured. But estimates of the number of the world’s poor and questions about whether it has been decreasing or increasing have given rise to one of the hottest controversies in the development community. Angus Deaton, Professor of Economics and International Affairs at Princeton University’s Woodrow Wilson School, who has looked in detail at India’s poverty numbers, has been at the center of this debate. He speaks here with Prakash Loungani of the IMF’s External Relations Department about the dimensions of the problem and what can be done to provide more transparent and more reliable data on the world’s poor.

LOUNGANI: The World Bank’s estimate that 1.2 billion people live on less than $1 a day is cited everywhere. How reliable is this estimate?

DEATON: There’s surely a very large margin of error in that estimate. Even small changes in the design of the survey used to measure poverty can often have dramatic impacts on the poverty estimates. For instance, you could lower the estimate of the number of poor in India by 175 million just by shortening the recall period from one month to one week.

LOUNGANI: It’s a dramatic example, but you’ll have to explain what a recall period is.

DEATON: To measure poverty, you have to survey people and ask them to recall their expenditures— how much they spent on food, clothing, and so forth. You have to choose whether to ask them to recall how much they spent over the past week or how much they spent over the past month. That’s the recall period. Choosing a one-week recall period generally yields higher expenditures, and therefore lower rates of poverty, than choosing a one-month recall period. (The latter is measured on a weekly basis, of course, so that you’re comparing like and like.) India has long used a 30-day recall period. In recent years, the statistical authorities in India did an experiment to see what difference the recall period makes to the estimate of the number of poor. They found, as I mentioned, that shifting to a one-week recall period would essentially halve the number of poor in India. That must be the most successful poverty-reduction program in the world!

LOUNGANI: But haven’t you been working to resolve such data problems and come up with a good estimate of the number of poor in India?

DEATON: Yes, I have been trying to use the parts of the survey that are consistent over time to adjust the poverty numbers and put them on a consistent track. What that has shown in the end is that there has been fairly steady poverty reduction in India. The number of people living in poverty has declined at a steady rate over the past 20–30 years; there is no evidence of a pickup in the rate of decline since the reforms of the 1990s. I end up with an estimate of a poverty rate for India of 28 percent in 2000. Scholars at the Delhi School of Economics, working independently and using methods quite different from mine, have reached similar conclusions

LOUNGANI: Your findings won’t give much comfort to either side of the debate in India.

DEATON: I think that is broadly right. But the reformers have more to cheer about than their opponents. The findings don’t give the reformers everything they would have liked—notably, a pickup in the rate of poverty reduction in the postreform era. But it certainly shows that the claims of their opponents that poverty reduction stalled as a result of the reforms or that poverty actually increased are quite incorrect.

LOUNGANI: Is the problem just with India’s poverty statistics or is it broader?

DEATON: It is a broader problem, but I should remark that, even with all the problems of measurement, we do know that India accounts for about one-third of the world’s poor. So coming up with a more reliable estimate of India’s poor goes a long way toward getting a better estimate of the world’s poverty rate. But the problems that we face with the poverty data in India are quite likely to be present elsewhere.

LOUNGANI: What are some of the problems with the poverty estimates, setting aside the issues of survey design that we’ve already to some extent discussed?

DEATON: Let me try to get the first problem across in a simple way. Suppose that I had tried to see if income growth in China had any impact on the poverty rate in India. Right away you’d say: “That’s crazy. You need the income and poverty numbers to be from the same country.” Well, in most countries the data on income and the data on poverty come from two different sources. And, exaggerating a bit now to make the point, sometimes these two sources are so far apart in the stories they tell that they may as well be from different countries.

LOUNGANI: For example?

DEATON: The problem is endemic, but again the most dramatic case is India’s. According to its national income accounts, India has had robust economic growth over the last decade, and this certainly accords with what most people think has happened. But, at least until the latest figures came out, the national survey statistics, which are the source of the poverty estimates, showed that average consumption has essentially been flat over the last decade. These two stories about what’s happened in India cannot both be right. How can you have strong growth in consumption in the national income accounts and no growth in average consumption in the household survey? Either consumption hasn’t grown as much as the national accounts say it has or consumption has grown more—and perhaps poverty has been reduced more—than the national surveys say it has. So this, in simple terms, is the first problem—the lack of reconciliation between the household survey and the national income accounts.

LOUNGANI: The lack of price indices is also a big problem, I guess?

DEATON: Absolutely. There are two separate issues here. One is that to compare poverty rates across countries, to make the kind of $1 a day numbers that you mentioned are cited everywhere, you have to use purchasing power parity (PPP) exchange rates. Well, revisions to these exchange rates can play havoc with the poverty estimates. The World Bank itself was caught in this trap: in the 1997 World Development Report, before the crisis, Thailand is shown as having a poverty rate of only 1 /10 of 1 percent of the population. This figure was attributed by then chief economist Joe Stiglitz to the Asian economic miracle. But this was less a demonstration of the miracle than of the dangers of inappropriate PPP conversion. It’s a bit disconcerting when the World Bank’s dream of a world free of poverty can be realized simply by misusing exchange rate data.

LOUNGANI: You said there was a second issue with respect to price indices?

DEATON: Yes, you also need good price indices to compare poverty rates within the country, particularly between urban and rural areas. Countries often have good data for urban centers but not for the countryside, which is often where most of the poor live. This can be a big problem. For instance, I think the unavailability of good price indices for rural areas is in part responsible for the very conflicting views of what impact the Asian crisis had on the poor in Indonesia.

LOUNGANI: If the poverty data are so error-ridden, why don’t we rely on other socioeconomic indicators?

DEATON: That is done. Statistics on life expectancy, infant mortality, and literacy are all things that people look at to supplement the poverty numbers. Amartya Sen has been the intellectual force behind this broader look at deprivation. The United Nations Development Program has come up with a Human Development Index that aggregates all this information in a certain way. I don’t think the way they aggregate it is quite right, but at least it’s wrong in a very transparent fashion. But it is important to realize that income or consumption poverty is an important dimension of poverty in its own right and we should not be using other indicators as a proxy for it, any more than we should be using income poverty as a proxy for health or illiteracy. They are different things.

LOUNGANI: Should we just ignore the poverty numbers altogether?

DEATON: No, that’s clearly going too far. I don’t have objections to the concept of poverty. We do have a notion of poverty, like we have a notion of being cold or being hot; people can generally identify who in their community is poor. But it’s one thing to have a rough notion of poverty in your community, quite another to come up with an estimate of the number of poor in the whole developing world. That, as we’ve discussed, requires a lot of decisions. So what I’m objecting to is the pretense that at the end of this series of decisions we can draw a very sharp cutoff, a poverty line. It encourages a rather Micawberish view of things where the result is taken to be happiness on one side of the line and misery on the other. (“Annual income twenty pounds, annual expenditure nineteen nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds ought and six, result misery.”) We should admit that the poverty numbers have large margins of error but keep working to improve them.

LOUNGANI: That’s a nice segue to my final set of questions. What institutional changes are needed to get some quality control on the poverty numbers?

DEATON: The often rather informal arrangements under which numbers are produced need to be looked at. I think the poverty numbers were first thought up for the Bank’s 1990 World Development Report. There was a lot of heroic work by Bank economists to put these numbers together. But they weren’t regarded then as frontline numbers. When folks first started doing GDP numbers, a few academics put some numbers together, and they were thought of as interesting and neat rather than solid numbers you could hang your hat on. Now the poverty numbers have become big important numbers on which many things, including the evaluation of the Bank’s own performance, hinge. At the moment, pretty much no one other than Bank economists can tell you how these numbers were put together and how they can be reproduced. So when someone comes along and accuses the Bank of biasing the numbers one way or the other, it’s difficult for an outside agency or independent scholars to leap to its defense and help resolve the controversy. So we need greater transparency at the Bank on how the poverty numbers are going to be put together in the future. You could imagine setting up other institutions to do this, but greater transparency would get us going in the right direction. And helping countries resolve statistical issues is something that the Bank and the IMF should do a lot more of.

LOUNGANI: It’s difficult for the IMF to take a deep interest in poverty measurement when some still call for us to leave the “poverty business” altogether.

DEATON: I’m in favor of the IMF’s staying in the poverty business, within limits. I was persuaded by [former IMF First Deputy Managing Director] Stan Fischer’s remarks at the conference last year [on macroeconomic policies and poverty reduction] as to why poverty is central to the IMF’s mission. He said that the IMF cannot use the “Von Braun defense”— “I just put the rockets up, and it’s someone else’s business where they fall”—to keep out of poverty. I don’t see how the IMF can cleanly mark out its core mission and say that poverty reduction is someone else’s business. The question is, how far do you go? Certainly, you don’t want to turn yourself into the Bank and hire all the specialists it has and replicate all the detailed poverty analysis it does. But showing greater awareness of poverty measurement issues is essential.

LOUNGANI: What are some areas we could focus on?

DEATON: Several of the problem areas that we discussed are areas where IMF economists are very highly skilled. In countries where there are discrepancies between the national income accounts and the national surveys, IMF staff may have some clues about the extent to which fudges in the national income accounts are responsible. The IMF also has had a long-standing interest in accurate price indices because of the need to get accurate measures of real monetary aggregates, real exchange rates, and the like. And I believe the IMF these days actually issues guidelines on how to provide macroeconomic data and assess their quality. That should be extended to poverty data. This is not the IMF changing its line of business, but simply recognizing that to do your business well you have to be well informed about the measurement of poverty.

Congratulations to Angus Deaton for winning the Nobel Prize in Economics. Below is my IMF Survey interview with Deaton (July 2002) on When numbers don’t tell the full story about poverty in India and the world

Before the world can answer questions about how poverty is reduced, it needs to know how progress can be measured. But estimates of the number of the world’s poor and questions about whether it has been decreasing or increasing have given rise to one of the hottest controversies in the development community.

Posted by at 2:16 PM

Labels: Profiles of Economists

Friday, October 2, 2015

The Frenchman Who Reshaped the IMF

Reflections on the work of Olivier, the IMF’s now retired chief economist.

The IMF is often caricatured as an institution that wants to nail every problem with the hammer of austerity and structural reforms.

An article in TIME claimed that the IMF tends to “dish out roughly similar advice to all countries, no matter what their circumstances,” noting that a cursory look at the IMF’s website would show that “prudent fiscal policy and reforms” had been recommended to Lesotho, France and Russia.

Whatever the merits of the caricature, Olivier Blanchard, the French-born, former MIT economist who served as the IMF’s chief economist from September 2008 to September 2015, achieved a rare feat.

He not only changed perceptions of the institution both on the inside and the outside but also, even more crucially, managed to reshape IMF policies.

Under Blanchard’s watch, the IMF:

- lent its support to a global fiscal stimulus during the Great Recession

- urged a very cautious removal of this stimulus during the Not-So-Great Recovery, and

- staunchly advocated easy monetary policies—including quantitative easing.

Even a famous critic of the institution agreed: “A recovery in aggregate demand is the single best cure … what a relief to hear the Fund say that,” Paul Krugman cooed about the thrust of IMF policy prescriptions during the Great Recession.

Olivier Blanchard also threw out some controversial ideas for discussion, such as: Should inflation targets be raised?

That idea ran into some predictable criticism (“if you flirt with inflation, you end up marrying it,” said a former German Bundesbank president).

But it also drew fire from friendly sources—Blanchard’s mentor and long-time collaborator Stan Fischer, currently the U.S. Fed Vice Chairman, thinks that a higher target would be a “mistake.”

Blanchard also nudged the IMF towards less doctrinaire positions on several other issues, notably on the use of capital controls during crises.

He thereby gave an impetus to a rethinking that had started after the Asian crisis of 1997-98—see my article for The Globalist entitled “The Vindication of Joe Stiglitz.”

The fiscal triptych

The biggest change that Blanchard brought about was in the IMF’s advice on fiscal policies. This came in three steps:

- In early 2008, Larry Summers advocated a U.S. fiscal stimulus that was “timely, targeted and temporary.” Avoiding alliteration’s allure, Blanchard and co-authors advocated a global fiscal stimulus that was “timely, large, lasting, diversified, contingent, collective, and sustainable.”

- Next came a chapter in the October 2010 edition of the IMF’s flagship publication (World Economic Outlook), which Blanchard played an active role in shaping. To the question “Will austerity hurt?” the chapter gave a clear answer: “Yes.

- And then came three pages that Gavyn Davies in a FT blog said could have “a greater effect on global economic policy than all of the interminable” sessions held in Tokyo that year at the Bank-Fund annual meetings.

This was in the October 2012 World Economic Outlook—and subsequent paper — where Blanchard and his colleague Daniel Leigh showed that “in advanced economies, stronger planned fiscal consolidation has been associated with lower growth than expected.”

Translation: the adverse impact of austerity on output was perhaps larger than had been expected.

The upshot of this work was not that fiscal consolidation should never be undertaken. Rather, it was that one should expect austerity to lower output.

Moreover, this effect could be greater in some circumstances (e.g., when monetary policy was constrained because policy interest rates could not be pushed below zero).

It wasn’t just fiscal

Here are three other areas where Blanchard left his imprint through his own writing, by guiding the work of others or by creating an open atmosphere where his staff could explore new pastures:

Who’s afraid of capital controls?

Blanchard presided over a series of papers by IMF staff that nudged the Fund towards a more flexible position on capital controls.

A December 2012 blog by Blanchard and Ostry “explains the logic and research that underpins the shift” in the Fund’s position.

The “4% solution”

In a paper with Giovanni Dell’Ariccia and Paolo Mauro, Olivier posed the question: “Should policymakers therefore aim for a higher target inflation rate in normal times, in order to increase the room for monetary policy to react to such shocks?”

Though the paper never explicitly advocated a new 4% target (that was done later by Larry Ball in an IMF working paper), and certainly not one to be adopted right away, this quickly became known as the “4 percent solution.”

Inequality

The IMF has received a lot of credit for its work on inequality. The finding that captured attention — by Jonathan Ostry and Andy Berg — was that inequality was detrimental to sustained growth.

Blanchard initially regarded this finding as an interesting cross-section correlation and then as a correlation that had cleverly tapped into the zeitgeist.

It is only more recently, in his foreword to the April 2014 WEO, that Blanchard has come to the view that the implications of inequality for macroeconomic developments are a “central issue.”

From the Globalist:

Reflections on the work of Olivier, the IMF’s now retired chief economist.

The IMF is often caricatured as an institution that wants to nail every problem with the hammer of austerity and structural reforms.

An article in TIME claimed that the IMF tends to “dish out roughly similar advice to all countries, no matter what their circumstances,” noting that a cursory look at the IMF’s website would show that “prudent fiscal policy and reforms” had been recommended to Lesotho,

Posted by at 12:14 PM

Labels: Profiles of Economists

Thursday, October 1, 2015

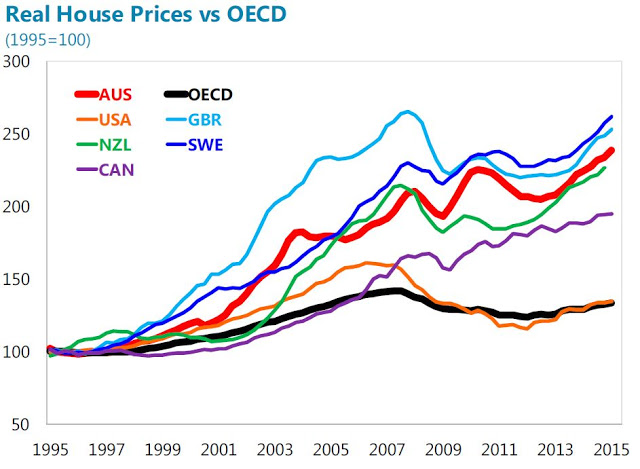

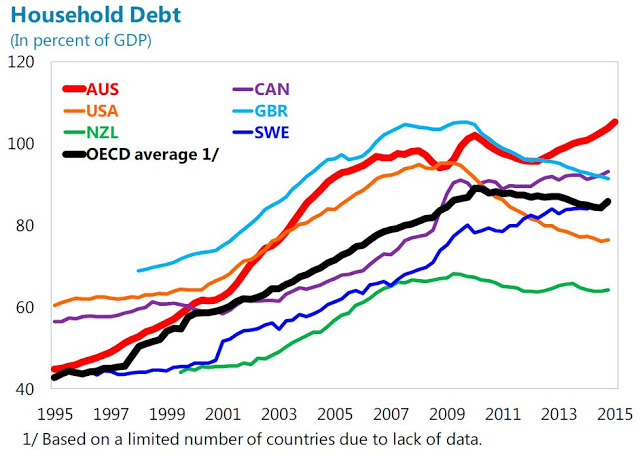

Are Australia’s House Prices Overvalued?

Below is the argument, counter arguments, and the bottom line from the study:

Argument: House prices have risen faster in Australia than in most other countries, suggesting, ceteris paribus, overvaluation

Counter argument 1: House prices are in line on an absolute basis

Bottom line: Price-to-income ratios have risen across all measures in Australia and are now near historic highs. However, international comparisons of price-to-income ratios suggest that Australia is broadly in line with comparator countries, although significant data comparability issues make inference difficult.

Counter argument 2: The equilibrium level of house prices has also risen sharply

Bottom line: Lower nominal and real interest rates and financial liberalization are key contributors to the strong increases in house prices over the past two decades. The various house price modeling approaches indicate that house prices are moderately stronger (in the range of 4-19 percent) than economic fundamentals would suggest.

Counter argument 3: High prices reflect low supply

Bottom line: housing supply does indeed seem to have grown significantly slower than demand, reducing (but not eliminating) concerns about overvaluation.

Counter argument 4: It is just a Sydney problem, not a national one

Bottom line: The two most populous cities, Sydney and Melbourne, have seen strong house price increase in recent years, including in the investor segment. A sharp downturn in the housing market in these cities could be expected to have real sector spillovers, pointing to the need for targeted measures –including investor lending-to reduce the risks related to a housing downturn.

Counter argument 5: There are no signs of weakening lending standards or speculation

Bottom line: While lending standards overall seem not to have loosened, the growing share of investor and interest only loans focused on the highly-buoyant Sydney market, is a pocket of concern.

Counter argument 6: Even if they are overvalued, it doesn’t matter as banks can withstand a big fall

Bottom line: While bank capital levels are likely sufficient to keep them solvent in the event of a major fall in house prices, they are not enough to prevent banks making an already extremely difficult macroeconomic situation worse.

“House prices in Australia have increased strongly over the past two decades, including by comparison internationally. Thus house prices are often argued to be overvalued. Many counter-arguments have been put forward for why such measures are flawed. We argue that house prices are moderately stronger than consistent with current economic fundamentals, but less than a comparison to historical or international averages would suggest”, according to the IMF special report on Australia’s housing market.

Below is the argument,

Posted by at 9:00 AM

Labels: Global Housing Watch

Subscribe to: Posts