Wednesday, September 16, 2015

Israel’s Labor Market: High Inequality, Low Productivity

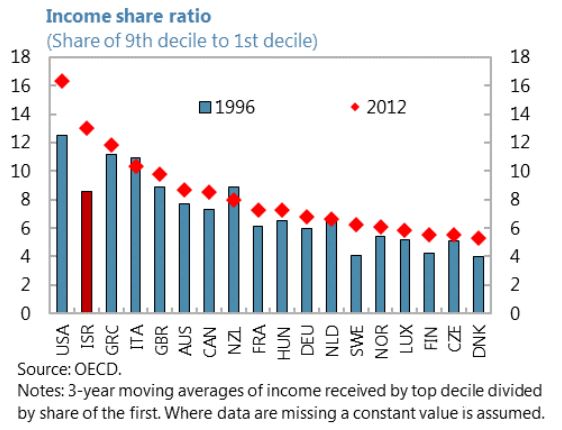

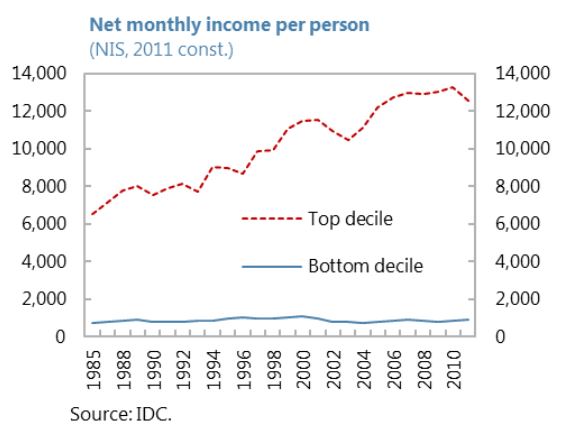

- Inequality in Israel is among the highest in the OECD (this refers to net income inequality, that is, inequality of income after tax and transfers). The income share of the richest 10 percent of people is 13 times the share of the bottom 10 percent, a ratio that is exceeded only by the United States. Real disposable incomes of the top decile have increased since the 1980s, while incomes of the bottom decile have stagnated. Israel’s Gini coefficient of disposable income is among the highest in the OECD.

- Average incomes in Israel are similar to those in Korea and New Zealand but well below the level in richer Western European countries and the United States. There was rapid catch-up toward U.S. incomes between 1950 and the mid- 1970s, but since then Israel’s average income has stagnated at around 60 percent of US average incomes.

- Part of this stagnation is due to low productivity growth. One reason may be that Israel is the most restrictive amongst advanced economies in terms of product market regulations—state control, barriers to entrepreneurship, and barriers to trade and investment all rank amongst the highest across its peers.. In terms of sectors, Israel ranks amongst the highest in regulation of network sectors, retail trade and professional services.

A new IMF report provides an in-depth look at Israel’s labor market:

- Inequality in Israel is among the highest in the OECD (this refers to net income inequality, that is, inequality of income after tax and transfers). The income share of the richest 10 percent of people is 13 times the share of the bottom 10 percent, a ratio that is exceeded only by the United States. Real disposable incomes of the top decile have increased since the 1980s,

Posted by at 5:58 PM

Labels: Inclusive Growth

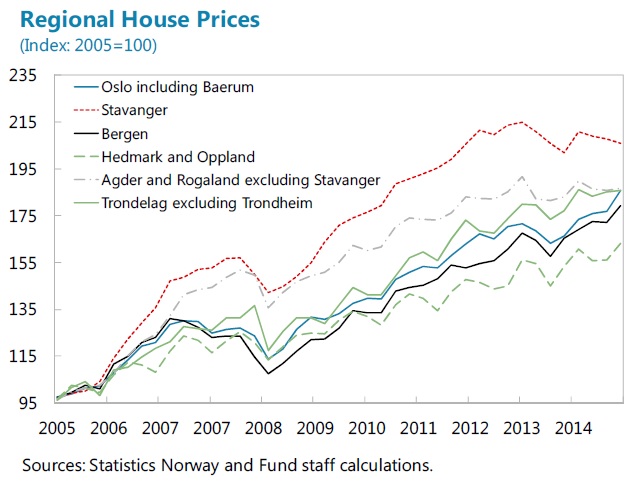

Rising House Prices and Household Debt: A Twin Boom in Norway?

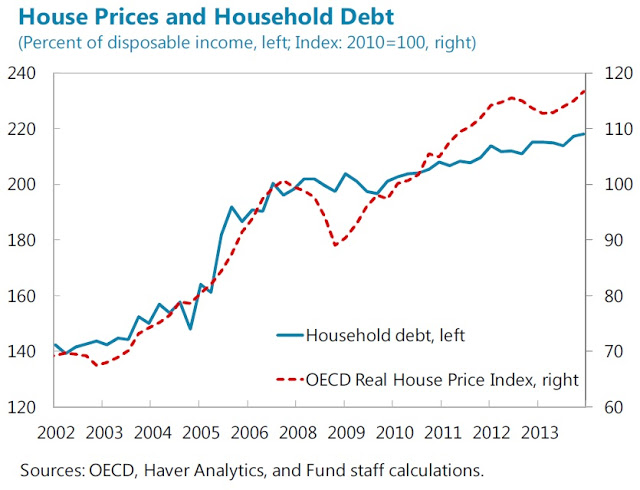

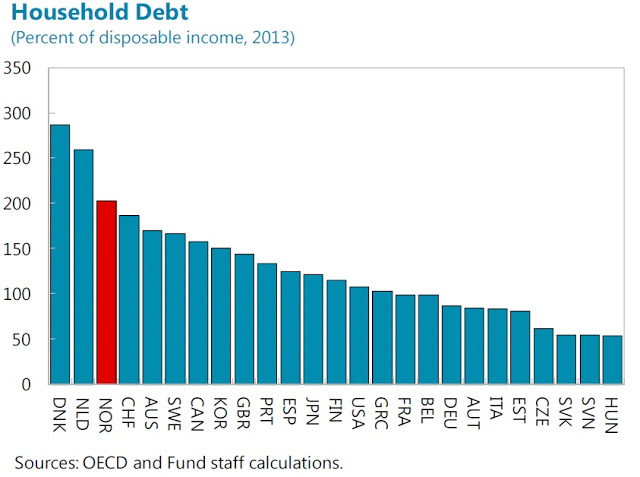

“The Norwegian housing market was only moderately affected by the global financial crisis, and the rising trend of house prices resumed shortly after the crisis. In the meantime, household debt reached more than 200 percent of disposable income, and it is expected to grow further”, a new IMF paper examines the characteristics of household debt and the factors driving the housing boom and debt accumulation. The paper also examines the potential macroeconomic impact of a possible house price correction. Read the full article…

Posted by at 9:00 AM

Labels: Global Housing Watch

Monday, September 14, 2015

Metals and Oil: A Tale of Two Commodities

“It was the best of times, it was the worst of times.” With these words Charles Dickens opens his novel “A Tale of Two Cities”. Winners and losers in a “tale of two commodities” may one day look back with similar reflections, as prices of metals and oil have seen some seismic shifts in recent weeks, months and years.

This blog seeks to explain how demand — but also supply and financial market conditions — are affecting metals prices. We will show some contrast with oil, where supply is the major factor. Stay tuned for a deeper analysis of the trends in a special commodities feature, which will be included in next month’s World Economic Outlook.

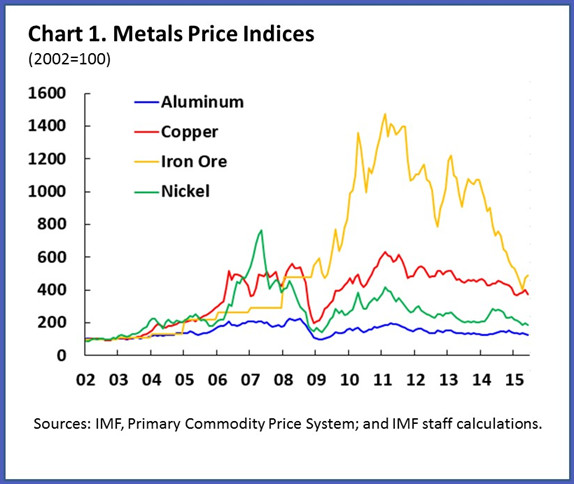

Metals matter

Base metals — such as iron ore, copper, aluminum and nickel — are the lifeblood of global industrial production and construction. Shaped by shifts in supply and demand, they are a valuable weathervane of change in the world economy.

There is no doubt about the direction of the prevailing wind for metals in recent years. Prices have been gradually declining since 2011 (chart 1). While oil prices have also dropped, the decline is more recent (prices peaked in 2014), and more abrupt. That said, in both cases the downward pressure on prices result broadly from abundant production from the era of high prices. This is now coming to roost with lower demand from both emerging markets and advanced economies. There are importance nuances however in the relative strength and nature of those forces.

Appetite for production

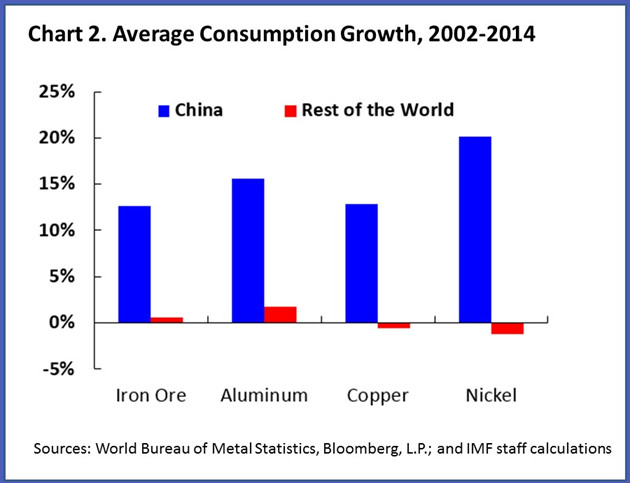

In the early 2000s, demand for metals shifted from advanced economies in the West to emerging markets in the East. China, by far the main driving force, now accounts for half of global base metal consumption (chart 2). Compare that with China’s more modest consumption of 14% of the world’s oil which is almost exclusively used for transportation.

It is therefore no surprise that metals prices are heavily influenced by demand, and the needs of one economic giant in particular. India, Russia and South Korea have also increased their metal consumption, but remain far behind China. The slower pace of investment in China in the last few years, however, compounded by concerns over future demand amid the sharp stock market decline and currency devaluation this summer, have been exerting downward pressure on metal prices.

Oil supply glut

Oil prices tell a different tale. Our view is that supply factors are playing a bigger role than demand. See also our blog from last December. OPEC’s decision to maintain its level of production and strong shale oil production in the United States — in addition to the large production capacity from earlier investment — have contributed to an unprecedented supply glut.

By IMF colleagues: Rabah Arezki and Akito Matsumoto

“It was the best of times, it was the worst of times.” With these words Charles Dickens opens his novel “A Tale of Two Cities”. Winners and losers in a “tale of two commodities” may one day look back with similar reflections, as prices of metals and oil have seen some seismic shifts in recent weeks, months and years.

This blog seeks to explain how demand — but also supply and financial market conditions — are affecting metals prices.

Posted by at 5:31 PM

Labels: Energy & Climate Change

Macroprudential Policies in the Philippines

The IMF’s report on the Philippines points out the macroprudential policies that have been implemented. The report says: “In light of the acceleration in credit growth in 2014 and risks of domestic asset price booms, the BSP [Central Bank of Philippines] conducted stress tests on banks’ real estate loan exposures and required corrective actions, enhanced monitoring of banks’ exposures to all types of real estate, and provided guidance on real estate mortgage loans, setting their maximum loan value at 60 percent of the appraised value. These measures have helped to restrain credit growth to the real estate sector. Single borrower limits (set at 25 percent of core capital) should be strictly enforced with the additional 25 percent allowance for exposures to PPPs allowed to lapse.”

The IMF’s report on the Philippines points out the macroprudential policies that have been implemented. The report says: “In light of the acceleration in credit growth in 2014 and risks of domestic asset price booms, the BSP [Central Bank of Philippines] conducted stress tests on banks’ real estate loan exposures and required corrective actions, enhanced monitoring of banks’ exposures to all types of real estate, and provided guidance on real estate mortgage loans,

Posted by at 9:00 AM

Labels: Global Housing Watch

Friday, September 11, 2015

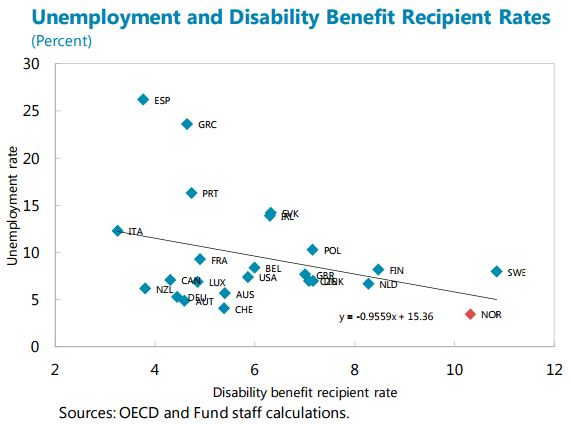

What Lies Behind Norway’s Low Unemployment Rate?

The unemployment rate in Norway is one of the lowest among OECD countries. At the same time, according to an IMF report, absence from work due to sickness “is the highest among the OECD countries, and so is expenditure on health related benefits, which is more than 5 percent of GDP. About one-fifth of the working age population receives income supports related to health problems or disability, which is nearly everybody who is not working. Read the full article…

Posted by at 9:00 AM

Labels: Inclusive Growth

Subscribe to: Posts